Melbourne land values surge while Sydney tops $1000 a square metre

This article was originally published by Nicole Lindsay via smh.com.au on Oct 24, 2017.

The median price for an Australian housing lot increased 8.5 per cent to $256,683 in the June quarter, an all-time high for vacant residential land, according to the HIA-CoreLogic Residential Land Report.

The price of residential land in Sydney has reached a record high of $1051 a square metre, setting a new benchmark for land values.

While Sydney median prices increased 9.8 per cent over the past 12 months, prices in Melbourne surged 19.6 per cent.

Melbourne land now costs $677 a square metre while Perth land commands $730 a square metre.

In the past 10 years, Sydney prices have increased 83 per cent but Melbourne land soared 159 per cent in the same 10-year period, according to the report.

HIA senior economist Shane Garrett said "the speed at which land price is increasing is a concern as it compounds the housing affordability problem".

CoreLogic's commercial research analyst Eliza Owen said "record-high lot prices over the past five quarters are likely to have contributed to worsening affordability and influenced the unprecedented level of high density developments under construction".

The report shows the volume of sales slowed in the past year, but turnover is picking up. The number of sales increased 13.1 per cent to 17,830 in the June quarter - but that figure remains 8.7 per lower than a year ago.

Nearly two-thirds of residential land transactions take place in capital cities, but regional areas account for 37.7 per cent.

The report found Melbourne is the most active market recording 21 per cent of all sales in the June quarter, with Sydney's more expensive environment yielding 10 per cent of the total deals.

Danni Addison, Victorian chief of the Urban Development Institute of Australia said prices will continue to rise "unless there's a big boost on the supply side of the equation".

"Demand isn't dying down, so we will continue to see increasing prices across the market unless there's a big boost on the supply side of the equation," Ms Addison said.

"There's a critical issue with housing production timeframes, which desperately need to be streamlined so industry can bring more housing to market at a pace that can meet demand," she said.

The least expensive land markets are found in South Australia and Tasmania. Hobart also boasts the largest average lots, at 669 square metres and land costs just $196 a square metre - an increase of 28 per cent since 2007.

Sydney, despite being the most expensive land market in Australia, also offers the second largest average lot sizes at 470 square metres, trailed by Brisbane at 448 square metres.

Land in Brisbane costs $563 a square metre, trailing slightly behind Adelaide which recorded land values of $602 a square metre.

Red-hot house prices in Melbourne's inner-north have forced one of the area's federal MPs to find a cheaper place to live.

Federal MP for Wills Peter Khalil says he and his family were "effectively priced out" of Brunswick, after they were given notice to vacate their rental property, despite having a pre-tax annual household income of more than $200,000.

The Labor backbencher says the "stressful experience" of the forced move has highlighted the plight of local renters and would-be home owners who are not lucky enough to enjoy six-figure incomes.

Mr Khalil is not alone in being overwhelmed by the cost of living in Brunswick where median house prices have soared from $860,000 in 2016 to $1.06 million this year, according to the latest data from Domain.

The news is not good for renters either with the median weekly price of a 3-bedroom house in the area now at $650.

The MP told Fairfax Media he was notified in August that his landlord wanted the Khalil family out of Stewart Street rental so the house could be put on the market.

"We tried to contact the owners to see if they were interested in selling, rather than us moving with two little kids," Mr Khalil said.

"That's when they came back and said they were looking for something like $1.9 million and my jaw just hit the floor; there was no way we could go near that."

Mr Khalil said he thought his MP's salary would allow he and his wife, who works part-time, to buy a new house without having to move too far.

He was wrong.

"We could not get near any of the properties for sale in Brunswick," Mr Khalil said.

"I was shocked that with this fantastic salary that an MP gets, we couldn't get into that market.

"We could not get near any of the properties for sale in Brunswick.

"It's a decent salary and I've got no complaints, but the bank is just not going to lend you enough, on that salary, to afford that price.

"Effectively we were priced out."

Eventually, with a little help from his parents, Mr Khalil was able to buy a property in the more affordable Pascoe Vale end of his electorate, but says the episode gave him an idea of the impact of Melbourne's affordability crisis.

"It highlights for me in a very literal way, how hard it is for young families to get into the market these days," he said.

Tenants Union of Victoria spokesperson Devon LaSalle said many residents of the inner-suburbs earning low or modest incomes had a choice: move further away from the city or face serious housing stress.

"Unfortunately what happens to a lot of renters is that the prices go up and they get priced out of the market," Ms LaSalle said.

"A lot of these people are paying in excess of 30 per cent of their incomes on rent – that's the threshold for being under housing stress.

"We're gonna see more and more people in those inner-city areas who are under housing stress and that's a problem."

This article was first published by Scott Carbines via news.com.au on 2o Oct 2017.

MELBOURNE’s median house price increased by its lowest quarterly amount in almost two years in a positive sign for first-home buyers.

A flood of sales at the affordable end of the market moderated growth to just 0.7 per cent in the September quarter, according to the Real Estate Institute of Victoria, which recorded a citywide median of $817,000.

Vendors in some of Melbourne’s traditional battler suburbs have received a boost from the rush for affordable properties.

Sunbury (14.5 per cent), Lalor (12.8 per cent) and Broadmeadows (9.7 per cent) were among Melbourne’s top 10 for median house price growth in the September quarter.

Dromana (15 per cent), Balwyn North (13.8 per cent) and Ringwood East (13.2 per cent) were other top performers.

REIV acting president Richard Simpson said 44 per cent of sales during the three month period were below $600,000.

This is the cut off point for the full first-home buyer stamp duty concession introduced by the State Government in July.

The Delaney family sold their Sunbury home in just two days. Picture: Jay Town Source:News Limited

“These incentives have certainly worked, with first-home buyers accounting for 18.3 per cent of all new home loans in August — the highest since September 2013,” Mr Simpson said.

“Despite the moderation, the market remains strong with the Melbourne median house price up a remarkable 14 per cent on the same period last year.

“We’re also seeing buyer demand continue to outstrip supply and a high level of vendor confidence.”

Leading Real Estate agent Adam Sacco said Sunbury houses were selling in just a few days with “seven out of 10 buyers” coming from out of area.

“There’s a $150,000 difference compared with the surrounding suburbs’ median price to Sunbury,” he said.

Jason and Jacqui Delaney’s three-bedroom Birkdale Court, Sunbury, home fetched $476,000 — about $40,000 more than the agent’s expectations — after seven offers at the first open for inspection.

Mr Delaney said the family “couldn’t be happier” at the quick result.

Advantage Property Consulting director Frank Valentic said tougher lending conditions for investors had also helped cool the Melbourne market and give first-home buyers an edge.

“First-home buyers are definitely getting a bit more opportunity now because investors have dropped off, and first-home buyers have picked up that slack under $750,000,” he said.

Melbourne’s median apartment price fell for the first time in six quarters, down 2.5 per cent to $587,000. House prices in regional Victoria increased for the third consecutive quarter, up 1.2 per cent to $385,000.

TOP GROWTH SUBURBS — SEPTEMBER QUARTER

Dromana, 15 per cent to $790,250

Sunbury, 14.5 per cent to $518,000

Balwyn North, 13.8 per cent to $2.105 million

Ringwood East, 13.2 per cent to $1.03 million

Lalor, 12.8 per cent to $682,500

Diamond Creek, 11.9 per cent to $813,100

Bentleigh, 11.8 per cent to $1.61 million

Richmond, 10.8 per cent to $1.442 million

Eltham, 9.8 per cent to $945,000

Broadmeadows, 9.7 per cent to $595,000

Source: Real Estate Institute of Victoria (minimum 30 sales)

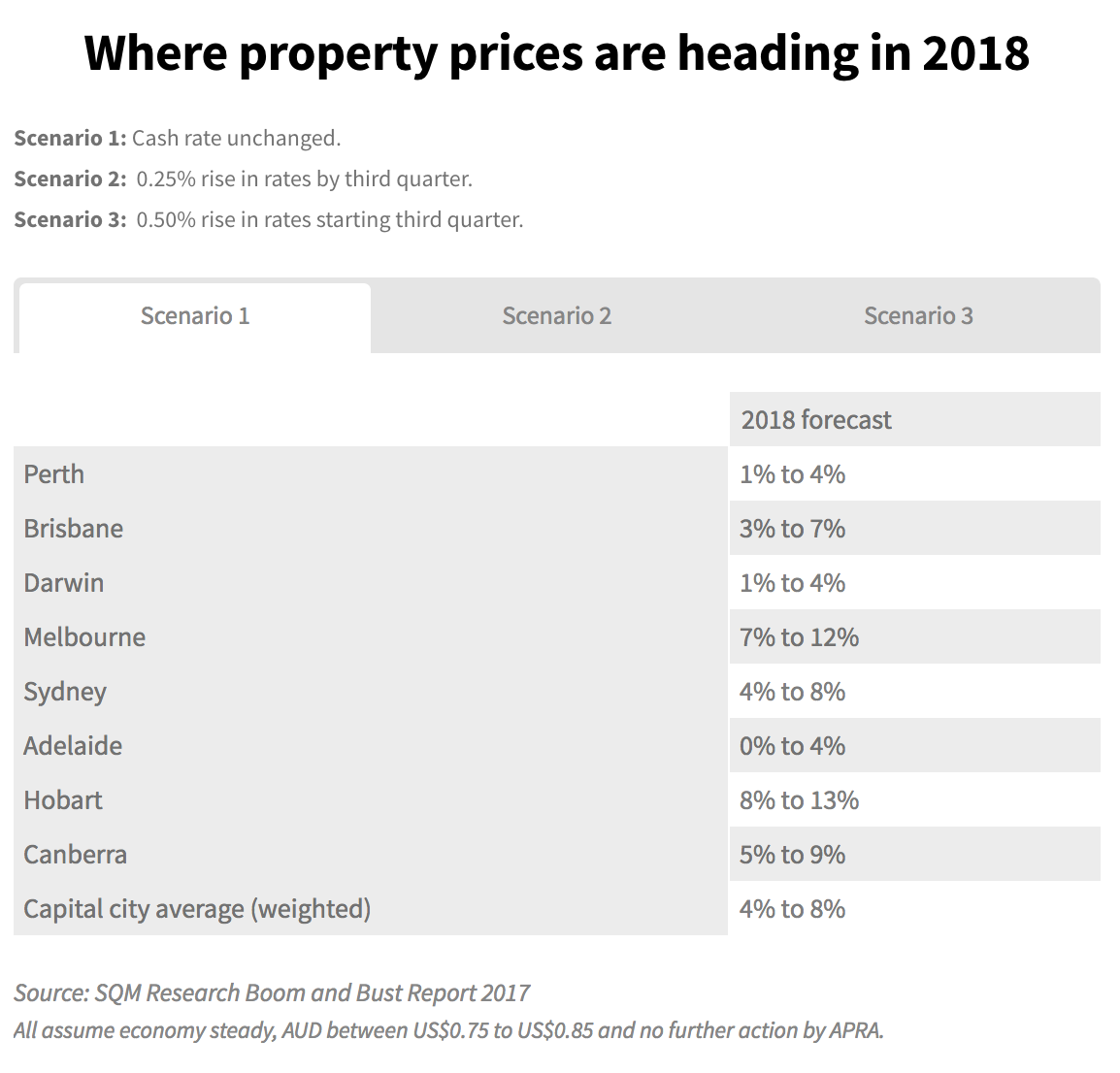

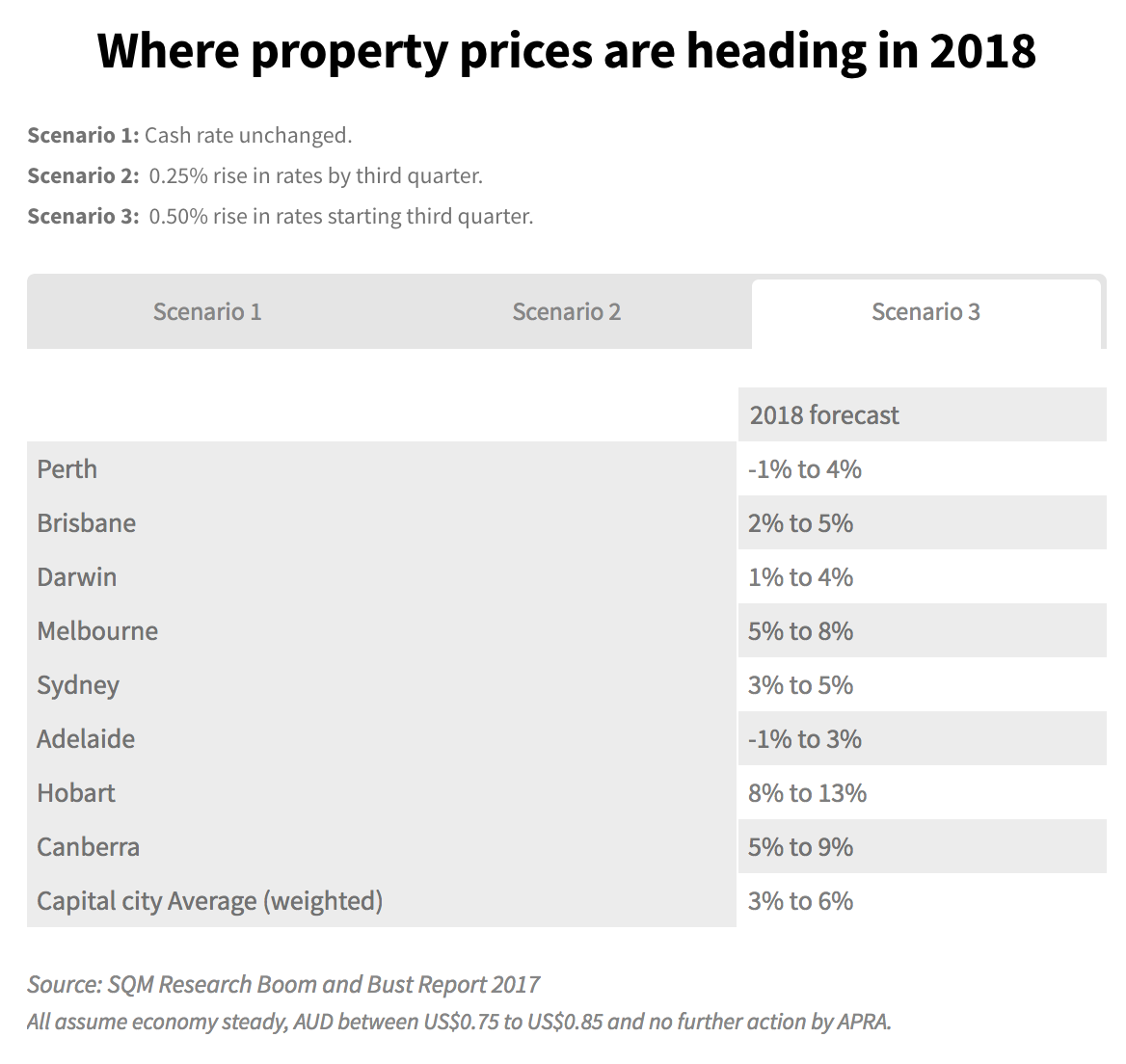

Despite some of Australia’s heavyweight property markets – including Sydney – recording price declines, one expert is forecasting significant house price growth in 2018 across Australia.

Melbourne’s property market is expected to climb between 7 to 12 per cent in 2018, while Sydney is anticipated to soar between 4 and 8 per cent next year, SQM Research managing director Louis Christopher’s Housing Boom and Bust Report 2017 shows.

And in Canberra, prices are anticipated to increase by 5 to 9 per cent, the report claims.

These are ”base case” scenarios that reflect the forecast outcome if interest rates remain stable, if the banking regulator – the Australian Prudential Regulation Authority – doesn’t act to dampen lending activity and the Australian dollar remains stable.

While a strong growth outlook for Sydney would come as a surprise for some after recent data found prices had fallen in the harbour city, Mr Christopher said the market was “a repeat of the second half of 2015”.

In late 2015, prices declined but soon picked up again in 2016, posting another $100,000 in house price growth in the months since.

“It’ll be slow [for the first half of 2018] and will pick up in the second half,” he said.

But even a forecast of 4 to 8 per cent growth is a decline on price movements in Sydney during the price boom.

Despite this, it wasn’t Sydney or Melbourne that Mr Christopher tipped for the strongest growth next year, but Hobart, with up to 13 per cent price growth on the cards.

And Brisbane is also likely to experience strong growth, with forecasts in the 3 to 7 per cent bracket.

Perth and Darwin were also predicted to be entering their “first-year” recoveries, with 1 to 4 per cent growth anticipated in both cities.

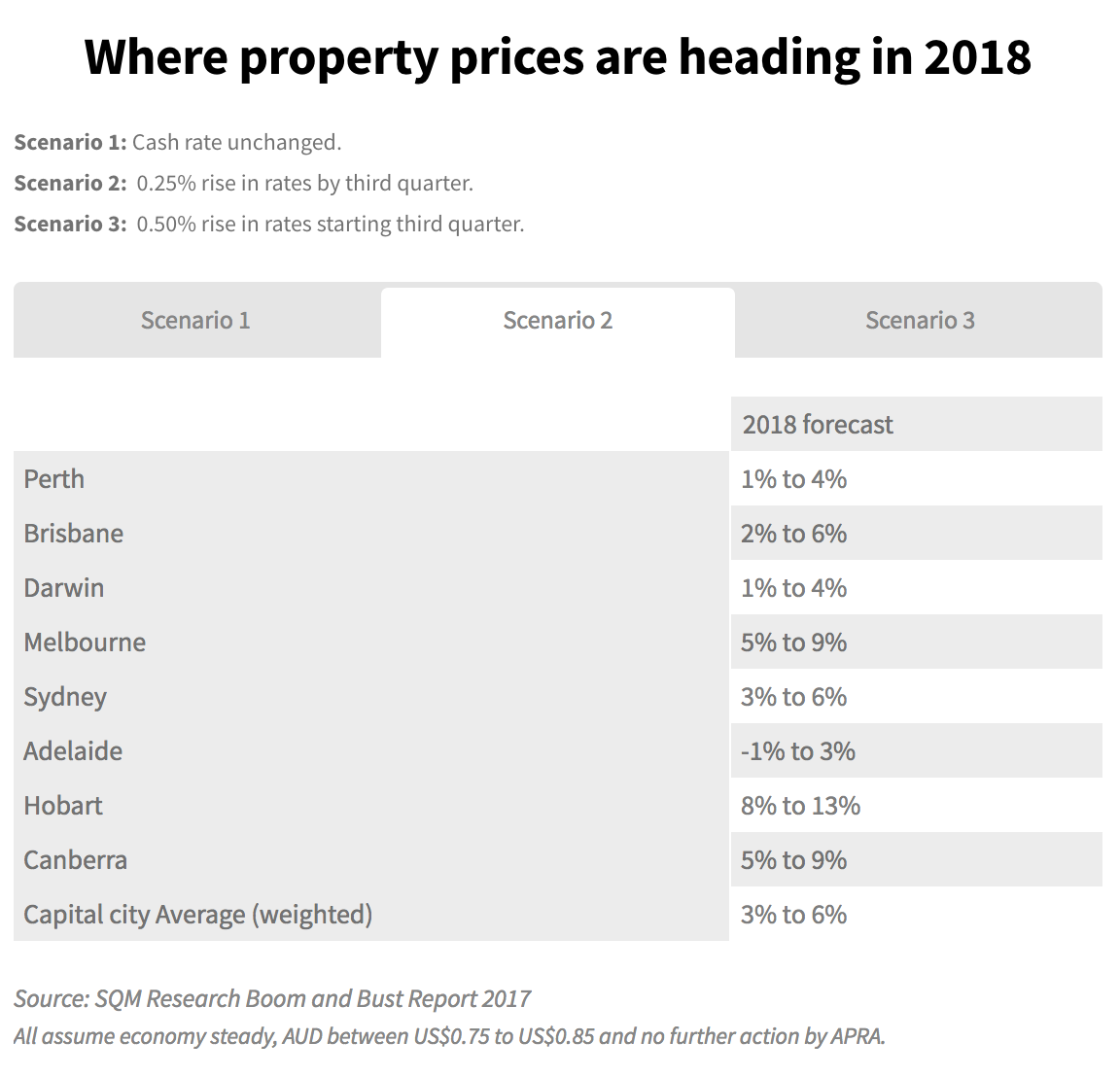

But any increase in rates could dramatically change these outlooks. And any changes from APRA were also an “X factor” that could alter the market, and which have thrown a spanner in the works for earlier forecasts.

”APRA’s action, which came earlier than I had expected, has meant that the Sydney housing market is cooling sooner than expected,” Mr Christopher said, noting this had left their previous forecast of 11 to 16 per cent price growth too bullish compared to a likely 6 to 8 per cent result for 2017.

“The authorities were right to take action earlier this year to restrict investing lending by banks,” he said.

“Failure to have taken action would have resulted in out-of- control Sydney and Melbourne housing markets, where additional aggressive monetary policy may well have triggered a large fall in dwelling prices in 2018.”

The Melbourne and Sydney markets were likely to be most sensitive to any rate hikes – with even a 0.25 per cent increase likely to lead to a lower range of growth in both cities.

In Melbourne, this would be 5 to 9 per cent – or 5 to 8 per cent with a 0.5 per cent rate hike. In Sydney, the growth projects fell to 3 to 6 per cent growth with a 25 basis point hike.

But Domain Group chief economist Andrew Wilson said he couldn’t see Sydney prices increasing by 8 per cent “under any circumstances” – anticipating the growth to be half that at a maximum of 4 per cent for 2018.

“We are set for the lowest growth since 2011,” Dr Wilson said.

“It’s now a very different economic environment [compared to] when the boom began.”

Despite the changing economy, Propertyology buyer’s agent Simon Pressley said he also agreed double-digit growth was on the cards for Hobart, and Perth was reaching the bottom of the cycle.

“The gap between Hobart and the next best capital city will widen significantly during 2018 … we anticipate 2018 Hobart price growth to be in the high teens, with some prospect of pushing through 20 per cent and rental yields to remain above 5 per cent,” he said, tipping 17.5 per cent growth.

In Brisbane, the picture was less bright with “jobs needing to be addressed” before significant price growth was likely to be seen, but he had expectations in excess of 5 per cent.

He expected Sydney would grow by just 1 per cent in 2018.

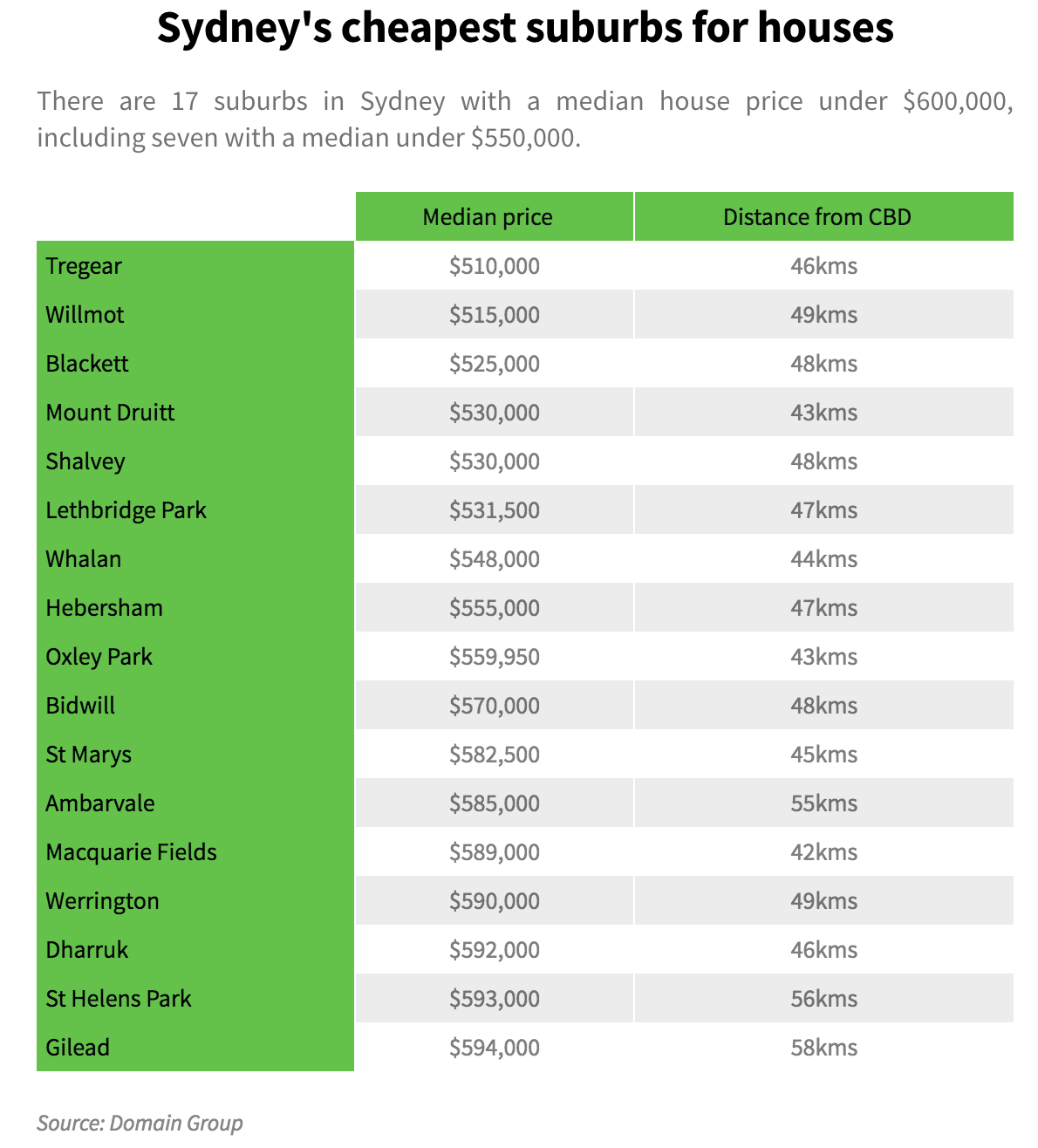

Sydney has surpassed another affordability milestone. There are now no suburbs with a median house price under $500,000.

Five years ago, Sydney was home to 159 suburbs with median house prices of less than half a million dollars.

But these have been dropping off at ever-increasing rates, Domain Group data shows.

Sydney’s western suburbs are among the most affordable – but none of them have a median price under $500,000 anymore.

In March there were four suburbs with a median price below $500,000. And by June, there was one suburb left: Willmot, with a median of $485,000.

But now, not a single suburb remains.

Ellsworth Drive, Tregear Photo - Ben Price Real Estate

The closest to this price point is Tregear where the median house price is $510,000 – followed by Willmot, with a $515,000 median price. Both suburbs are more than 40 kilometres west of the Sydney CBD, September quarter data shows.

In Tregear, a typical three-bedroom house on 580 square metres aimed at first-home buyers and investors, sold for $515,000 in July.

As this is the “median” price – the middle sale of everything sold in a measured time period – this means there would be some homes available under this value.

But it’s a stark reminder of how unaffordable Sydney has become for entry-level buyers, Domain Group chief economist Andrew Wilson said.

“There will always be pressure from the bottom prices upwards, even as the market slows, as many people are still scrambling to buy in.”

Suburbs with a median house price under $600,000 are also in short supply – with 17 suburbs in this category out of hundreds in the Greater Sydney basin.

This includes the cheapest suburb Tregear, but also neighbouring Willmot, Blackett and Mount Druitt – all western suburbs within the Blacktown area.

“Sydney has now waved goodbye to the half-a-million dollar mark, and it’s possible a surge in first-home buyers is behind this,” Dr Wilson said.

First-home buyer data released in August by the Australian Bureau of Statistics saw an uptick in NSW entry-level buyers, likely on the back of stamp duty concessions introduced in July.

This has likely pushed the single remaining suburb under $500,000 up above the mark, as well as increasing the median price in surrounding Blacktown area locations, First Home Buyers of Australia co-founder Taj Singh said.

Investment activity has also continued in these lower-priced areas, despite signs of an easing in activity with lower auction clearance rates.

For young buyers unwilling to consider suburbs more than 40 kilometres from the CBD, the alternative is apartments in the middle-ring for $600,000 to $700,000, Mr Singh said.

“There is a concern that entry-level housing may even exceed the stamp duty exemption level as demand for these areas grows,” he said.

This demand was making it “harder and harder” for those trying to get a foot on the ladder, Compass Economics chief economist Hans Kunnen said.

As a result, first-home buyers were likely to heavily rely on parents and relatives for assistance, and to consider regional or interstate locations.

Others were buying investment properties instead, he said.

But whether droves would move interstate to seek out affordable markets was less clear.

“Sydney is still where many jobs are but Melbourne and Brisbane are making a strong case in terms of job creation,” he said.

This article was originally published by ALLISON WORRALL via domain.com.au on the OCT 12, 2017.

Melbourne house prices are still tracking up, but new data shows growth has started to slow, an early sign the property market is cooling.

And while Sydney’s median house price has fallen for the first time in two years, economists say the Victorian capital is unlikely to follow in the coming year.

According to the Domain Group’s latestState of the Market report, released on Thursday, Melbourne’s median house price has risen to $880,902, a jump of more than $100,000 over the past year.

House prices have now consecutively risen every quarter for five years, but the latest figures show growth is tapering off. Over the September quarter, the median house price rose 1.3 per cent, the lowest result in three years.

HSBC chief economist Paul Bloxham said the cooling of the Melbourne housing market was expected.

“Some cooling of conditions in Melbourne is consistent with tighter lending standards, rising investor mortgage rates and some pullback in foreign demand,” Mr Bloxham said.

Agents say house prices are becoming more consistent. Photo: Jellis Craig

“But we see the demand/supply fundamentals still supporting further house price growth in coming quarters, given very strong recent population growth.”

Mr Bloxham said he expected growth in Melbourne house prices to slow to single digit rates in 2018, reflecting the bank’s view that interest rates will rise next year.

In the apartment market, the median unit price has broken the $500,000 mark for the first time, rising 3.4 per cent over the quarter to $506,334.

The outer suburbs have experienced strong price growth in the past year. Photo: Pat Scala

Overall, apartment prices have risen by 11.4 per cent — or $52,000 — since the September quarter last year.

Domain Group chief economist Andrew Wilson said it was a very strong result, particularly in the outer suburbs.

“Rather than any easing, we’re seeing an acceleration of prices,” Dr Wilson said. “The units in the outer suburbs are just flying at the moment and that’s where the growth clearly is.”

Apartments in the outer south-east region — which includes Carrum, Frankston, Narre Warren, Berwick and Springvale — have experienced the biggest boom in prices, with the median soaring 12 per cent over the quarter and 26 per cent over the year.

It was a different story in inner urban areas where the median fell 2.5 per cent in the September quarter. Inner-city apartment prices remain relatively stagnant, recording 0.3 per cent growth over the past year.

Dr Wilson said Melbourne was overall still recording strong results at auction, averaging clearance rates above 70 per cent.

“It’s still very much a seller’s market,” he said. “But the inner eastern suburbs have been a bit weaker than usual.”

The inner east remains the city’s most expensive pocket, with the median house price sitting at $1.6 million, but it has experienced the lowest annual growth of Melbourne’s eight regions.

Jellis Craig managing director Andrew McCann said A-grade properties in the inner east were still in high demand but, across the board, buyers had become more discerning.

“We’ve been very fortunate that in the past three years we’ve had tremendous gains in the market, so at some point we needed to see a bit more consistency in the pricing side of things,” Mr McCann said.

“For two or three years, we were constantly selling homes for more than we thought they were worth.

“At the moment we are achieving results at expected levels, so if we think a home is worth $2 million, then it’s selling for somewhere between $1.95 and $2.1 million.”

The inner south has also recorded weakening growth while the median house price in the inner-city region dropped 2.5 per cent over the quarter.

WPB Group chief executive Greville Pabst said there were some early signs of falling levels of confidence in the housing market.

“We’ve come off this huge wave of strong prices,” Mr Pabst said. “We’re going to enter into a new paradigm whereby we’re going to see more properties pass in [at auction].”

This article was originally published by Matt Wade via smh.com.au on Oct 9th 2017.

They have dominated suburban Sydney for generations but the freestanding home with a driveway and a yard is in decline.

The total number of traditional detached homes across greater Sydney has fallen by almost 15,000 over the past decade, analysis of the census shows, even though the city's population grew by more than three-quarters of a million people in that time.

While many new free-standing homes are still being added, especially on the outskirts of the city, an even bigger number have been demolished to make way for semis, townhouses and apartment blocks.

The three-bedroom stand-alone home owned by Fotis Maggos on a busy stretch of the Princes Highway at Kogarah Bay will soon be part of the trend.

Fotis Maggos sold his Princes Highway home to a developer. Photo: Fiona Morris

It will make way for apartments after Mr Maggos and his neighbour agreed to sell their properties to a developer when local zoning laws were changed to allow higher density residential buildings.

"This is a prime location for redevelopment," said the 48-year old father of three who owns a small food distribution business.

"It was always going to happen – there's not many houses left along highways now."

Mr Maggos, who has lived in the home for 20 years, said his decision to co-operate with a neighbour and sell to a developer delivered a healthy premium.

In Sydney many older homes are making way for apartments. Photo: Michele Mossop

"I got $1 million more than the value of my property," he said.

Terry Rawnsley, regional economist with consultancy SGS Economics & Planning, said the decline in freestanding housing in Sydney has been driven by the city's growing size and integration with the global economy.

The city's population recently passed 5 million and the increasing demand for well-located land has transformed the economics of housing.

"If you look at other cities of around 5 million or more around the world, many of them don't have anywhere near the amount of detached housing that Sydney does," Mr Rawnsley said.

"Sydney is going through a catch-up phase to get more of that medium and high-density accommodation."

According to the census the number of apartments in Sydney rose by 65,000 between 2006 and 2016 while semis and townhouses were up by 47,000.

About 70 per cent of all dwellings constructed in Sydney last financial year were medium and high density.

The decline of detached houses in Sydney contrasts with other capitals. The number of separate homes in Melbourne climbed by almost 100,000 between 2011 and 2016 while in Brisbane the increase was 80,000.

Greater Sydney's stock of detached housing peaked at 940,000 in 2006 but shrank to just over 924,000 by 2016.

Melbourne now has 1.07 million stand-alone homes, about 143,000 more than Sydney despite its smaller population.

The share of detached homes in greater Sydney in 2016 – 56.9 per cent of all dwellings in the city – is now 16 percentage points below the national average (72.9 per cent).

Mr Rawnsley said that for many Sydneysiders the housing dream was not for a bungalow with a yard but for "an apartment close to public transport where lots of things are going on".

This article was originally published by EWEN MCRAE via starweekly.com.au on OCTOBER 9, 2017

Median house prices in Sunshine and Albion have gone up an average of 11 per cent a year for the past decade, according to new figures.

Figures from property data analysts CoreLogic show Sunshine and Albion as being the equal second most consistently strong housing market, behind East Melbourne which has grown at 12.5 per cent per year since 2008.

Average growth across Melbourne was 6.6 per cent a year for the past decade, while Brimbank as a whole grew by 8.8 per cent in the same time.

Albion now has a median house price of $651, 250, while Sunshine has grown to a median of $728,000.

Douglas Kay Real Estate Sunshine partner, Adrian Kay, said it was no secret the west was becoming more popular for home buyers looking for a bargain, and Sunshine and Albion were particularly attractive.

“I think with the proximity to the city and the value for money you get for the size of properties makes the area very attractive for buyers,” Mr Kay said.

“Sunshine is one of the central transport hubs of the west, and there’s been significant government investment in infrastructure in the area, so whenever you have growing infrastructure the property market always grow around that.

“We’re also seeing a big growth in investors from Sydney, who look at our proximity to the city and compare it to their market and can see value.”

Unit and land medians have also grown steadily over the past 10 years, though not as quickly as house prices.

While house prices have risen steeply in recent years, Mr Kay said it was likely the market would stay strong for some time.

“It’s always difficult to project too far ahead, but I think the growth is sustainable for a while yet,” he said.

“It feels like we’ve got the right recipe to keep growing, with proximity to the city and facilities in the area. Even though prices are going up there is still value for money.

“Our spring season is absolutely on fire at the moment, lots of buyers on the market and a strong clearance rate so there’s plenty to be excited about.”

This article was originally published by Lucy Dean for nestegg.com.au on Oct 5 2017.

Despite public perception that the “nefarious actions” of Chinese buyers are pushing up housing prices, there’s “no evidence” of this, an analyst has argued.

A new report from China research group, Cross Border Management, argues that Australian housing prices are “much more correlated with interest rates and population growth” than Chinese investment.

“The idea of malevolent effects from Chinese investment has gained a significant following in relation to the property market, where it’s become commonplace to attribute the rapid growth in Australian housing prices to the insatiable appetite of Chinese buyers,” said the director of Cross Border Management, CT Johnson.

Pointing to the rising popularity of political groups like One Nation and figures like Clive Palmer, he said: “Groups like Pauline Hanson’s One Nation and the Party For Freedom have made opposition to Chinese investment in Australian real estate one of their signature political issues, and with some success.”

However, he argued that the notion that Chinese investor interest is the driving force behind surging prices is “conspicuously short on supporting evidence”.

Speaking to Nest Egg, Mr Johnson said: “Chinese buyers are a distraction from the actual problem of housing affordability, which is being driven by low interest rates and high population growth.

“Because of their money and race, the Chinese are conspicuous, which makes it tempting to blame them for housing price increases. But that’s just not true.”

Chinese investment in Australia is “relatively small” compared to investors from the US and the UK

While growth in Chinese investment has been “swift and dramatic”, growing from $6.2 billion in 2007 to $87.2 billion in 2016, Chinese investment still counts for just 2.7 per cent of inbound investment flows, according to figures from the Australian Bureau of Statistics.

“In comparison, the US (Australia’s top investor) has invested five times more than China over the past 10 years, doubling its total investment from $433 billion in 2007 to $861 billion in 2016,” Mr Johnson said.

Within real estate alone, for an average $12,800 price increase in Sydney and Melbourne housing each quarter, just $80-$122 was attributable to foreign buyers. That’s according to a 2016 working paper from the Australian Treasury.

Mr Johnson said: "As an American, it’s funny to me that the impact of US investment has been ignored. Over the past decade, the US has invested five times more in Australia than the Chinese have. But I don’t see comments in the paper about the Yanks taking over.”

Population changes in Australia have simply made Chinese residents more visible

Chinese immigrants make up 55 per cent of total immigration from East Asia, ABS figures report. Further, Australians with East-Asian ancestry made up one in 12 Australians in 2016, compared to one in 18 in 2006.

However, Mr Johnson argued: “Many residents from countries like Japan, Korea, Vietnam and Malaysia are mistakenly identified as Chinese. Counting all the groups together nearly doubles the number of “Chinese” in Australia.”

The fact that Chinese residents are “highly visible and highly concentrated”, and sometimes congregate in neighbourhoods like Sydney’s Burwood where the ratio is one in three, or Clayton in Melbourne, where the ratio is one in four, can exacerbate the perception of a Chinese influx.

Pointing out the growing rate of Australian citizens with Chinese ancestry, Mr Johnson said: “It’s not Chinese investment that has generated the public perception of Australia being taken over, but the increase in Australian residents from China and other parts of Asia.”

The proportion of Mandarin-speaking residents is “in no way correlated” with housing price growth

By comparing the 2016 census data about the 79 neighbourhoods with the highest proportion of Mandarin speaking households and the average house price growth rate in that neighbourhood, Mr Johnson and Cross Border Management concluded that “there’s no evidence” that Chinese buyers are pushing prices up in a “significant” way.

“Rather than a correlation between the number of Mandarin speakers and the average annual price growth in an area, we found an uncoordinated mix of average price growth rates,” he said.

“We found that, on average, Chinese buyers like to buy in nicer, more expensive areas, but we found no evidence that they actually drive the price up. In fact, in the case of Melbourne units, it looks like they may have driven prices down, because they spurred so much new development.”

This unaffordability is due to interest rates and population growth

Housing is becoming “progressively less affordable for everyday Aussies”, Mr Johnson said, and this “staggering” increase is a reality that “confronts all Australians” and particularly those with smaller incomes.

However, according to Mr Johnson, this problem is tied to the “conventional” factors of low interest rates, a growing population, limited supply and a lack of available land. Australia’s population has grown by 18 per cent since 2006, ABS figures show.

“Australian interest rates are not merely low, they are at an all-time low, down to 1.5 per cent in 2017, from a high of 17.5 per cent in January of 1990,” Mr Johnson added, noting that housing price increases have historically accompanied periods of low interest rates.

Further: “It’s simply a geographical fact that most of Australia’s population is concentrated around the coasts, where cities are hemmed in by geographical features like oceans and mountains. This makes it challenging to develop new land in response to population growth.”

"Australian house prices are being driven by conventional factors like population and mortgage interest rates, rather than the nefarious actions of Chinese buyers," he concluded.

This article was originally published by Emily Cadman via Bloomberg.com | 5 October 2017

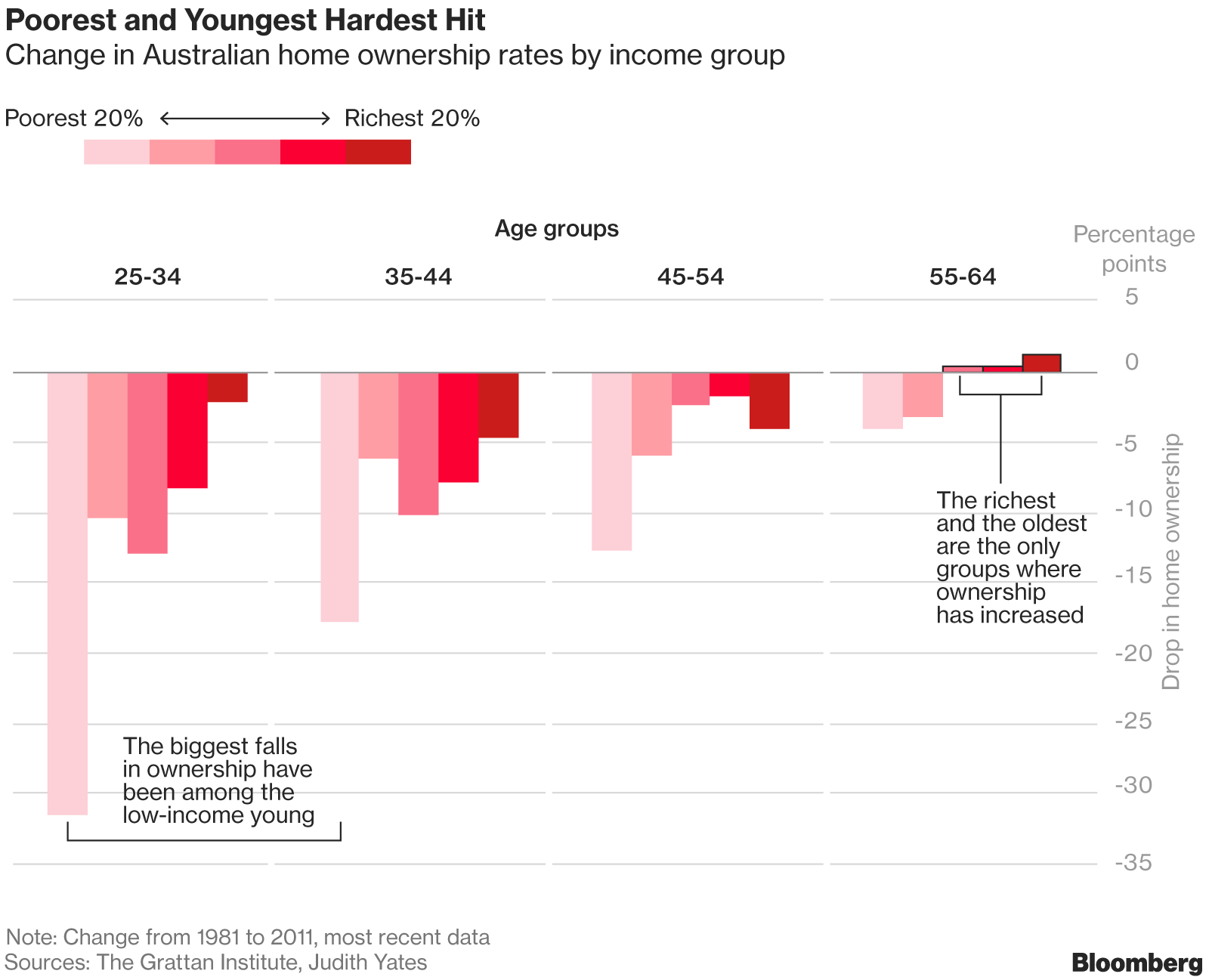

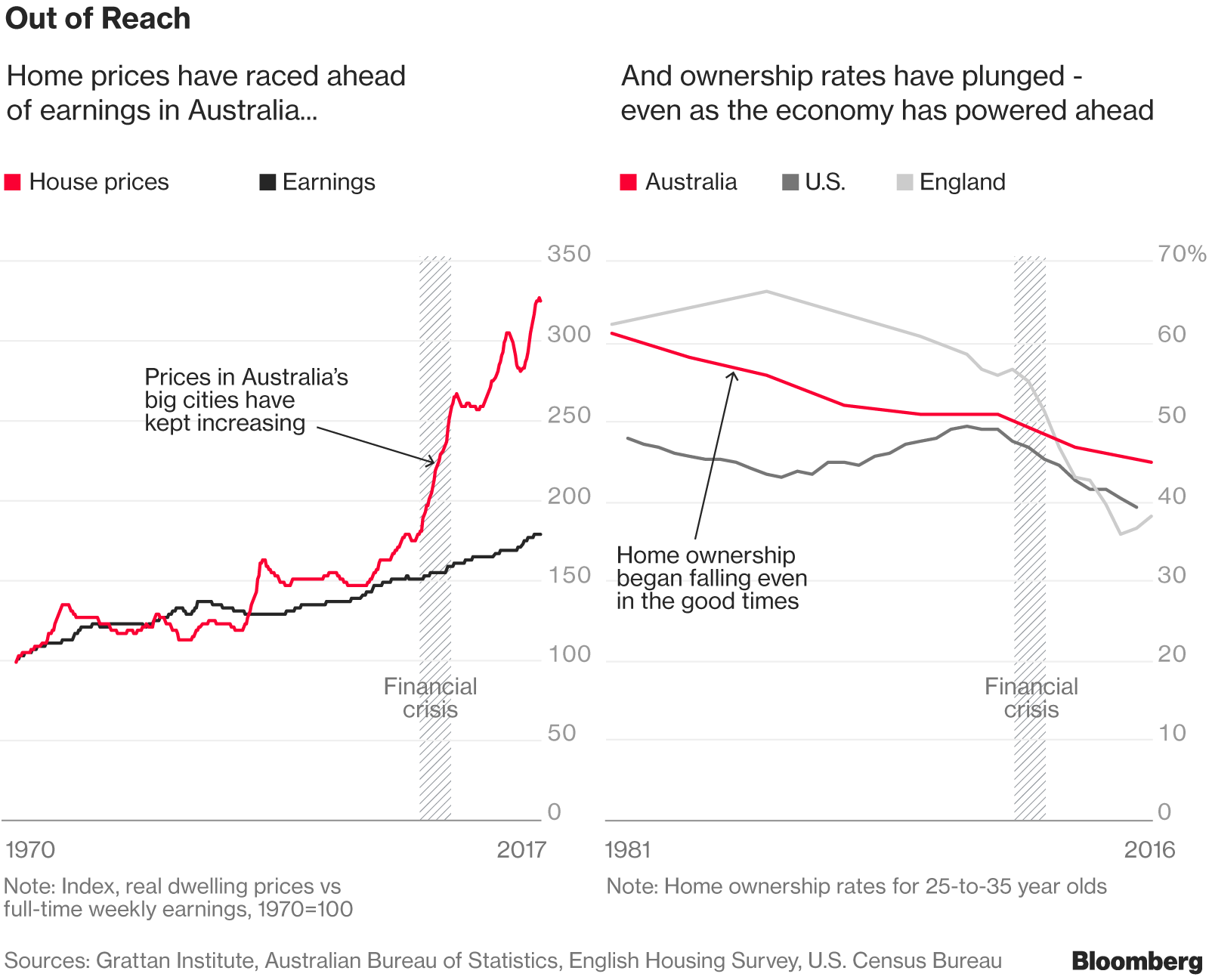

Home ownership among young Australians has fallen to the lowest level on record, as an explosive property boom squeezes out all but the wealthiest.

Supercharged by record low interest rates, a lack of supply and a tax system that favors property investors, home prices have surged more than 140 percent in the past 15 years, propelling Sydney past London and New York to rank as the world’s second-most expensive housing market. Melbourne, ranked the world’s most livable city the past seven years by the Economist Intelligence Unit, is now the planet’s sixth-most expensive place to buy a house.

In response, home ownership among the young has plunged: only 45 percent of 25-to-34 year-olds own their own home, down 16 percentage points from the 1980s, with almost half the decline coming in the past decade. At the same time, hefty mortgages have pushed household debt to a record, acting as a drag on the economy’s 26 years of unbroken growth. As more people retire still owing a mortgage, or renting, they are more likely to qualify for government welfare, undermining the A$2.3 trillion ($1.8 trillion) pension savings system.

“The great Australian dream of home ownership is becoming a nightmare,’’ said Brendan Coates, a housing policy expert at the Grattan Institute. “It’s down to a collective failure of government policy that will take at least two decades to fix.”

Voter angst over housing affordability is mounting: almost 90 percent of Australians fear future generations won’t be able to buy a home, according to an Australian National University survey. Failure to address the issue is heaping pressure on a government already under fire for the botched rollout of a A$49 billion national high-speed internet network, and energy-policy bungling that’s sent power bills soaring and triggered fears of blackouts this summer.

One of the biggest flashpoints are tax incentives that have turned housing into a speculative financial asset. First-home buyers complain they can’t compete against investors, who through a perk known as negative gearing can claim the costs of owning a property-for-rent -- including mortgage interest -- as a tax deduction against other income. The allure of property investment was turbocharged in 1999, when capital gains tax was halved. With housing prices seen as a one-way bet, investors piled in.

More than 2 million, or one-in-12, Australians own an investment property, with almost 30 percent of those owning two or more.

“More money going on servicing a mortgage means there is less to spend elsewhere, dragging on economic growth,” said Paul Dales, chief Australian economist at Capital Economics. “It won’t take many rate rises for indicators to start flashing amber and red for more-indebted households.”

As the average price of a Sydney home sailed past A$1 million, housing affordability fell victim to the hyper-partisanship that has gripped Canberra over the past decade and paralyzed policy making. During last year’s election campaign, when the opposition Labor party proposed changes to limit negative gearing to newly-built houses and reduce the capital gains tax discount, Prime Minister Malcolm Turnbull retaliated by ruling out any changes and launched an assault claiming Labor’s move would “take a sledgehammer” to the property market and “punish” mum and dad investors.

A package of measures in the May budget aimed at improving housing affordability only tinkered at the edges -- targeting overseas investors who leave properties vacant and offering tax breaks for people saving for a deposit on their first home. State governments have also done little to address the issue, relying on policies such as stamp duty discounts or grants to first-home buyers that just act to push prices up even further.

“There’s no way we can fully put the genie back in the bottle,” Coates said. “Pretty much anyone under the age of 35 you’re going to find it pretty hard” to buy a home unless they are a high-income earner, he said.

Politicians, meantime, have offered only superficial solutions. Former Treasurer Joe Hockey said buyers struggling to get into the market should simply “get a good job that pays good money.” Deputy Prime Minister Barnaby Joyce said people priced out of Sydney should have the “gumption’’ to move to rural areas like Charleville in outback Queensland -- where houses are about one-sixth the price of Sydney, but youth unemployment in the region is the highest in the nation.

“What politicians have offered so far are band-aid solutions that might be popular in the short-term but will be ineffective in the long-run” said Judith Yates, who has advised the government on housing policy and is an honorary associate professor at the University of Sydney. “There hasn’t been a serious attempt to tackle the fundamental causes of declining affordability.”

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.