Why we shouldn't be too scared of dramatic house price drop predictions

This following article was originally published by Michael Pascoe on JANUARY 15 2018 via smh.com.au

Multibillionaire Meriton tsar Harry Triguboff has picked up this year where he left off last year, and the year before – decrying any and all moves to tighten up on foreign investors buying the apartments he churns out.

Harry talking his own book, who'd have thought it?

"Government taxes and credit restrictions have started to hit foreign buyer demand for residential property so hard in Australia that major developers are either pulling out of the apartment market altogether or, like Meriton's Harry Triguboff, are left grappling with Chinese investors who can't settle on pre-sold apartments," it says.

With an estimated wealth of $11.4 billion, I suspect Triguboff will be fine. Photo: James Brickwood

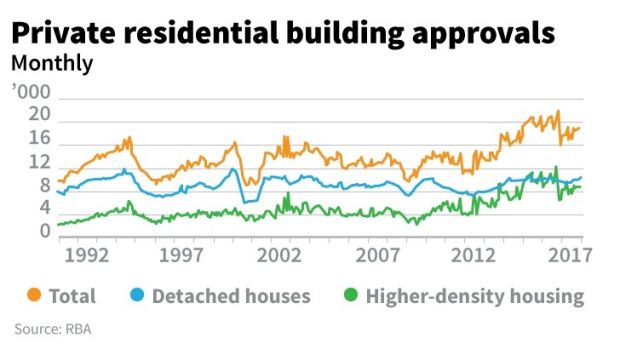

Building approvals actually peaked back in 2016. An odd surge in Footscray high-rise approvals distorted the November figures, but the completely expected pullback from unsustainable growth is in place. And not all approvals will turn into commencements.

That's the reassuring thing about the latest instalment in the multi-year saga of scary housing-related headlines.

Developers responding to reduced demand by reducing new supply means less chance of a fat overhang seriously damaging the market. Past property busts had developers going full tilt up to and over the edge.

Pulling back now means even the oversupplied markets, such as Brisbane high-rise units, could have space to clear in time given the increasingly strong domestic demand fundamentals of employment and population growth.

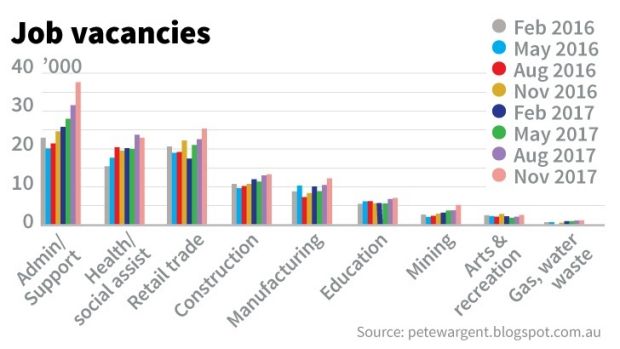

A series of graphs by property analyst Peter Wargent neatly summarises how strong this week's job vacancy figures were, including good growth in the often-maligned manufacturing and mining industries.

On the evidence, Wargent dares suggest Sydney could see record low unemployment in 18 months or so.

Not that there aren't/won't be pockets of actual house price stress, as opposed to exaggerated and highly subjective "mortgage stress" figures so loved by the doom-and-gloomers. (You know the "if rates rise 25 points we'll be ruined" stories? Most people could save more than that by comparison shopping.)

But back to Triguboff. In April 2016, he was slamming the NSW government for increasing stamp duty for foreign buyers, saying Chinese buyers were disappearing.

That was when he wasn't bagging local councils for stopping him building more apartments and criticising the Reserve Bank and Australian Prudential Regulation Authority for tightening up on local banks' lending to foreign buyers.

By the end of the year, all was again well with Meriton's outlook, aside from "idiots" on councils not approving his projects quickly enough.

Five months later, Triguboff said apartment prices were weakening and he would finance about $200 million of the $1.4 billion of apartment sales he expected to make in 2017 thanks to local banks' policies and Beijing's crackdown on money leaving the country.

In July, there was another slowdown after another NSW stamp duty hike but Triguboff said demand was slowly shifting to local buyers.

"The problem with Australians is they are very slow," he told the AFR. "They ask their lawyer, they ask their financial adviser, they ask their family, they ask everybody. The Chinese don't ask anybody, they come off the plane, buy their unit and go."

But now it seems Meriton has problems with some of those hot-off-the-plane-and-plan buyers.

"Many of the Chinese can't settle," he said in the AFR earlier this month.

"So now we have to resell them – there is another problem. And everyone thought that the Australian buyer would come in when the prices started coming down – they haven't – I knew they wouldn't – it wouldn't make any sense if they did."

With an estimated wealth of $11.4 billion, I suspect Triguboff will be fine, and Meriton more than capable of riding the market's ructions.

For a correction of some parts of the market to turn into a housing crash, the usual requirements are one or more of a sharp rise in unemployment, a sharp rise in interest rates or a fall in population.

The multi-year housing bears continue to be denied all three, but have seized on the idea of the "IO cliff" – the bunch of interest-only loans that the authorities are pressuring banks to turn into principle-and-interest to ensure the stability of the financial system.

That comes with a consequent jump in monthly repayments, mainly for speculators who have been betting on rapid capital growth continuing.

Kevin Young, founder of Queensland's Property Club (previously called The Investors Club) had said: "We're advising our members to get themselves into conflict with their bank, to say they can't afford principal and interest repayments without ending up in financial stress.

"Most of the time, the bank will acquiesce."

Through the usual seminars and such, Property Club markets property for developers to "members" with inhouse brokers and service providers helping with the details.

When property prices are soaring and property investment is touted as a sure way to wealth, well, a rising tide lifts all boats. When the price of marginal new properties doesn't rise and 20,000 customers have been encouraged to take IO loans during sales seminars, gee, what could go wrong?

Fortunately, for the broader market, it doesn't look as bleak as the local UBS office likes to paint it. With the banks now well under their IO ceiling and cheaper rates available by shopping around for P&I, the "cliff" is more likely to be a hill. But don't let that get in the way of a scary story.

In February 2017 I predicted that Melbourne real estate median price appreciation would increase by 12 to 13 per cent. My prediction was recorded on the YouTube video below;

(Just fast forward to 39:30 sec to the actual prediction, or watch the entire video from the beginning to the end to understand the justification for my opinion.)

(Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.)

And guess what, recent official RP Data figures come out with 12.1% for Dec 1st 2017...

When I am right, I am right...

Would you like to know my predications for 2018 and beyond?

And more importantly which suburbs in Melbourne will rise far beyond the average and which will fall in value or move sideways, then join me and 40 like-minded property investors at the very first Real Estate Fast Track Weekend for 2018!

Seats are strictly limited so book NOW in order to avoid disappointment...

Investing in yourself may be the most profitable investment of your life!

Yours in success,

Konrad Bobilak

This article was originally published by Scott Carbines on JANUARY 6, 2018 via news.com.au

TRADITIONAL Melbourne battler suburbs are tipped to be some of the strongest performing for growth in 2018.

Broadmeadows, Frankston North, Epping, St Albans, Lalor and West Footscray are among the areas real estate experts expect to excel this year, as buyers scramble for affordable homes.

Real Estate Institute of Victoria president Richard Simpson said the best options remained in the city’s north and west after a widespread price boom in recent years.

21 Glamis Rd, Footscray, is on the market for $1 million. Source: Supplied

“Given increasing buyer demand for areas that offer value, suburbs yet to reach the citywide median house price are best placed to experience strong price growth in 2018,” he said.

CoreLogic attributed a median value of $832,735 to Melbourne houses in December.

Mr Simpson tipped north and western suburbs Albion, Ardeer, Broadmeadows, Epping, Mill Park, Albanvale, Doreen and Taylors Lakes to lead the charge this year.

“With the median house price in Melbourne’s middle ring tipped to break $1 million next year, Taylors Lakes provides a more affordable alternative without really needing to compromise on proximity to the CBD,” he said.

The suburb, 23km north west of the city, had a median house price of $690,000 after a 14 per cent boost in the 12 months to September, according to CoreLogic.

Suburbs forecast to have a big year, based on 2017 growth and tips from experts. Source:Herald Sun

Frankston North and Bayswater North, surrounded by suburbs with higher median house prices, were also flagged as ones to watch by Mr Simpson.

LJ Hooker, Frankston, agent Nancy Nugent said Frankston’s North affordability, transport links to the city, proximity to the beach and schools were among its drawcards.

The suburb was one of 2017’s strongest performers for growth, with the median house price rising 34.4 per cent to $437,500 in the 12 months to September, CoreLogic data shows.

Realestate.com.au chief economist Nerida Conisbee said user activity on the site showed “a big push to the west” and notably to Kensington (median house price $1 million).

“It’s very close to the city, it’s got a lot of period homes. It’s far more affordable than if you went to the north, east or southeast,” she said.

WBP Group executive chairman Greville Pabst flagged nearby Maidstone and West Footscray as other hot spots as buyers searched for affordable homes close to the city.

He said Cheltenham would also be boosted by the new train station at Southland.

358 Findon Rd, Epping, is on the market for $570,000-$620,000. Source:Supplied

Lisa and Jarrod Richardson are selling the three-bedroom house they renovated at 21 Glamis Rd, West Footscray, with price hopes of $1 million.

“Our neighbourhood is amazing,” Ms Richardson said.

“It’s very community-based, despite how close we are to the city, everyone is willing to help each other and that’s what we love about it.”

Hocking Stuart, Yarraville, agent Adam Welling said demand in the suburb, just 7km from the CBD, was driven by families.

“It seems ridiculous to say but $1 million is an affordable family home now,” he said.

Advantage Property Consulting director Frank Valentic said Mornington Peninsula suburbs including Rosebud, Dromana, McCrae and Capel Sound also still offered great value for money, alongside suburbs in the middle west and north.

Ray White, Epping, agent Vanny Bains said the suburb had attracted high demand from investors and homebuyers over the past two years.

“Numbers have increased dramatically from interstate investors and there’s very high demand from first-home buyers in the area,” he said.

Mr Bains said the four-bedroom house at 358 Findon Rd, Epping, would draw first-home buyers and investors. It has a price guide of $570,000-$620,000.

New infrastructure projects are a key factor driving up the value of houses in suburbs around the country but they are often ignored by property investors.

Property valuer and analyst Suburbanite's Anna Porter has looked at six areas where there is either new infrastructure being built or recently completed that she expects will help continue to drive rising property values.

1. Adelaide

Adelaide is benefiting from multiple major investments in infrastructure, which will more than compensate for the downturn in manufacturing in recent times Ms Porter says.

The number of big projects is impressive. They include expansions to the Adelaide airport, based on the government's 30-year master plan, which require $1 billion to be spent in the next five years.

There are also upgrades to Adelaide Riverbank, a $1 billion redevelopment encompassing 380 hectares around the River Torrens that coincides with the Adelaide Oval upgrade, consisting of three key precincts; the health and wellbeing precinct, the core entertainment precinct and the cultural and education precinct.

Then there is the new Royal Adelaide Hospital, located close to Adelaide's CBD which was completed in early 2017. And on top of all that Adelaide is to be the hub for Australia's future submarines construction contract.

The most recent data from outgoing SA Defense Chief Andy Keough reveals that there is an anticipated job creation of around 6000 to Adelaide off the back of this project.

2. Liverpool, NSW

Sydney broadly has certainly had its fair share of property growth and new infrastructure projects - think of the future around Badgery's Creek in the far west of Sydney where a new airport will be built.

That has been a lottery win for "poor man's acreage". But slightly closer to the city around Liverpool in Sydney's south west are also going from strength to strength with new projects such as the Moorebank Intermodal.

The construction of an intermodal freight terminal and port shuttle operation to and from Port Botany is set to deliver more than $11 billion in economic benefits and the creation of around 6,800 jobs, according to Moorebank Intermodal Company.

Ms Porter says that such investment has seen the property market in the local council area of Liverpool rise by 12.88 per cent according to Corelogic, for the 12-months to July 2016: (the period just after the commencement of the project).

"Such growth puts Liverpool in standing with markets closer to Sydney CBD such as the Inner West and Eastern suburbs."

3. Gold Coast

The Gold Coast has traditionally struggled to keep pace with Brisbane's growth rates, but infrastructure required for hosting the Commonwealth Games has created a construction boom.

Like Sydney CBD's light rail project the Gold Coast had to recently endure the havoc such infrastructure creates on retailers and business.

However the Gold Coast's light rail project has revived properties along its route. But the light rail was just one of a number of infrastructure projects for the Gold Coast.

There are also the Pacific Motorway upgrade, at a cost of almost $3.8 billion; the Gold Coast Rapid Transit system, at $1.8 billion; and a planned extension of the rail link from Varsity Lakes to Coolangatta, costing $1.2 billion.

Infrastructure relating to health services includes the $1.76 billion Gold Coast University Hospital and the Griffith University Health Centre at $150 million.

"This past 12 months has seen the Gold Coast outstrip Brisbane growth by a 1.62 per cent differential to the 12-months to July 2017.

4. Brisbane CBD

For the Brisbane CBD there is something in the order of $12 billion in "city-shaping" major projects slated or underway.

It is part of the reason why the Singaporean government's sovereign wealth fund, GIC just bought, through Charter Hall, an office tower for $370 million despite the city's office vacancy now well above historical highs.

The projects include Destination Brisbane Consortium's development of the Queen's Wharf worth about $3 billion.

The nearby mixed use Brisbane Quarter is also under construction and there are potential additions such as the highly politicised Cross River Rail project.

"A massive revamp of Brisbane's CBD is set for completion in six years," Anna Porter says.

5. South East Melbourne

South East Melbourne has seen significant infrastructure by way of transport benefiting the likes of areas such as Dandenong and Frankston.

"Upgrades to transport from the Melbourne CBD to the area has seen a significant rise in buyers moving from the inner CBD locations to these outer areas," Suburbanite's Anna Porter says.

The big projects there include the Eastlink Freeway, which opened in 2008 and starts at Carrum Downs, connecting to the existing Monash Freeway, allowing for a 35 minute commute to the CBD.

The 2013 opened Peninsula Link Freeway, now connecting the Eastlink and Monash Freeway, allows access to both CBD and lower bayside suburbs.

The $115 million Bayside Rail Project, too, has provided easier and faster access to the south eastern suburbs of Melbourne.

There was also the construction of the $80.9 million Stage 3 development of Frankston Hospital completed and officially opened by the Minister for Health in early 2015.

"These projects have helped Frankston experience 19.5 per cent average growth for the 12-months to July 2017, outstripping nearby Port Phillip Council in Melbourne's inner metro for the same period, at just 11.15 per cent."

6. Geelong

Despite the winding down of car manufacturing, Geelong is being looked after with several big new projects.

"Geelong has gone from being the laughing stock of Melbourne," Ms Porter says, "The council went into administration, but Geelong has become one of the powerhouses of the Australian property market."

Geelong has seen its fair share of major projects including the major upgrade to Geelong Hospital, receiving funding from both the Federal and State government to the tune of $128 million.

Collaborative partnerships have also created several major projects worth about $2 billion in new investment to the region including the $1 billion Avalon Freight Precinct which will become Victoria's largest, lowest cost interstate seaport, road and rail freight terminal.

There is a $600-$800million high-security water infrastructure spend that will "drought-proof" the region; a $300 million investment at CSIRO's animal health laboratory in Geelong and an injection of $70 million into Deakin's Carbon Nexus research centre will further drive opportunity for the region.

This article was originally published by Scott Carbines on JANUARY 4, 2018 via news.com.au

MELBOURNE’s median house asking price has hit $1 million for the first time. The figure marks a surge of 27.8 per cent from the same time last year, according to SQM Research.

Buyers searching for an average home in Melbourne are being faced with a seven figure price tag for the first time.

Sellers are demanding a $1 million price tag for their homes, with the median asking price now reaching record levels.

The figure, $1,000,300 from all currently advertised properties, marks a surge of 27.8 per cent from the same time last year, according to SQM Research.

It comes amid tighter stock levels across the traditionally quiet Christmas and New Year period, with 28,895 residential properties listed in Melbourne in December.

That’s a decline of 10.3 per cent on the same time last year and 12.6 per cent from November.

Melbourne property listings are tipped to grow in 2018. Source:istock

The median asking price for Melbourne units was $528,100 for the week ending January 2 — a 15 per cent annual rise.

SQM Research managing director Louis Christopher said the group predicted property price growth of 7-12 per cent in Melbourne this year and the city’s listings to grow in 2018.

“Melbourne has a year-on-year decrease (in listings) and we are still of the belief this is just a temporary stay and Melbourne will continue its ongoing strength, which is also reflected in the median house asking price, which has now reached $1 million,” he said.

“We’re still relatively positive on Melbourne because of the very strong population rates the city is experiencing now, which, combined with a booming local economy, is assisting the housing market in terms of recording rising prices and numbers vendors can feel very confident about.”

SQM Research managing director Louis Christopher. Source: Supplied

Mr Christopher said Melbourne’s stock levels could be boosted by vendors motivated to sell by signs of a slight slow down in the market.

“The market may well slow down in the first half of the year but we don’t think it’s going to last for the full year,” he said.

Australia’s median house asking price rose 11.3 per cent year-on-year to $567,800, while the median unit asking price rose 7.9 per cent to $374,500 for the week ending January 2.

This article was originally published by Nathan Mawby via news.com.au | DECEMBER 19, 2017

MONSTER sales with eight-figures price tags have dominated the top of the Stonnington property market in 2017. Take a look at some of Melbourne’s biggest earners.

ALL eyes have been on the top end of Stonnington’s property market since an almost $40 million record sale in Toorak halfway through the year.

The off-market deal for 18 St Georges Rd shattered the record for any Victorian house sale to date.

And RT Edgar Toorak’s Jeremy Fox said the past 12 months in Toorak’s top end had been as strong as the interest in the record-breaking sale by his agency.

18 St Georges Rd, Toorak, rewrote Melbourne’s property record books in 2017. Source:Supplied

“I think it’s had the best year it’s had for a long time,” Mr Fox said.

The St Georges Rd sale topped Toorak’s previous record holder, 9 Towers Rd, by about $13 million.

The former Besen family home at 9 Towers Rd, Toorak, was the suburb’s prior record holder. Source: Supplied

Morell and Koren director and high-end buyer’s advocate David Morell said 18 St Georges Rd was the highlight of what had been an “interesting” year.

However, he added that it would have hampered some other high-end sales in the area as owners of illustrious properties raised their asking prices.

“You will get this lag from St Georges Rd, the people there will think there home is worth quite a bit more,” Mr Morell said.

He said one of the few top sales in the suburb this year not affected by the result at No. 18 St Georges Rd, was the $16.8 million deal signed for 2 Rostil Court in March.

The six-bedroom house spread over four storeys, came with a pool and tennis court, plus a home theatre and impressive views across the suburb.

Later in the year, celebrity chef Shannon Bennet and actor wife Madeleine West are also believed to have splashed about $16 million on a Lansell Rd, Toorak, house, and sold their 38 Cromwell Rd home in South Yarra for close to $10 million.

2 Myvore Court, Toorak, was one of the year’s most unusual top-end deals. Source: Supplied

Sales records show it achieved $16 million the second time around.

“Myvore was the weirdest of the year,” Mr Morrell said.

Mr Fox said with a number of big prices in Toorak this year it was possible the suburb’s new record could be broken again in the coming year, but he did not expect it would be bested by such a margin.

“The market is very strong, so it could be soon,” Mr Fox said.

“I think the next record to be broken will be $40 million plus, but in the $40 million range somewhere.”

He said the strength of the market, which had added several eight-figure addresses to Stonnington’s streets in 2017, had set other benchmarks as well.

He pointed to the sale of a 606sq m block at 22 Lansell Rd, Toorak, for $6.4 million.

It worked out to $11,000 a square metre.

“That’s the highest price paid for land in Toorak,” he said.

Mr Morell said the price per square metre was the real litmus test for quality properties at the top end in Toorak.

“This time last year I was paying $6500-$7000 (a square metre) for reasonable blocks,” he said. “And in the past 12 months it’s up to $10,000 per square metre.”

10 Hampden Rd, Armadale, sold for $7.8 million and was one of the bigger sales outside of Toorak. Source: Supplied

Elsewhere in the municipality, CoreLogic records show high prices were paid in South Yarra, where a $13.8 million sum for 125-133 Walsh St added another eight-figured address to the vaunted street.

33 Grant St, Malvern East, sold for $6.125 million in October .Source: Supplied

Sales records also showed a handful of hefty sums paid in other suburbs including the $7.8 million splashed on 10 Hampden Rd, Armadale, on November 25.

Even Prahran and Windsor, the municipality’s most affordable suburbs, had some sizeable results.

The biggest recorded by CoreLogic was the $4.47 million sale of 52 The Avenue.

52 The Avenue, Prahran, picked up $4.47 million in March, 2017. Source: Supplied

This article was originally published by Samantha Landy via news.com.au | DECEMBER 17, 2017

MELBOURNE homeowners earned more than $4.6 billion in property profits in the September quarter, with fewer than 1 per cent of houses reselling at a loss in the city.

CoreLogic’s latest Pain & Gain report reveals Boroondara, Whitehorse and Monash were the most profitable property markets by value in the period, while heavy apartment development fuelled losses in parts of the inner city.

The data largely paints a positive picture for homeowners in “powerhouse” Melbourne, revealing 99.2 per cent of houses sold in the three months to September 30 earned more than their owners originally paid for them.

This was the highest proportion of the nation’s capitals, edging out Sydney (98.3 per cent) and Hobart (97.4 per cent).

18 Massey St, Box Hill South sold for $1.445 million in August, making a substantial profit on its previous transaction for $818,000 in 2013. Source:Supplied

CoreLogic head of research Cameron Kusher said the data highlighted the strength of Melbourne’s near-bulletproof house market in recent years.

But it was a different story for the city’s units and apartments — the report found one in ten resold at a loss in the quarter.

“That figure is starting to fall, but it’s still a lot higher than what it is for houses,” Mr Kusher said.

“We’ve seen capital growth lagging behind in units. That’s the driving force behind the city’s weaker markets like Melbourne (CBD), which is almost dominated by units.”

About a quarter of CBD dwellings sold in the three months to September 30 earned less than their vendors had paid for them, equating to a total loss of $8.47 million at a median of $40,507 per sale.

High proportions of homeowners in Stonnington (16.9 per cent) and Moonee Valley (11.2 per cent) also experienced pain, making $2.88 million and $2.72 million in total losses respectively.

Mr Kusher said these deficits were largely driven by an influx of off-the-plan apartment projects creating oversupplied markets in these areas.

On the flip side, every single home sold in the Mitchell, Moorabool and Murrindindi council areas in the September quarter made a profit.

Boroondara sellers made the biggest total windfall by value — a combined $281.4 million — followed by Whitehorse ($266.48 million) and Monash ($239.3 million).

Bayside vendors scored the highest median profit of $615,000 per sale.

Melbourne houses that were held for 8.5 years and units for 7.5 typically enjoyed price gains, while average hold periods for a loss were 3 and 6.1 years respectively.

Just 1.8 per cent of owner-occupiers sold properties at a loss compared to 6.4 per cent of investors.

This article was originally published by Brendan Casey via Herald Sun Real Estate | DECEMBER 1, 2017

MELBOURNE continues to defy a national property market downturn, new figures show.

The Victorian city was the only mainland capital to see growth in the property market in November.

CoreLogic’s latest Hedonic Home Value Index revealed Melbourne home values continued to nudge higher last month, albeit at a slower pace than a year ago.

Melbourne’s homes values grew 0.5 per cent, compared to a 0.7 per cent fall in Sydney in November. Combined capital city values dropped -0.1 per cent last month.

Melbourne home values recorded relatively steady growth over the past three months, rising

1.9 per cent.

“The stronger performance for Melbourne relative to Sydney can be attributed to a number of factors,” CoreLogic head of research Tim Lawless said.

“Melbourne’s market has a healthier level of housing affordability, a lower concentration of investment activity over recent years and higher rates of net migration.”

CoreLogic head of research, Tim Lawless.Source:News Corp Australia

Despite bucking the national trend, Melbourne’s rate of growth has lost steam on an annual basis, slowing to 10.1 per cent annual growth from a recent peak of 13.1 per cent in July this year.

Nationally, home values fell 0.1 per cent, pulled down by Sydney, Perth and Darwin.

Gross rental yields have also drifted to a new record low across Melbourne, sitting at 2.88 per cent.

Highlights from the CoreLogic Hedonic Home Value Index

Best performing capital city: Hobart +3.3 per cent

Weakest performing capital city: Darwin -2.7 per cent

Melbourne’s property market is showing no signs of slowing down in the lead-up to Christmas, with the city recording its second-highest number of auctions for the year over the past week.

Almost 2000 properties went under the hammer, 200 more than this time last year: 64.7 per cent were sold at auction.

CoreLogic commentator Kevin Brogan said the rise in auction volume demonstrated a typical “rush to the finish line” for the end of the year.

“We often see a headlong rush towards the new year, with people wanting to be in their new home by Christmas or wanting a new property for the new year,” Mr Brogan said.

Geelong, southwest of Melbourne, recorded the week’s highest preliminary clearance rate of 83.87 per cent from about 80 auctions.

Auctions were down in Sydney, its softening market reflected in auction volume and clearance rates. It had 990 auctions last week, 150 fewer than the previous week, with a clearance rate of 58.7 per cent.

CoreLogic data shows 26,000 properties currently advertised for sale in Sydney, a 19.6 per cent rise on property listings advertised this time last year.

Perth had a clearance rate of 46.7 per cent across 62 auctions.

Canberra remains resilient, with 66.7 per cent of properties sold from 84 reported results,

Adelaide remains steady with clearance rates in the mid-60s. Brisbane returned the lowest results this week, with 46.6 per cent successful sales from 131 auctions.

This article was originally published via abc.net.au | Dec 10, 2017

One in three Melbourne suburbs now have a median house price of at least $1 million, and the once-affordable outer suburbs are also on the rise, according to Victoria's leading real estate body.

The latest data from the Real Estate Institute of Victoria found 90 per cent of suburbs within 10 kilometres of the CBD and almost half of suburbs in the middle ring — between 10 and 20km — are now in the million-dollar club.

Ten years ago only three middle-ring suburbs had a seven-figure median price.

REIV president Richmond Simpson said 154 of Melbourne's 402 suburbs recorded a median house price of $1 million or higher.

A staggering 44 suburbs made the jump in 2017, including Mordialloc on Melbourne's bayside, Kingsville in the inner west, and Coburg in the north.

"Ninety per cent of suburbs in the inner ring have a median house price of over a $1 million, that's what you sort of expect," he said.

"Suburbs such as Moorabbin, Craigieburn, Narre Warren North, those types of suburbs, they're the ones we're seeing the best price growth."

Clayton, 19 kilometres south-east of the city, had been a standout according to Mr Simpson. Its median house price increased 210 per cent over the last decade — now at $1.3 million.

"We've had unprecedented growth in real estate prices over the last 10 years, but more particularly in the last few years," he said.

"It's mainly driven by low interest rates and also high population movements to Melbourne from interstate and overseas that's put pressure on housing."

With Melbourne's population still growing at a strong rate, the REIV said it's likely more suburbs will join the million-dollar club.

"And we'll see the price in the outer suburbs coming up towards that $1 million. Suburbs in that middle ring, people can't afford those anymore, so what we're seeing is a lot more competition in the outer ring."

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.