But analysis from ANZ suggests risks of a financial collapse are unlikely — at least when it comes to the residential property market.

ANZ senior China economist Betty Wang and colleague Kaushik Baidya based their thesis on two arguments:

While mortgage growth has increased rapidly in the last three years, China’s debt-to-GDP ratio is still lower than many developed economies; and

Based on China’s aggregate loan-to-value ratio, there’s room for a significant price correction before lenders come under material stress.

Residential housing mortgages in China amounted to 21.9 trillion yuan as at Q3 2017, representing an increase of about 27% a year since 2015.

And the rise in mortgage activity has seen total Chinese household debt rise to 48% of GDP as at Q3 2017 — up from 38.8% in 2015.

However, “while the rapid rise in household debt and mortgage has caught the attention of the Chinese government, we think concerns about property bubble have been over-stated”, said Wang and Baidya.

For one thing, China’s household debt-to-GDP ratio is still less than half that of Australia, which has a ratio of well over 100%:

In addition, the analysts said China’s banking sector has a broader loan portfolio, and is thus less exposed to residential mortgages.

“For the banking sector, the share of home mortgages stood at 18% of total loans in 2017, one third of that in Australia and 70% of that in the US,” the analysts said.

Wang and Baidya added that an assessment of loan-to-value (LTV) ratios on issued mortgages is a more effective stress-test than debt-to-GDP. A higher LTV means more money is required from the borrower up front.

Mortgage data in China is hard to come by so the analysts constructed an indicative model based on available information.

The pair used new building sales as a proxy for estimating mortgage issuance, and applied a model based on one-year lending rates for data before 2009 (when mortgage rates data wasn’t released).

They also estimated mortgage length and rebuilt the National Bureau of Statistics’ property price index back to 2004 to get a more accurate picture of collateral household wealth.

“The weighted average LTV ratio was 33.8% as of 2017, according to our calculations. It means that the market value of collaterals (i.e. underlying properties) is almost two times the outstanding loans,” the analysts said.

“We find that all cohorts can bear a substantial 50% decline in property prices (if not bigger) without running into negative equity.”

“We expect that many mortgages drawn in early years have been paid up by now. At the same time, prices of the underlying properties doubled from early 2000s, substantially boosting the market value of the collateral.”

They said the rapid rise in mortgage growth over the last three years adds an increased level of risk to the market.

However, the LTV ratio of more recent loans is a stringent 40% — much higher than the 20% requirement for loans issued before that.

Furthermore, in line with the recent crackdown on excessive leverage by Chinese authorities, annual mortgage growth has slowed to 22%, down from 36% in 2016.

“As long as the collateral value of these parts of mortgage is not falling significantly, the government’s cooling measures since 2016 will prevent the risk from further escalation,” the analysts said.

Home sales in Sydney and Melbourne fell last year to their lowest levels in at least four years as stock shortages kept listings low and tighter credit rules hampered investor purchases.

The figures are preliminary, and likely to be revised higher as more home settlement data is recorded for transactions sealed during the quarter, but official figures showing lower transaction numbers and weaker dwelling price growth laid bare the growing risk for state governments that have become accustomed to strong stamp duty revenues in the now-ending booming housing market.

"The slowdown in price growth and reduction in the amount of transaction volumes places states like NSW and Victoria in a difficult position when it comes to their revenues," said Housing Industry Association senior economist Shane Garrett. "Stamp duty is something they depend on a lot and they're now at risk of seeing a reduction in stamp duty revenues."

Transfers of established houses in the NSW capital slipped to 46,361 last calendar year, down from 50,383 in 2016 and the weakest number since 2012, when they totalled 44,298, the preliminary Australian Bureau of Statistics figures on Tuesday showed.

The drop in attached dwellings – apartments, townhouses and semi-detached homes – was even greater, with the annual total dropping to 37,129, the lowest since 2006, when it was 34,970.

While the figures show the effect of tighter credit rules for investors particularly in the Australian state with the highest proportion– about 40 per cent –of investor buyers, it also indicated the effect of soaring prices that have encouraged people to renovate and stay where they are rather than move house, and also some displacement as buyers opted for newly built homes over established ones.

Transactions slowed

Dependence on stamp duty has soared in the two largest states in recent years. In NSW it jumped from 18.1 per cent of total revenue in 2012 to 28.1 per cent in 2016, and in Victoria it rose from 22.3 per cent to 30 per cent, HIA analysis shows. Queensland was the next highest, at 23.9 per cent, followed by Tasmania (20.2 per cent), SA (19.6 per cent), WA (19.4 per cent), NT (18.8 per cent) and ACT (18.2 per cent).

Home transactions also slowed in Melbourne, where investors make up a smaller proportion of total sales, although the decline was less dramatic. Established house transfers fell to 46,361, also a five-year low, while attached-dwelling transfers slowed to 35,569, their lowest since 2013.

"It underlines the unreliability of stamp duty as a source of state government revenue and it re-emphasises the importance of states generating revenue from other sources outside of stamp duty, if they want to keep their finances on a sustainable path," Mr Garrett said.

Separately, the figures showed the average price growth slowed across Australia's eight capital cities in the December quarter, to 5.6 per cent for houses from 9.3 per cent in the same quarter a year earlier. Attached dwelling prices also slowed, to 3.4 per cent from 5.1 per cent a year earlier for apartments. Both were pulled lower by the Sydney slowdown.

Former treasurer Peter Costello told the Urban Development Institute of Australia national conference on Tuesday that higher borrowing costs would inevitably push the prices of assets, including property, lower."

"It's going to be slow and it could be painful and the question is will it be a hard landing or a soft landing but it's going to be a landing," Mr Costello said.

This article was originally published by Scott Carbines on MARCH 21, 2018 via news.com.au

MANY Melburnians who bought in the right suburbs 10 years ago can now count themselves to be millionaires and among the country’s luckiest homeowners.

House prices have surged over the past decade, with Kingsville, Notting Hill and Forest Hill in the nation’s top 10 for price increases in suburbs now around the $1 million median mark.

Kingsville’s median house price rose the most in that category in Melbourne, growing $651,000 to $1,091,500 over that period, CoreLogic data to March collated by realestate.com.au shows.

But the city’s middle eastern suburbs dominated the list, with Notting Hill ($638,500 increase), Forest Hill (up $594,362), Vermont (up $586,500), Nunawading (up $586,000) and Mitcham (up $575,912) homeowners sitting on goldmines after their property choices proved financially fruitful.

Newport’s median house price increased $530,000 to $1,082,500, Oakleigh South’s $550,000 to $1.035 million and Flemington’s $540,000 to $1.095 million.

The property at 112 Wales St, Kingsville, has a price guide of $1.54 million. Source:Supplied

CoreLogic Victorian director Geoff White said the middle to outer eastern suburbs had benefited from buyers looking further out than the always-strong suburbs closer in.

“The people that tend to buy in that area are definitely those that would look at the inner east and then realise it’s not so much in their budget, Camberwell or Hawthorn, and then consider the outer eastern suburbs as the next best alternative,” he said.

“The amenity of areas like that, the standard of housing, buildings, infrastructure and shopping all plays into those areas as well, so invariably if someone can’t afford one suburb they’ll look at the next or one nearby and that’s the scenario with that, ‘it’s not far from where we’d like to have been and it’s more in our budget’.”

Mr White added buyers had woken up to suburbs like Kingsville, that might have been overlooked in the past, being great places to live close to the city.

Don't miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Dear Fellow Property Investor,

A decade ago, 71 per cent of houses and 75.8 per cent of units in Australia's major capital cities sold for under $400,000. Similarly, a decade ago, only a small fraction, 3.4 per cent of houses, and 1.9 per cent of units located in the major capital cities sold for more than $1 million dollars.

In mid-2016, just 10 years later, a significant percentage of suburbs joined the $1 million dollar club, with 12.4 per cent of houses, and 4.6 per cent of units exceeded the magic $1 million dollar range.

What's interesting now is that a house with a $1 million dollar price tag has become a very common occurrence across many of Australia's suburbs located in the major capital cities. The new benchmark today, it seems, is to break the $2 million dollar mark, and join the elusive $2 Million-Plus Club.

So, let's just stop for a second and reflect back on the implications of the $1 and $2 million dollar club. I don't know about you but to me it's just incredible that it's now a common occurrence for people to spend $1 million or $2 million dollars for a house in a good suburb.

For those readers old enough, just think back 10 years ago when the median price in Melbourne was $370,000 or 20 years ago when the typical house cost $150,000 to even consider back then anyone buying a house for $1 million or $2 million dollar price tag?

It was something you heard millionaires doing in Mossman or Toorak, but definitely out of reach for the average Australian family. And that's for houses...if you consider now that there are penthouses (apartments) in Sydney and Melbourne selling for $10 million to $15 million it's just incredible!

Whilst the top suburbs in Australia continue to accelerate in prices, for the first time a significant percentage of the population are being permanently squeezed out of the housing market, according to recent survey results from REST Industry Super show.

They survey of 1000 Millennials found more than half of 18 to 34-year-olds blamed rapidly rising house prices and the increased cost of living for pricing them out of home ownership. REST Industry Super Chief Operating Officer, Andrew Howard, said research found the majority of respondents believed home ownership was just as important to them as it was for their parents, "so they're obviously feeling quite disheartened about the current property market".

This short video gives them some hope by highlighting three valid investment options in Melbourne under $500,000.

Don't miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Don't miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Here is what you will learn by watching this video:

You have probably heard the old saying "land appreciates, and buildings depreciate", and I must say that if I had a dollar every time I heard this phrase at a seminar, workshop, radio or read in a book I would probably have a deposit for a good investment property in one of Australia's top suburbs.

Finite all-encompassing statements like these have been thrown around in property investing for decades.

It's a combination of folklore, vested interests, or just plain old ignorance.

Here are a few more that you may have come across;

You always make money on property in the way in,

Always buy cash flow positive property, and never fall into the negatively geared trap,

Location, location, location is the most important criteria when selecting properties,

And the list goes on, and on...

The objective of this video is to dispel these myths, and arm you with the ability to conduct unbiased due-diligence and become a more informed and intelligent investor, rather than listening to the herd. Once you gain a clear understanding of the real key drivers behind property appreciation, which as you will find out in the video run far beyond the intrinsic value of the land and the building of a property, then you will be able to objectively identify and zoom in on the very best suburbs, streets in those suburbs, and specific properties with laser like precision, and achieve capital growth beyond the market average.

If you look at this statement from a strictly literal perspective, it would imply that the only investment properties that can appreciate in capital growth are those with a significant land component in them, or more specifically, that the value of a property is determined more on the size of the land content than on the building component.

Now I don't know what the exact land content is require in order for a property to fulfil its minimum prerequisite to be deemed a property that has land, but given that this phrase has been excessively propagated by house and land developers, or agents selling house and land estates, I will assume that a good 500 square meters or even 1000 square meters plus, would tick the box.

The premise being made in the "land appreciates, and buildings depreciate" statement is an overly simplistic one that unless property has an intrinsic land component it cannot appreciate value, or it would outperform the capital growth potential of those properties with a low or from a practical perspective non-existent land component, such as apartments, or to a lesser extent townhouses.

I can tell you that making such finite oversimplified statements is a sure way to lose all your money in real estate, fast!

Don't miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

This article was originally published by Megan Miller on March 9, 2018 via Herald Sun.

MELBOURNE’S inner north, inner west and CBD continue to be strong dining destinations, but Dandenong in the southeast and Laverton in the southwest are emerging as the next hot spots.

Parkdale and Coburg are also among a list of seven suburbs identified in analysis by corporate giant PwC.

Analyst Jonathan Cairns-Terry said their popularity was determined by accessibility via public transport and a ripple effect as higher rents in suburbs closer to the city forced food operators further out.

“Not everyone is going to live within 30 minutes of the CBD and if you’re wanting to have a thriving dining and night life scene some of that is going to have to move out of the centre,” he said

“Precinct development is where we see urban planning going and dining, bars and entertainment is part of providing that whole package.”

Acclaimed chef Scott Pickett put Northcote on the foodie map in 2011 when he opened his first solo venture Estelle. At the time, the inner north was all about Fitzroy.

“There were a lot of great little places around here, and I wanted to be part of it, but just take it to the next level,” he said.

“It was a bit cheaper (than Fitzroy) both for restaurants and to live, but that gap has closed and they’re now much closer in pricing.”

Research also shows how Melbourne’s coffee obsession has spilt into the property market, with homebuyers’ caffeine cravings fuelling demand for suburbs with cool cafes.

Coffee-obsessed buyers are paying up to 20 per cent more for homes in areas that offer lifestyle and convenience, including being within walking distance of their daily brew.

Proximity to cafes, bars and restaurants is as important as access to schools, parkland and public transport to an increasing number of homebuyers who are seeking the lifestyle, village atmosphere and better connection to their community that cafes give, say leading buyers advocates.

Nicole Jacobs, of Nicole Jacobs Property, said these lifestyle factors contributed to emotional buying, which drove up prices.

“The market can tell us what a property is worth but emotion comes in and who knows how much people are willing to pay? It might be 10 to 20 per cent more,” she said.

“For a lot of young professionals, their infrastructure is cafes and restaurants. For them, it’s not schools at the moment. They’re looking at their lifestyle, which is wanting to walk to the cafe at the weekend, read the papers and have a great meal.

“Everyone is gravitating more to that village atmosphere. You go to the big complexes when you’ve got a lot of shopping to do, but you’d rather hang out in your little village, which is usually anchored with a great coffee shop.

“That’s what everyone’s going back to and what’s driving a lot of the suburbs.”

Agents regularly highlight nearby cafes in for-sale brochures and often serve the cafe’s lattes and flat whites to successful buyers to welcome them to the neighbourhood.

Jon Martin has moved to Sandringham to be close to family but also because of the suburb's great coffee shops. Picture: Jake Nowakowski

Developers of new housing estates in outer suburbs are prioritising cafes as much as roads and schools to helping to create a village, while developers of new apartment blocks will lock in high-profile cafe operators early for their ground floors as a selling tool to potential residents.

“Do people gravitate to areas just because of cafes? Yes,” Ms Jacobs said.

“Developers have seen that and will approach a cafe team to set up their second or third business to attract buyers.

“They have a recipe that works — it’s groovy, it’s artisan and then they replicate that in another suburb that’s taking off.”

Elite Buyer Agents managing director Kim Easterbrook agrees that suburbs with good cafes and restaurants attract higher prices.

A worn-out house in Beaumaris that was marketed as a new home site soared $720,000 above reserve before selling for $3.72 million at a weekend auction.

The strong result for the 1940s house on a 1111-square-metre block at 2 Point Avenue, near Ricketts Point, highlights how free-title properties with development potential are faring better than some period-style homes in the current market.

On Saturday, several prominent Victorian homes that were affected by restrictive council heritage overlays failed to attract bids at their auctions. In contrast, other Victorian and Edwardian houses, not subject to heritage overlays, received offers from multiple bidders and sold strongly.

A home at 32 Lisson Grove, Hawthorn failed to attract any genuine bids at auction.

The real estate agent’s catchcry that “if you can knock it over, it’s worth more” was wholeheartedly embraced by buyers at auctions in Hawthorn, Balwyn North, Bentleigh East, Brighton and other suburbs.

Hodges auctioneer Michael Cooney fielded six bidders at the sale of 2 Point Avenue, which was quoted at $2.8 million to $3.08 million.

The property last changed hands in 1944 and is subject to a single dwelling covenant, meaning that a new house – but not multiple flats or townhouses – can be built on the site.

2 Point Avenue sold for $720,000 above reserve at auction this weekend.

That caveat didn’t stop the rare site from climbing $720,000 above reserve or the six bidders from posting 104 bids for the property.

“I haven’t had 104 bids for a while,” Mr Cooney said. “This is the number one spot in the Black Rock/Beaumaris area: the properties come up once every 10 years, if that.”

He added that demand for homes and knock-down-and-rebuild sites between $2.8 million and $4 million was very strong in the prized pocket, in part because the area had no designated high-density development zones.

This meant only townhouses could be erected on greenfield sites, a factor that was attracting families away from other Bayside suburbs experiencing more intense unit development.

Overall, the residential market trended down slightly at the weekend. The weekend clearance rate for metropolitan Melbourne was 65.7 per cent from 989 auction results reported to the Domain Group. This compares to 69 per cent from the 1085 auction results reported on the previous weekend, which the Domain Group has now revised down to 64.4 per cent after counting late reported results from February 24 and 25.

Heritage overlays are vigorously supported by hundreds of home owners in the Boroondara and Stonnington council areas and in other heritage-rich locales as they protect streetscapes from radical change.

On Saturday, Kay & Burton auctioneer Sam Wilkinson pointed out these sought-after benefits to a crowd of 80 at the auction of a beautifully proportioned Victorian home in need of some TLC at 32 Lisson Grove, Hawthorn.

But the pitch failed to generate any genuine bids for the 1671-square-metre property, which was passed on a single vendor bid of $5.7 million.

Elsewhere in Hawthorn, two period homes without heritage overlays sold well.

Buyer’s advocate and architect Adam Woledge said a five-bedroom Edwardian-style house at 66 Illawarra Road sold for $4.33 million through Marshall White with competition from three bidders. Meanwhile, a renovated and extended Victorian with five bedrooms at 59 Manningtree Road, which was quoted at $3.8 million to $4.18 million, drew offers from three bidders at its Abercromby’s auction before selling for $4.3 million.

Mr Woledge said these were strong results, adding that both properties were quality houses updated for contemporary living, but the absence of a heritage overlay provided an additional reason to purchase.

“The properties with heritage overlays are restrictive, and buyers are a bit tentative in the way they approach them,” he said.

At lower price points, overlays don’t have the same effect on demand.

For example, Advantage Property Consulting’s Frank Valentic attended a hot auction for a dilapidated but heritage overlay-protected timber double-fronted house at 13 Barkly Street, Richmond.

The property was marketed by Biggin & Scott as “in need of total renovation” and the auctioneer, Andrew Crotty, declared it on the market with the first genuine bid of $1 million.

Competition from the three bidders – all young couples – pushed the house $405,000 higher to a final selling price of $1.405 million.

“It was a rundown shack on 200 square metres of land, which is a fair whack of land for Richmond,” Mr Valentic said. “What explains this result is that there are not enough houses in that area and people are paying premium prices.”

Property Mavens head Miriam Sandkuhler said the inner-Melbourne market was patchy. She noted that a cottage at 46 Glover Street, South Melbourne, which was passed in on Saturday by Greg Hocking Holdsworth on a low bid of $1.26 million from the sole genuine bidder, would have fared better last year.

“A pretty Victorian bordering Albert Park would have drawn multiple bidders late last year but today the house passed in for just $10,000 more than the vendor opening bid of $1.25 million,” she said. “The two-bedroom property had strong appeal to upsizers and downsizers.”

The top house sale reported in Melbourne on the weekend was for a property at 107 Esplanade, Williamstown. It fetched $4.75 million through Greg Hocking Elly Partners, although some other properties punched higher at public auctions where the price paid was not officially revealed.

In Hawthorn’s prized Scotch Hill precinct, five bidders pushed a six-bedroom residence with a pool and tennis court to a $9.01 million sale price. The Marshall White-listed house at 42 Berkeley Street was on the market at $8.675 million and sold to a family currently based in Melbourne’s south-east.

In general, the prestige segment looks to be in better shape than the market for $1 million to $2 million houses.

For example, a period home at 24 Turner Street, Malvern East, was listed last year with a single price quote of $4 million. The property was subsequently withdrawn from sale after getting few nibbles, but on Saturday a new agent, RT Edgar, sold it at auction for an upbeat sum.

Mr Woledge said the 839-square-metre property drew an opening bid of $3.8 million, went on the market at $4.1 million and sold for $600,000 more – $4.7 million. There were four bidders.

The outcome of this auction suggests that three wounded under-bidders will be hunting for a similar standard property in the weeks ahead.

This article was originally published by CHRIS KOHLER | DOMAIN BUSINESS EDITOR | MAR 4, 2018 | domain.com.au

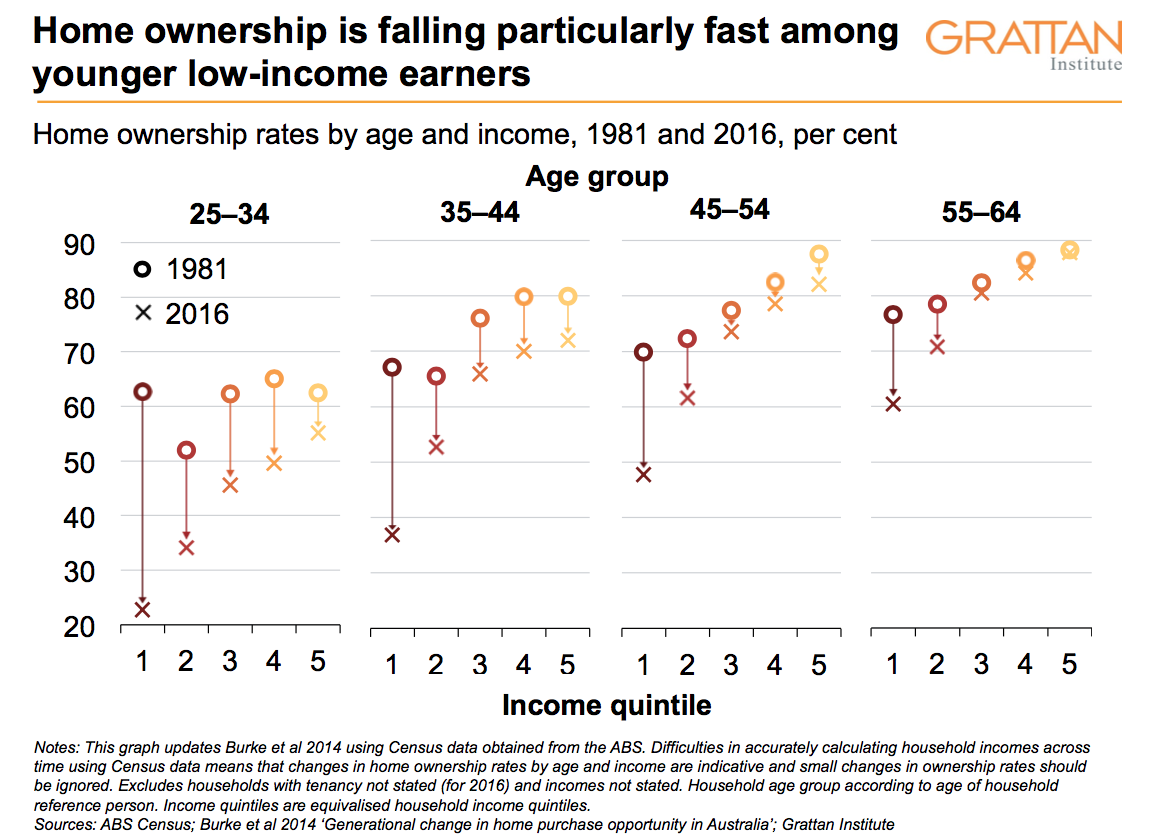

For the first time in living memory, young Australians are likely to be financially worse off than their parents, and it’s the fault of the now-extinguished house price boom.

The boom, which saw house prices in Sydney soar 83 per cent in the seven years following 2010, handed a generation of homeowners hundreds of thousands of dollars in real, untaxed gains – a windfall likely to drive a new long-lasting wedge between the rich and poor.

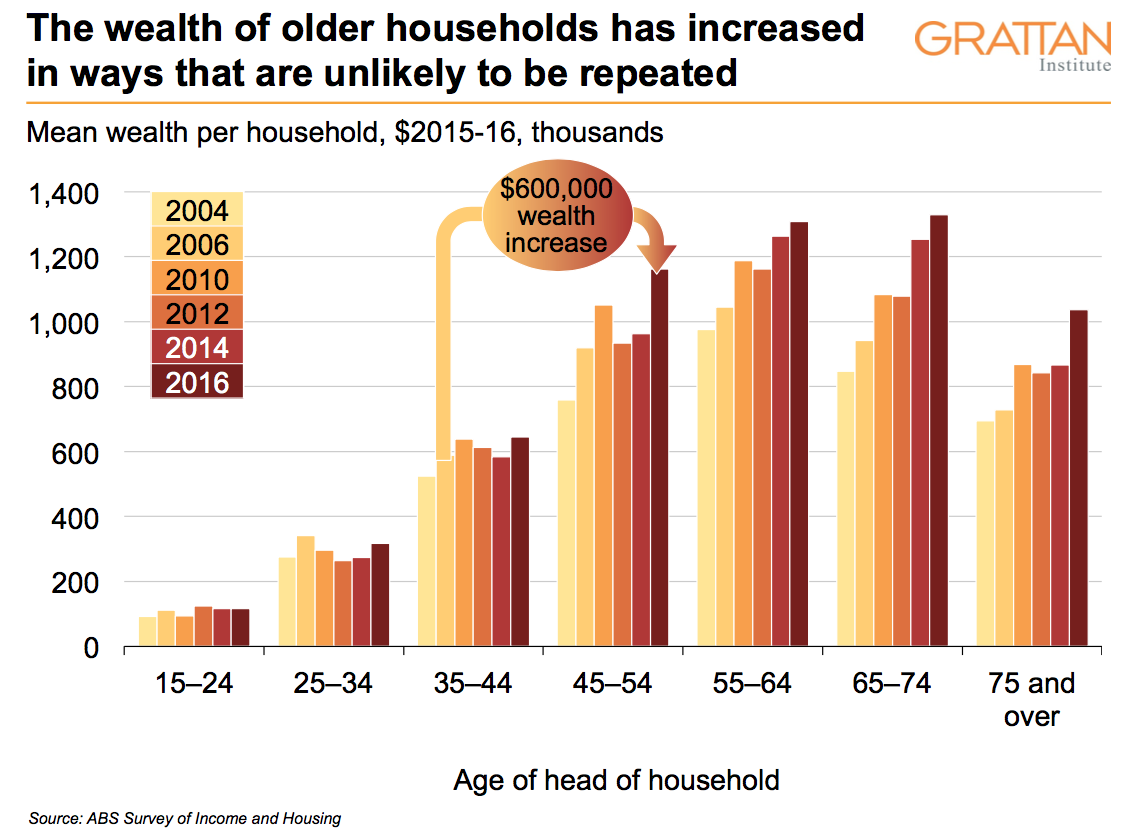

Specifically, homeowners that were 35-44 years old in 2005-06 increased their average wealth by almost $600,000 in the decade that followed, according to a new report from the Grattan Institute.

The only ones not to benefit were younger Australians.

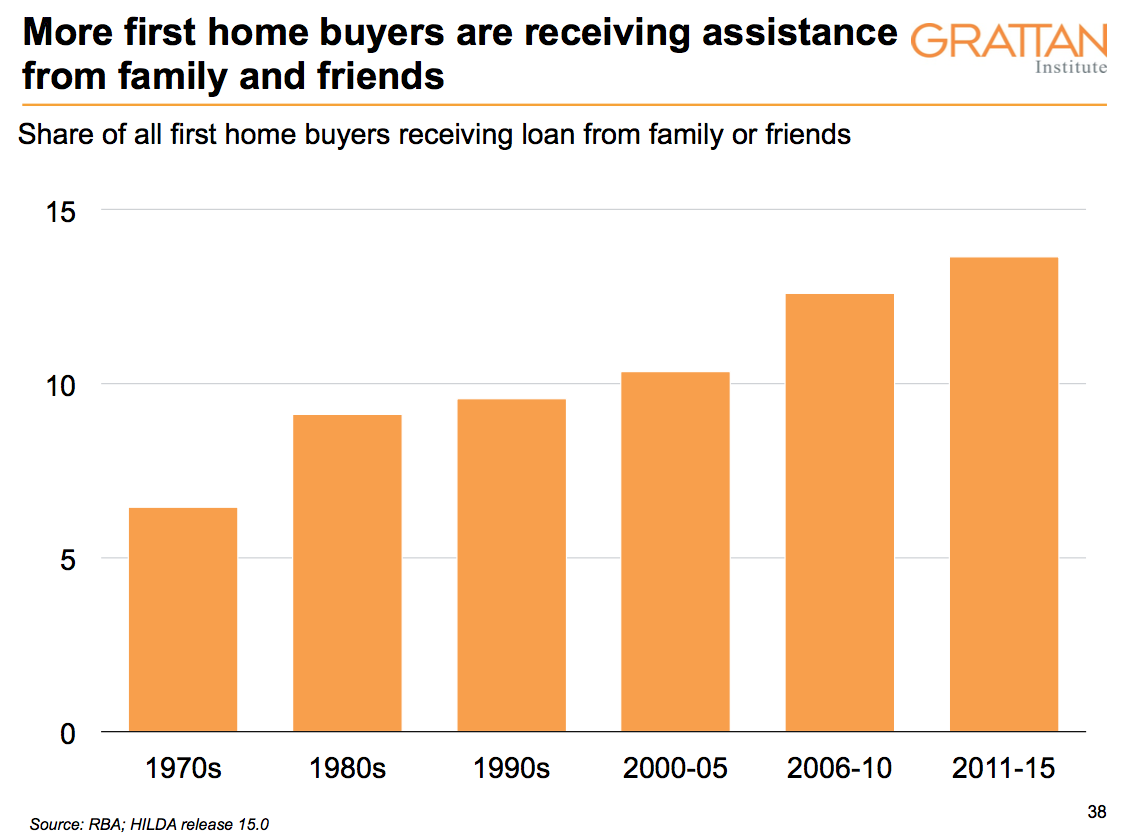

The boom in property values is now helping create a greater Australian wealth divide, the report finds, with more first-home buyers relying on their parents’ wealth than ever before.

“25-34 year old households today are no more wealthy than the equivalent households a decade before.”Grattan Institute chief executive John Daley and fellow Brendan Coates

“Older Australians are capturing an increasing share of the nation’s resources,” according to the report’s authors, Grattan Institute chief executive John Daley and fellow Brendan Coates.

“Despite the global financial crisis, 65-74 year old households today are $480,000 wealthier in real terms than households of that age twelve years ago.”

“25-34 year old households today are no more wealthy than the equivalent households a decade before.”

A central part of the soaring wealth experienced by older Australians is tied to booming house prices in Sydney and Melbourne brought on by record low post-GFC interest rates, and favourable tax settings.

“These households enjoyed a significant, untaxed windfall gain from rising [house] prices and they continue to benefit from house prices remaining high,” Mr Daley and Mr Coates wrote.

“Households that did not own property before the boom — disproportionately the younger generation — missed out on the windfall boost in wealth from the price rises.”

Relying on the bank of mum and dad

The next generation of Australian “haves” and “have nots” is now increasingly tied to whose parents were property owners during the house price boom and whose weren’t. Larger inheritances are on the way and they’ll follow family lines.

“If home ownership relies more on the ‘bank of mum and dad’, then getting a home depends more on the success of one’s parents than on one’s own endeavours,” Mr Daley said.

Australia’s wealth will become increasingly concentrated following the recent burst of wealth creation, and the amount of financial assistance able to be provided throughout the economy will differ greatly.

Hopeful first-home buyer Christopher Best and his wife wonder how far help from their parents can push the needle, given the now astronomical home prices.

The newlyweds are aiming for a modest two-bedroom property on Melbourne’s outskirts, somewhere like Cranbourne, but despite both working full time in marketing and social media management for four years, are “nowhere near being able to put together a deposit”.

“Any help from our parents would be a very significant gesture and we’d be extremely grateful, but honestly the prices are so astronomical I wonder how anyone whose parents aren’t ‘Silicon Valley rich’ can really help out.

“A 20 per cent deposit for a lot of places is now $160,000 … An enormous gift of, say, $10,000 — a fantastic gesture — is barely going to move the needle.”

Wealth versus money: Why Australians don’t feel so rich

For now, much of the gains felt by Australian homeowners remains on paper, with the wealth created doing little to ease ongoing household financial burdens.

“Things such as utility bills, health premiums and transport costs – the grudge purchases have been rising, which has had an impact,” CommSec senior economist Ryan Felsman said, adding that “anaemic” wages growth was also weighing on the minds of homeowners.

“Wages growth several years ago was in the vicinity of 3.5-4 per cent – we’re now around half that level and households feel restrained as a consequence of that.”

And with Australian households among the most heavily indebted in the world, all eyes are focused on the Reserve Bank’s plan to eventually tighten interest rates, with even a small lift expected to send shockwaves through the economy.

Vacant residential land prices are soaring in Australia, creating a mammoth headache for the nation’s housing affordability crisis.

According to latest HIA-CoreLogic Residential Land Report, the median vacant residential lot price surged by 6.5% in the September quarter of last year, hitting $267,368, up 10.9% on a year earlier.

Median prices in capital cities jumped by 7.8% during the quarter, far outpacing growth of 2.7% in regional areas.

Over the year, capital city prices ballooned to a record high of $313,74, up 12.8% over the year.

“Record population growth in Australia over the past decade has been accompanied by an economy with remarkably low and stable mortgage rates and demand for housing has grown very substantially as a result,” the report said.

“The ability of new home building activity to respond to this increased demand has been held back by insufficient supply of shovel-ready residential land.”

This, according to Australia’s Housing Industry Association (HIA), is only making the task of solving Australia’s housing affordability crisis worse.

“The high cost of new residential land is at the heart of Australia’s housing affordability crisis,” said HIA Senior Economist Shane Garrett.

“The housing industry’s ability to ramp up the supply of new dwellings as demand dictates is hampered by the inconsistency of the land supply pipeline. The time it takes for land to be made available to builders is unnecessarily long.”

Eliza Owen, CoreLogic’s Commercial Research Analyst, said the enormous increase in land prices partially reflects ongoing strong demand despite a recent softening in the east coast housing markets.

“The 6.5% acceleration in vacant residential land prices suggests strong demand, even in the context of our largest residential markets passing peak growth rates for the current cycle,” she says.

“The CoreLogic Hedonic Home value index is showing a 1% quarterly decline in capital city dwellings in the three months to January, led by the Sydney market which saw a 2.5% decline.

“Despite the softening in capital growth, land prices were driven higher by long term confidence in some Australian metropolitan markets.”

Along with strong demand, another major factor behind the increase was a sharp drop in supply with turnover falling to levels not seen in five years.

“Our preliminary estimate suggests that the vacant residential lot sales volume dropped by 10.3% during the quarter and 20.4% from a year earlier.

That largely reflected a quarterly decline of 10.9% in Australia’s capital cities, leaving the drop on a year earlier at 20.9%.

“Melbourne is Australia’s most active residential land market with preliminary figures indicating that 3,201 lots were transacted during the quarter, equivalent to over one in five (23%) of the national total,” the report said.

“During the same period, Brisbane was the second most active residential land market with 1,928 lots sold accounting for 13% of the national total, followed by Perth in third place with 1,829 transactions, or 12% of the total.

“Although Sydney has the highest volume of building activity it is only the fourth largest residential land market at 8% of the total.”

With demand strong and supply far smaller than levels seen in recent years, median lot prices rose dramatically in Melbourne and Sydney over the year, lifting by 33% and 10.3% respectively.

These are Australia’s fastest growing capitals in terms of population increase, according to latest data released by the ABS. They’re also home to the highest median house prices in the country.

“Median lot prices in both Sydney ($480,000) and Melbourne ($331,000) reached new all-time highs during the September quarter,” the report said.

Perth, at 9%, also recorded a strong increase in prices over the year, rising to $272,500.

At the other end of the spectrum, median lot prices fell in Hobart, Brisbane and Adelaide, declining 16.7%, 7.2% and 4.3% respectively to $125,000, $231,000 and $225,000.

This table from the report shows the movement in median lot prices over the past five years.

Excluding the impact of different lot sizes on offer, the median price per square meter jumped by $48 in Melbourne, $44 in Perth and $28 in Adelaide over the quarter.

Prices in Hobart, Sydney and Brisbane went in the other direction, falling $27, $11 and $1 per meter respectively.

Longer term, as seen in this next chart from the report, prices per square meter have skyrocketed over the past decade in Australia’s southeastern corner, tripling in Melbourne and doubling in Sydney, Brisbane and Adelaide.

This article was originally published by Samantha Landy on Feb 11th, 2018 via news.com.au

MELBOURNE is Australia’s equal fastest selling capital city housing market, with the typical home being snapped up in about a month.

124 Dorset Rd, Boronia sold for $737,000 30 days after hitting the market. Source:Supplied

MELBOURNE is Australia’s equal fastest selling capital city housing market, with the typical home being snapped up in just 33 days.

The city was tied with Hobart, and the pair boasted much speedier private treaty markets than the remaining Aussie capitals, according to new CoreLogic figures.

Private sales accounted for about 70 per cent of all property transactions in Melbourne, despite it being considered “the auction capital of the world”, CoreLogic state director for Victoria Geoff White said.

Mr White said rampant buyer demand was keeping Melbourne’s average days on market down, with properties in popular parts of the city commonly selling within a week.

The CoreLogic Property Pulse report revealed that at the end of 2017, properties sold privately in Australia took an average of 45 days to change hands and across the combined capitals, 40 days.

The typical time on market period was 41 days in Adelaide, 42 in both Sydney and Canberra, 47 in Brisbane, 53 in Perth and 75 in Darwin.

Melbourne’s figure had increased from a recent record low of 29 days at the end of 2016 — and the report tipped it to continue rising.

“With dwelling values now ... slowing across many cities, it is reasonable to expect that over the coming 12 months, the number of days it takes to sell a property will trend higher,” it said.

“This is likely to occur in Sydney and Melbourne, given both cities have experienced rapid rates of sale and strong growth in dwelling values over recent years.”

Mr White was more bullish about Melbourne’s private treaty market, tipping the days on market figure to remain it the low 30s for the foreseeable future.

“It won’t change that much unless something significant happens, like an interest rate rise that cools buyer demand, or an influx in supply,” he said.

23 Ararat Rd, Stawell has been on the market for nine and a half years. Source:Supplied

Vendors were also likely to be aware of Melbourne’s slowing market conditions and accordingly set “more realistic” asking prices, Mr White said.

He urged them to do so, as when properties took longer to sell, buyers became more inclined to negotiate.

Properties that lingered on the market for a long time accordingly offered good opportunities for househunters, he said: “As time goes on, you could anticipate vendors becoming motivated to consider offers outside the range they were originally willing to expect.”

The three-bedroom abode at 23 Ararat Rd has a $385,000 asking price, but its seller is open to reasonable offers.

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.