Charles Dickens famous novel ‘A Tale of Two Cities’ best captures the economic and financial market turmoil that everyone has been experiencing in 2011;

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness” – Charles Dickens.

Lately, I have seen many examples of the media thriving on the ‘doom and gloom’ of the current environment, and for most people it’s been one big rollercoaster ride, with the bailout of the US debt market, the decline and possible talk of the breakup of the of the European markets and single Euro currency, and the near collapse, then subsequent recovery of the Australian stock market.

This fear-mongering bandwagon, which the media loves to jump on, has created a very negative overall consumer sentiment in Australia. In fact, Australians have reverted to increasing their spending equivalent to that of the 1985 era, delaying the purchasing of big-ticket items, and, many first home buyers are delaying their entry into the property market. This, in turn, has resulted in low clearance rates of 50% across the major capital cities in 2011, low volume of new listings and a slight decline in the median price across the major capital cities, seen in the table below.

Simultaneously, all of this has created ideal buying opportunities for ‘cashed-up’, and market ready property investors who are capitalising on the dire market conditions, by negotiating massive discounts on blue-chip properties, in premium locations across the major capital cities. Not only are there bargains to be had after a property is passed in at an auction, I have personally witnessed developers slashing tens of thousands of dollars of existing and off-the-plan stock, in an attempt to sell out projects before the end of this uncertain and volatile year. It is truly a time of wisdom, and the age of foolishness.

With a high probability of substantial interest cuts in early 2012, coupled with escalating rental yields across the major capital cities, 2012 is looking like the beginning of the next strong upward trend in the property cycle, especially in Melbourne and Sydney. Many people will look back at 2011 and correctly identify it as the ‘best time to buy property’ under market value, and by that stage of course, it will be too late, as all the bargains will be gone, and market would have moved into the next phase of the property cycle.

One of the most fundamental principles of investing in property in Australia is to appreciate that the market moves in distinct cycles which are characterised by periods of strong capital growth and demand for properties, through to periods of a flat-lining market, following periods of distinctive falling median prices, lower demand for properties, and a decline in property prices. The money is made by both the timing of the market, and of time in the market. Hence my advice right now to investors is not to wait to buy property, rather, buy property and wait.

The general rule of thumb is that these property cycles last 7 to 10 years, and can be segmented into 4 main parts, the ‘Peak of the Market’ being the shortest of the four;

Peak of the Property Market – High capital growth, auction clearance rates of 85 per cent plus.

Decline of the Property Market – Declining capital growth, auction clearance rates dropping from 80 per cent to 60 and 50 per cent.

Bottom of the Property Market – Extended periods of low capital growth, auction clearance rates of 45 percent to 50 per cent.

Growth of the Property Market – Increasing capital growth, increase demand for property, increasing auction clearance rates, 55 per cent to 75 per cent.

It is interesting to note that not only do these cycles vary drastically across the major capital cities in Australia, but the variance can be further observed on a smaller scale within the major cities themselves, for example in Melbourne the Western suburbs and Bayside are counter-cyclical to each other, while in Sydney, the North Shore and the Western suburbs at times have shown similar behaviour. Furthermore, these property cycles can be further characterised by a shifting balance between capital growth and rental yields, this relationship being largely an ‘inverse one’. That is, during times of strong capital growth, rental yields tend to drop as a percentage; the reverse is true during times of stagnant capital growth, or declining capital growth, when rental yields eventually catch up to the market, and increase as a percentage.

So what is the implication of all of this for the average investor?

In essence, successful property investors practice counter-cyclical investing, or they do the exact opposite of what the market is doing. When the consumer sentiment is low, characterised by low clearance rates of 50 per cent or lower, they buy. When the market is booming, which is usually the shortest part of the property cycle, sophisticated investors focus their energy of ‘revaluating’ their properties, and lock in their lines of credit (LOC) at the highest possible level, waiting once again for an opportunity to snap up a bargain at the low point in the market.

Perhaps the best example of ‘counter-cyclical-investing’ is that of the infamous Warren Buffett, who by age 79 built Berkshire Hathaway into a $198 billion company, averaging an annual growth in book value of 20.3% to its shareholders for the last 44 years, while employing large amounts of capital, and minimal debt. Warrens’ famous style of investing was encapsulated in a quote;

“I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.” – Warren Buffett.

Remember that the ‘risk’ always lies with ‘you’, not with the market. The market is simply a vehicle that transfers wealth from the uneducated to the educated. The sooner you gain the necessary skills and education to take advantage of the property market, the sooner you will be making money and taking advantage of rare opportunities such as what the current property and share markets are presenting right now.

After spending years in the industry as financier working for one of the major four, then setting up a mortgage broking company consisting of 15 mortgage brokers, and finally achieving substantial personal wealth via property investing, here is what I deem to be the essential wealth formula when it comes to building large property portfolios and attaining ‘financial independence’:

[Investor Psychology (80%) X Specialised Knowledge (20%)] Mastermind Group

Permit me to break down this wealth formula into its essential components which will be tackled individually, then reassembled into one formula…with some practical applications.

INVESTOR PSYCHOLOGY Multiplied by SPECIALISED KNOWLEDGE.

The first part of this formula is based on the Pareto Principle.

When it comes to property investing, 80 per cent of the formula can be attributed to having cultivated the correct mindset, or ‘Investor Psychology’ and the other 20 per cent can be attributed to what I refer to as ‘Specialised Knowledge’.

The Pareto Principle, also referred to as ‘The 80-20 Rule’, ‘The Law of the Vital Few’, and ‘The Principle of Factor Sparsity’, states that roughly 80% of the effects come from only 20% of the causes. Business management thinker, Joseph M. Juran, suggested the principle and named it after Italian economist Vilfredo Pareto, who observed in 1906 that 80% of the land in Italy was owned by 20% of the population.

The original observation was in connection with income and wealth, and since, various surveys carried out in a variety of other countries have found that a similar distribution of wealth applied, not only in terms of wealth distribution, but the relationship applied also to subsets of the income ranges amongst the rich. For example, if you take the ten wealthiest individuals in the world, we see that the top three (Warren Buffett, Carlos Slim Helú, and Bill Gates) own as much as the next seven put together.

Let’s examine the first component of the formula, ‘Investor Psychology’, which is perhaps the most important component of the ‘wealth formula’.

‘Investor Psychology’ will mean different things to different people, especially when it comes to the world of property investing, given that there are so many approaches and strategies that exist in this realm of investing. For example, there are buy and hold investors buying ‘growth’ properties, investors interested in cash flow positive properties, investors who renovate properties and manufacture capital growth, investors who secure properties via option contracts and on-sell them, and investors who buy property for the purpose of re-development, subdivisions, re-zoning…the list is endless.

Ultimately, there are some commonalities linking all these investors, and their approach to property investing, and it has more to do with what ‘belief systems’ they adhere to and how they do things. As Wallace D Wattles put it in his famous book ‘The Science of Getting Rich’, the rich get rich by “doing things in a certain way” not by doing ‘certain things’. In other words, it’s not what you do, it’s the way that you do it, and that’s what gets results.

So, if that is as ‘clear as mud’ to you, let me get into specifics here, especially when it comes to property investing, and building large property portfolios. Investors with the right psychology tend to use an ‘Optimised Loan Structure’, which is one that allows the property investor to have maximum flexibility and control over every single property that they control or own, either via direct ownership or via a trust/company structure. So each property is set up as a ‘Stand Alone’ facility, that is, only one loan is taken against one property, and hence none of the properties are cross collateralised, all consisting of a variable ‘true’ Line of Credit, with no mandatory repayments, and a self-capitalising component built in with the loan, preferably with separate lenders. To add to this structure, the Line of Credit facility (LOC) will have an offset facility attached to it, allowing the investor, and their partner to directly credit their salaries and rental incomes into their LOC, which in turn offsets the amount of interest that they pay on their Primary Place of Residence (PPR) if they have one.

Furthermore, investors with the right ‘Investor Psychology’ tend to use other people’s money, or ‘OPM’, that is, they use the maximum Loan to Value Ratio, say 95% and are comfortable paying Lenders Mortgage Insurance (LMI) as they know that the most important aspect of investing is in assessing the Return on Equity (ROE) not Return on Asset (ROA). They also do not own any assets in their own name, that is, they use Trusts and Corporate Trustees to ‘Control Assets’ rather than to ‘Own Assets’. And the rich NEVER risk their homes. They pay for advice, surrounding themselves with successful advisors, and are themselves ‘Financially Literate’. They focus all their efforts on accumulating ‘Growth Assets’, using ‘Good Debts’, or tax deductable debts, while avoiding taking on ‘Bad Debts’ or consumer credit, which has no tax advantages to secure assets that devalue over time.

Finally, Investors with the right ‘Investor Psychology’ invest in their personal development and network with like-minded individuals, who support their investing endeavours. They understand that the only risk in investing is ‘them’, not the market, and that the market, whether it’s the property market or stock market, is simply a vehicle that transfers wealth from the uneducated to the educated. They also understand that time is the most precious commodity, and they know that investing in property is simply ‘buying time’ in a market that has a proven history of growth with certain properties.

The ‘Specialised Knowledge’ section of the ‘wealth equation’ refers to the actual strategies which will allow you to secure properties, or build wealth through property. More specifically, it refers to the investor’s depth of knowledge of their chosen area of property investing. Whether it’s property options, property development, subdivisions, buy and hold, flipping or renovations, the ultimate success will lie in the investors ‘grasp’ of the technical aspects of their strategy, in a given area of property, together with their detail and due-diligence or feasibility studies leading up to the deal.

The important aspect to appreciate here is that there is an immeasurable difference between ‘knowing the talk’, and ‘walking the talk’. There are literally thousands of ‘academics’ and ‘theorists’ out there who possess the basic knowledge of ‘the how’ to structure and execute ‘the deal’, but very few who actually implement the strategies. The difference lies in their lack of ‘Investors Psychology’ – that crucial element of the ‘equation’ that actually makes the investor take action. Without ‘the why’, ‘the how’ is irrelevant, as there is no execution, hence the investor doesn’t make any money.

In essence, ‘knowledge’ is not power, as ‘knowledge’ without ‘action’ does not equate to tangible results and money. The final component of the ‘wealth equation’ is the reliance by the investor on his or her Mastermind Group.

To the Power of THE MASTERMIND TEAM

Behind every self made millionaire there is a team of ‘Experts’ that have been that person’s catalysts of success. Put simply, all the ‘Psychology’, and ‘Specialised Knowledge’ in the world will not translate to ‘actual results’. One needs a solicitor to settle the property, one needs a real estate agent to sell the property, one needs a mortgage broker to submit the loan to the bank…you get the idea.

The ‘Mastermind Group’ concept was formally introduced in Napoleon Hill’s timeless classic, “Think And Grow Rich” where he described the principle as:

“The coordination of knowledge and effort of two or more people, who work toward a definite purpose, in the spirit of harmony.”

He continued on to say:

“No two minds ever come together without thereby creating a third, invisible intangible force, which may be likened to a third mind.”

From my observations and interactions with successful property investors and developers over the last decade I have come to the conclusion that most successful property investors are themselves not ‘experts’ in every single field of property investing, rather they become ‘generalists’, relying on their ‘Mastermind Team of Experts’ that they in turn leverage from for their expertise and knowledge. These include, but are not limited to the following:

Your Property Solicitor,

Your Mortgage Broker or Banker,

Your Property Accountant,

Your Quantity Surveyor,

Your Property Valuer,

Your Property Manager,

Your insurance Broker or Financial Planner,

Your Property Mentor.

The key to your success, is to develop your level of ‘Specialised Knowledge’ to such an extent, that you can:

Prequalify and shortlist your key ‘Mastermind Team’ of industry experts;

Coordinate them in a manner that will enable them to implement the necessary steps and actions that will eventually lead to your desired outcome.

The difficulty with accurately identifying and pre-qualifying the relevant ‘Experts’ which will ultimately form part of your Mastermind Team lies with the ‘Investors’ level of ‘Specialised Knowledge’ in that particular field, and their ability to ask the right questions in order to pre-qualify and short list them.

Specifically, your accountant should be very familiar with setting up various types of trusts, (Hybrid, Unit, Family, etc) and have fist hand experience with property settlements utilising those structures, not to mention lending. Your Mortgage Broker of banker should also be conformable with setting up loans via Trusts and Company Trustees, and understand the various credit policy restrictions that apply to buying properties via these. Your solicitor should specialise in Property Law in your particular state, and be well versed in the latest legislation, sale of land act, etc.

Ideally, your Solicitor, Mortgage Broker, and specifically Accountant should all specialise in ‘Property Law’ and they should be positioned as ‘niche’ operators in that industry, resulting in majority of their client base being ‘property focused’ or working in property related industries. To illustrate this example, my accountant is a Property Accountant, My Solicitor specialised only in Property Law, my Mortgage Broker ONLY looks after investors. How about your ‘Mastermind Team’?

To emphasise the importance of the ‘Mastermind Team’ in the ‘Wealth Equation’, this is literally the catalyst of your success! Hence the equation is incomplete with this essential element of an investor’s journey to financial independence. To further re-emphasise this point, I cannot tell you how many clients I have come across (both during my days working for a bank as a financier, and managing a mortgage broking company) who have been given average advice, by accountants, financial planners, and bank managers, and hence have resulted in achieving average results, or in many examples with financial planners, losing substantial amounts of money both in their superfund, and in personal wealth. The problem was, in virtually all cases, that the client failed to correctly identify and assess their consultant’s credentials and accurately assess their ability to give them the correct advice and guidance. The credentials that I am referring to here have nothing to do with the consultants formal qualifications; they are a given, based on current legislation in financial planning, mortgage broking and banking. The lacking credentials that are essentially missing in all cases was that the financial planner, accountant, and mortgage broker were themselves not wealthy individuals, rather, they were selling their time, advice and services, or receiving a commission for the client taking up a recommended product. Looking back now over the years, the most obvious commonality between all the successful clients that I have worked with was that their ‘consultants’ were themselves investors and wealthy individuals in their own right.

So, let me save you years of trial and error, and in the process millions of dollars of potential losses or unrealised profits, by demonstrating to you the most essential pre-qualifying question that you need to ask your Financial Planner, Accountant, Mortgage Broker…

‘How many investment properties do YOU personally own or control?’ Or

‘How much money have YOU personally made from this recommendation?’

And if the answer is none, then walk away! The company’s brand, the company’s reputation, time in the industry or letters after your ‘consultants’ name are all irrelevant – all that matters is their bank account and real results. As harsh as that sounds, what I am giving you is what the 2 per cent who control the other 98 per cent of the world’s money understand. My accountant has $19,000,000 in residential and commercial property, and my mortgage broker has over 21 investment properties. How many properties does your Account, Financial Planner, or Mortgage Broker have?

In summary, assembling your ‘Mastermind Team’ or group of experts will take a long time, due to the scarcity of ‘consultants’ in the various industries who not only hold the correct formal qualifications, e.g. Advanced Diploma of Financial Services (Financial Planning), or being a Charted Practicing Accountant, but also have a PHD in results. The key in finding them lies in your ability to access other successful investors, industry networks, and getting referrals from industry leaders. If you do assemble a ‘Mastermind Team’ of experts who themselves are success stories, your wealth will skyrocket exponentially! Hence the formula for Wealth is ‘Investor’s Psychology, multiplied by ‘Specialised Knowledge’, to the power of (Your) ‘Mastermind Team’.

To Your Success!

Konrad Bobilak.

The extreme Armageddon-like Australian property outlook portrayed by the likes of Harry Dent, Dr Steven Keen and Jordan Wirsz have been extensively publicised recently by the media, spreading wide concern amongst first home buyers, and the largely uninformed mum and dad home owners. Whilst these views are not only unfounded, flawed and often sensationalised, they also have a tendency of robbing the average Australian of the opportunity to invest into an asset class that has proven its resilience to global economic downturns and recessions for well over 100 years, essentially scaring them from buying an investment property.

On this note, the most extreme point of view was voiced by US real estate analyst, Jordan Wirsz, who believes that Australia is heading towards a “property bloodbath” as the global economic downturn spreads, with a decline in property prices of 60 per cent. Mr Wirsz was quoted saying:

“Right now is not a time to be buying real estate in Australia,” and further to this, he stated;

“The market has slowed substantially but residential prices are likely to fall up to 60 per cent, possibly even more, within five years.”

Similar doom and gloom opinions were voiced by visiting US economist Harry Dent who recently said Australian house prices were 50 per cent overvalued, and were destined to crash, just like they did in the US.

Conversely, these extreme views have been largely slammed by Australian property experts, leading economists, and property research based companies including, but not limited to, Residex, RP Data, AMP, ANZ, HIA, BIS Shrapnel, HSBC leading economist -Paul Bloxham, and the list goes on. To put this statement into context, a 60 per cent decline in property prices across Australia would translate to, Sydney’s house prices dropping from $660,000 to $264,000, Melbourne’s house prices dropping from $550,000 to $220,000, and Brisbane’s house dropping from $580,000 to $232,000. It’s laughable, isn’t it?

Did I mention that this proposed ‘market crash’ is supposed to take place in an Australian economic environment which includes low unemployment rates, historically low interest rates, a strong Australian dollar riding on the back of a resource and commodities boom industry, not to mention a massive surge in incoming migration, most of whom will settle in the major capital cities, with a back drop of a decline in housing construction and shortage of dwellings of approximately 160,000 by 2021?

These ‘doom and gloom’ ravings of Steven Keen, Harry Dent, and Jordan Wirsz remind me of the childhood story of Chicken Little. For those unfamiliar with the story, there are several European versions, of which the best-known involves a chick that believes the sky is falling after an acorn falls on its head. Having reached this astounding conclusion, Chicken Little decides to tell the King. On his journey meets other animals (mostly other fowl) which join in the quest. After this point, there are many endings. In the most familiar, a fox invites them to its lair and there eats them all.

The main theme and phrase of this famous fable – The sky is falling! – has been used to make light of the behaviour of those paranoid individuals who catastrophise, or incite panic and fear in others, sometimes to the point of mass hysteria. The Mirriam-Webster Dictionary records the first application of the name Chicken Little to ‘one who warns of or predicts calamity, especially without justification’ – I cannot recall a better application of this phrase than the recent representation made by the likes of Steven Keen, Harry Dent, and Jordan Wirsz.

Before we examine the basis on which most of these doom and gloom arguments rely, keep in mind that this is certainly not the first time in the last 50 years that predictions of the Australian Property Market crashing have been made by so called experts, and academics. In all instances they were proven wrong, as the Australian Housing Median Prices continue to defiantly appreciate decade by decade. The table below depicts median price increases across the major capital cities in Australia since 1966.

It would seem that it’s been raining acorns for the Chicken Littles of this world over the last 50 years. Here is a short list of major economic events, both local and global that triggered a flurry of media articles and predictions that the Australian Property market would crash;

Early to mid 60’s Australia was experiencing a major credit squeeze and finance dried up. Banks lending policies were tightened, resulting in an environment where it was very difficult to borrow any money to buy property. Due to the inability for most Australians to enter the property market, Academics and ‘Experts’ predicted that the Australian property market would crash. They were wrong.

The late 1960’s Poseidon bubble, saw the price of Australian mining shares soar, especially in the late 1969, then subsequently crash in early 1970. This ‘stock market bubble’ was triggered by the Poseidon NL company’s discovery of a promising site for nickel mining in September 1969. As a result, academics and ‘experts’ predicted that the Australian property market would crash. They were wrong.

In the 70’s, Australia, along with most of the industrialized countries, except Japan, experienced an economic recession due to an oil crisis caused by oil embargoes by the Organization of Arab Petroleum Exporting Countries. The crisis saw the first instance of stagflation. Coined ‘the OPEC Oil Crisis’, this global event created a media frenzy of ‘Doom and Gloom’, and academics and ‘experts’ again predicted that the Australian property market would crash. They were wrong.

The early 1980′s saw ‘a severe global economic recession’, affecting much of the developed world in the late 1970′s and early 1980′s. The United States and Japan exited the recession relatively early, but high unemployment would continue to affect other OECD nations including Australia through to at least 1985. Long term effects of the recession contributed to the ‘Latin American Debt Crisis’, the ‘Savings and Loan Crisis’ in the United States, and a general adoption of neoliberal economic policies throughout the 1980′s and 1990′s. Academics and ‘experts’ again predicted that the Australian property market would crash in the mid 1980’s. They were wrong.

After the Australian Property market refused to crash in the early to mid 1980’s, many Financial and Economic commentators got onto the ‘doom and gloom’ band wagon, fuelled by the media, stating that Australian house prices were way ‘overpriced’ compared to other industrialised countries, and that the ‘property bubble’ would ultimately burst, leaving behind devastation. The prevailing argument here was that the average household debt had reached a ‘peak’ level, and based on academic deduction of the data, conclusions were drawn that people would simply not be in a position to borrow more money, hence property would stagnate and eventually crash. At the time, property median prices in Melbourne and Sydney were about $85,000! They were wrong.

On the 20th of September 1985 the Australian Government introduced Capital Gains Tax. The implications for Property investors was that any capital profits made from a sale of an investment property was now subject to a marginal tax rate of the investor. Financial commentators, financial planners, and so called ‘experts’ predicted that this was going to BE THE END of property investing as we knew it. They were wrong.

In 1987 we had the ‘Stock market crash’ and what many referred to as a ‘1930’s type depression, with consumer sentiment at record low levels, the media once again jumped on the ‘doom and gloom’ bandwagon. With super funds being wiped out virtually overnight, many financial commentators and academics predicted that this prolonged period of economic uncertainty would be followed by a ‘Property market Crash’. They were wrong.

In 1989 to 1991 Australia experienced historically record high interest rates and inflation. The early 1990′s were the beginning of another recession; many of us will remember it for the famous quote from the treasurer, Paul Keating, “this was the recession we had to have”. Of the 18 OECD countries of reasonable size and development, 17 experienced a recession in the early 1990′s — a similar situation to the mid-1970′s and early 1980′s global recessions. The cash rate reached a staggering 18 per cent in the second half of 1989, and mortgage rates of 17 per cent, and many loans to businesses were well in excess of 20 per cent. Unemployment ended up peaking at 11.3 per cent, and once again many academics and experts predicted that the property market would crash. They were wrong.

The ‘Asian Currency Crisis’, which gripped many of the Asian countries in mid 1997, raised fears of a worldwide economic recession. The crisis started in Thailand, and soon spread to neighbouring countries, eventually reaching as far as China and Japan, which directly impacted US and Europe. With major impacts on the various stock markets and managed funds around the world, many academics and experts predicted that the Australian Property Market would crash. They were wrong.

The coordinated terrorist attacks on USA that took place on September 11, 2001, resulting in the collapse of the Twin Towers of the World Trade Centre created a virtual stock market freefall in the US and considerable drops were witnessed around the world. The uncertainty of follow-up terrorist attacks, created a downward spiral of negative consumer sentiment, and once again, academics and experts predicted that the Australian Property Market would crash. They Were wrong.

The Sub-Prime Crisis in the US in 2006 to 2007 was triggered by a rise in sub-prime mortgage delinquencies and foreclosures, and the eventual collapse of subprime mortgage backed securities. Being essentially blamed on poor banking credit standards, greed, and speculation of assets continuously rising in value, the impact of this crisis triggered a plethora of media articles, and commentary of warnings that what happened in the US would eventually happen in Australia. In fact, many so called academics and experts went on record to say that the Australian household debts in relation to house prices were unsustainable, and the bubble would burst somewhere in 2009 to 2010. It didn’t. And as the table below depicts, the market slowdown was minimal, and was absorbed by the ‘buyers’ market almost instantly.

In 2010 to 2011, after defying the predictions of many academics and experts, the Australian Property Market once again continued to climb, with Melbourne hitting a new peak median price of $601K in December of 2010. This defiance to conform to predictions of collapse, lead to, in 2011 and early 2012, another campaign of predictions that the ever mounting household debt locked in the Australian housing market would ultimately lead to a ‘bubble bursting’ – with many families and household owners losing their life savings when the housing market corrects by 30 to 60 per cent of its current levels. Perhaps the most memorable example of a doom and gloom article is that of commercial property advocate, Chris Lang, who proclaimed that Baby Boomers who do not sell their homes in 2012 will have to wait until 2025 before they could sell them, as no one would be interested in a large 4 bedroom houses in Melbourne and Sydney…

“Baby Boomers are facing an enormous challenge. And the sad fact is that they are probably not even aware of the problem. You see, if they haven’t sold their traditional inner-suburban homes before 2012 they need to be prepared to hold onto them until 2025, because there simply won’t be a market for that type of property before then.”

There is, in fact, an exhaustive list of other arguments that all predict that the Australian Property Market has to crash, ranging from demographic reasons, to economic reasons, stock market related reasons, to monetary and fiscal changes in Europe.

One argument used excessively by various commentators is that Australian house prices are overvalued, with the average mortgage representing the equivalent of 9.2 times the average annual income. Hence, the argument is, that this is unsustainable, as eventually people will not be able to service or even qualify for these loans if prices continue to rise. This argument was addressed in a recent report issued by the ANZ bank, senior economist David Cannington and Paul Braddick, head of property research at ANZ, stated that;

“Despite the continued concerns about significant Australian house price overvaluation from some commentators, housing market fundamentals remain supportive,”

The report goes on to state that majority of the capital growth in Australian median prices since 1986 can be attributed to gains in average household incomes and a structural decline in the cost of borrowing. See table below.

Furthermore, the report stated that some 92 per cent of the median price appreciation since 1986, of the residential market, can be explained by these two contributing factors (shown above) which are interest rates, and household income growth.

Here are my personal top 8 reasons why the Australian Property Market will continue to beat the odds and continue to exponentially appreciate over time, especially over the next 15 to 20 years.

1. Increasing Population growth via migration. If we look at the basics, the number one driver of house prices is demand, especially if that demand is every growing, consistent, and focused on specific areas and suburbs. This is definitely the case with the record high level of migration that is coming into the country on an ever increasing basis, year after year.

Based on estimates released by the Treasury, Australia’s population will explode to over 35million by 2056, that’s an increase of 14.5million people, most of whom will come from overseas. It’s important to note that most of these people will be living along the eastern cost of Australia, concentrated around the major capital cities like Melbourne, Sydney, Brisbane, and Perth. This point is further highlighted by the table below, depicting population increases in the specific cities around Australia. For example, the estimated influx of additional 3,355,957 people that will be migrating to Victoria, 2,991,976 of them will be living in Melbourne.

2. Australiana faces a looming housing shortage, and our Housing Industry cannot cater for the ever growing demand of housing. One of the most significant and perhaps challenging issues that will have to be addressed by the Australian governments in the next 5 to 10 years is how to solve the ever increasing housing shortage which according to the Housing Industry Association (HIA) will stand at approximately 160,000 by 2020 in NSW, 112,000 in WA, and there will be a shortage of 105,000 in VIC.

As can be seen by the table below, the shortage of new dwellings coming into the market is dire across the board, with a prediction of over 500,000 dwelling shortages across Australia by 2020.

Whilst these shortages are staggering, there are two more aspects of this issue that need to be appreciated in order to fully take in the gravity of this situation. The first is that the majority of new dwellings are being constructed on the fringes of the major capital cities in Australia in new estates. This is mainly due to established suburbs having height and density restrictions; large scale developers are usually left with fringe city farm land that has been rezoned as the place to establish new housing estates. In Melbourne, there are over 105 new housing estates located in all directions on the outskirts of the city. This means that the housing pressures on established suburbs and inner city areas are likely to keep increasing, along with their prices, due to the majority of jobs and infrastructure being concentrated in the city areas of the major capital cities in Australia.

The second point to appreciate is that currently Australia does not have a workforce that is capable of building 500,000 new homes by 2020. This shortage of skilled labour, combined with the bureaucracy involved in creating new land estates will continue to underpin property prices across the nation for decades to come.

3. Australia has strong economic fundamentals in place that will underwrite the demand for houses for decades to come. With the Australian Government’s constant focus on the trade and strengthening economic ties with the emerging Asian markets since the 1970’s, shifting from reliance on the western European markets has certainly paid off. Since the 1980’s Australia has experienced extensive periods of economic growth averaging 3.3 per cent in real GDP growth rates. This shift has turned Australia into one of the fastest growing advanced economies in the world.

Australia is the 13th largest economy in the world according to nominal GDP (current prices) and the 17th largest according to GDP (PPP). In 2010, Australia’s GDP (PPP) was US$882.344 billion – a 3.94 percent increase from 2009. Australia’s nominal GDP (current prices, US dollars) growth during the same period was even more amazing – GDP (current prices, US dollars) grew from US$994.25 billion in 2009 to US$1.219 trillion, a 22.68 percent increase.

With strong ties with China, who is about to relocate 130 million of its people into city areas, and skilled jobs, the likelihood is that China’s thirst for Australian’s commodities is likely to last for decades.

4. A unique banking system that is underwritten by the residential property market. Our $3.5 trillion dollar private residential housing market is completely dominated by the four major banks in terms of mortgage exposure, which only stands at about 30 per cent. Putting aside unencumbered houses and investment properties, owner occupied properties in Australia have mortgage levels where the average loan to value ratio is located somewhere between 50 to 60 per cent. This is a very important point to appreciate for two reasons. One, properties would need to devalue by 40 to 50 per cent before there would be any effect on mortgage sentiment, and even at that point in time, given the strength of the economy and emotional link to owner occupied living, most people would be hesitant to sell their house, and perhaps more importantly, two, the mortgage debt is not evenly spread against all dwellings across all suburbs. Taking Melbourne as an example, top suburbs like Kew, Camberwell or Balwyn have 65 per cent of all properties unencumbered. Contrasted with new our ring estates like Point Cook, Tarneit, or Pakenham, 95 per cent debt. The reality is that there are a lot of rich people in Melbourne, Sydney and Brisbane, sitting in houses that are completely paid off, and completely unaffected by any property price movements.

The other unique aspect making up the Australian banking landscape is the very stringent lending policies and credit scoring systems that are widely used in Australia, where the majority of loans written are full doc loans, insured by QBE or GE, resulting in an extremely low mortgage default rate of 0.7% per year. This is an extremely low default rate by international standards, and it’s a credit to our banking system, which has provided so much needed stability in recent economic times.

5. Strong social emphasis on house ownership, entrenched by government and developers. We have all heard at one time or another that the‘Great Australian Dream’ is to own a 4 bedroom house on a 1200 square metre block. Whilst for many this is a now all but a dream, with median prices around Australia’s major capital cities hovering around the $550,000 to $600,000 mark, and realistically requiring $900,000 to buy a 4 bedroom house in an established area, many first home buyers or migrants struggle to buy into one of the most expensive markets in the world. Ranking ahead of London, New York, Rome, Los Angeles, Berlin or Hong Kong, the latest survey by the Economist Intelligence Unit, shows that Sydney leads the list of the five Australian mainland capital cities in the Top 20. Sydney globally is ranked at number seven, slightly ahead of Melbourne at number eight. Perth is the 13th most expensive place to live in the world, Brisbane is 14th and Adelaide is 18th.

One of the contributing factors to the resilience of our residential property market is the extensive push by our government since the end of the Second World War into home ownership. This has, in large, been reflected in the various financial incentives, such as the First Home Buyers Grant, offered by both the state and federal governments. The other major contributing factor is the constant drive and advertising by major land developers such as Delfin, Vic Urban, Australand and others, depicting families in new house and land estates. This relentless push of home ownership has resulted in a deep entrenchment of home ownership as part of the Australian culture and rite of passage from one generation to the next. The point being made here is that one cannot underestimate the potency of the belief systems and values of a society, that have been developed and reinforced by family members and peers over decades.

6. Geographically isolated premium suburbs, and estates. One of the most unique features of the Australian Housing landscape is that virtually every suburb in Australian came into existence within the last 200 years, and more importantly, each suburb was at one stage a ‘master planned’ estate that was sold to home buyers based on a stage released process. This means that each and every suburb at one stage or another had a similar price range, and housing design guideline, attracting a similar type of buyer based on demographic, and income band. Needless to say, over time, some suburbs have transformed, with many of the traditional inner city suburbs which were originally made up of blue collar workers, such as Melbourne’s Middle Park or Port Melbourne, have now attracted white collar workers due to their unique proximity to the city, being 3 to 4 km, access to infrastructure, and the beach. However, there are always exceptions to this rule; many of the original affluent suburbs have also remained affluent over the decades, such as Melbourne’s Toorak, South Yarra, Canterbury, Kew, all of which shared a common thread of having land blocks in excess of 1000 sqm and houses of 25 to 50 squares being offered in the original suburb marketing plan. The end result being that Melbourne, Sydney, and Brisbane have ended up with very distinctive and often fragmented property markets, virtually independent of each other, and have no real common links. In Melbourne for example, there is no correlation between Broadmeadows in the western suburbs, where the median price is $350,000 compared to Toorak, where the median price is $2.75million. These distinctive suburbs house have virtually nothing in common, in terms of level of debt, income bands, job industries, etc.

Due to this unique and fairly recent establishment of suburbs by international standards, within the main capital cities around Australia, we have ended up with a situation where the rich are concentrated in very specific areas or suburbs, as are the middle class, as are the less affluent. This has resulted in different suburbs and areas being affected in completely different ways depending on what the economy or interest rates are doing. During times of high interest rates for example, the outer ring suburbs in Melbourne experience much higher ‘mortgage stress’ levels than the ‘old money suburbs’, where over 50 per cent of house are completely paid off.

Further to this, suburbs within the 10km ring around the CBD have also been under mounting pressure due to their close proximity to major job hubs, transport, and lifestyle areas.

7. Taxation system that is biased in favour of property investing. One aspect that has been a catalyst of property investing is the numerous tax advantages that are available to property investor due to a unique tax system. The list of tax deductions that are available under the current tax legislation runs literally into hundreds of potential tax deductions that are available to individuals who choose to invest in property. Perhaps the most notable of these is the ability to claim the interest component of the loan as a tax deduction, not to mention building deduction of 2.5 per cent over 40 years, depreciation of fixtures and fittings over 5 to 15 years (depending on method of depreciation, diminishing value or straight line) and a multitude of other deductions relating to upkeeping; insurance, property management costs, and ongoing costs associated with an investment property. All of these factors combined have the potential to turn a negatively geared property (whereby the rental income from the property does not cover the interest only repayments) to a neutrally geared property or even cash flow positive.

Essentially, the implications of a taxation system that is completely biased in favour of property investing means that accountants, mortgage brokers, and some financial planners will continuously be recommending direct property investing as a holistic solution to wealth creation.

8. Social proof of property investing as a safe, predictable way to make money. Despite the recent international stock market volatility, according to an investment report by Russell Investments, the average house in Melbourne has returned an average of 49.8 per cent over a five year period until June 2011. This equates to an average annual return of 9.98 per cent per year, which is a hefty contrast compared to the stock market, bonds, or commodities. What’s more astounding, is that despite all the doom and gloom predictions, and in light of major international economic turmoil, the Australian Residential Property Market has managed to return an average of 10.1 per cent for the 10 year period until June 2011, and a staggering annual average of 11.6 per cent of a 25 year average until June 2011.

Similar results were documented in a recent ANZ report, which showed that over a 24 year period, taking costs, taxes and gearing into account, property was the winner compared to that of the ASX200, Government bonds, Commercial Property and term deposits. See table below.

Further studies by RMIT substantiated these findings, showing that over a 20 year period of time, residential property outperformed the ASX top 200 companies. The ANZ report called ‘Australian Property Research Asset Returns: Past, Present and Future’, showed that once all the associated holding costs were considered for the various assets included in the study, owner-occupied housing was found to have generated an annual return of 12 per cent. Investment property 9.6 per cent, stocks 8.9 per cent, government bonds 4.8 per cent, commercial property 4.2 per cent and term deposits 3.7 per cent.

Despite these unquestionably outstanding results, every year there is a new breed of ‘doom and gloom’ seers, who eagerly await the mythical property bubble to finally burst, and for the property market to come tumbling down. These prophets of doom seem to reappear every time the property market enters its decline or stabilization part of the property cycle, and they disappear as quickly as they came, when the market shows signs of recovery and progresses, once again, to the upturn and boom part of the property cycle. They then retreat into the dark cubicles, libraries, or university research departments, collecting new documents and data, preparing for a new opportunity to herald their next Apocalyptic prophecies.

At the end of the day, you will have to make up your own mind on the outcome of the Australian Property Market, and whether or not it is ‘safe’ to invest. Invariably, some will go the way of Chicken Little, assuming ‘the sky [or market] is falling’, catastrophising their way to quiet desperation. Others will proceed with caution, evaluating the true situation, recognising the excellent prospects before them. Personally, I advise you to pause and be wary of the hysteria – it has been the source of regret for so many Australians, who, after realising their lost opportunities, have now been forced to swap their old mantra for a disheartening new one; “If only”. So instead, do this; go out, buy a helmet, and the next time ‘The Oracle’ hollers that the sky is falling, look up, look down, and realise, it’s just an acorn.

Before I go into what I believe are the best investment opportunities in 2013, permit me to take a moment to reflect on 2013, an interesting year, during which we were told the world was supposed to end several times, not to mention our economy and property market crash.

Lets rewind the clock back to 2008 and reflect a little on the Global Financial Crisis, (GFC), which came and went, and all the media in Australia, including academic, so called ‘experts’ who made extensive predictions that Australia was heading towards a “property bloodbath” as the global economic downturn spread, with a decline in property prices of 60 per cent (Jordan Wirsz) or worse. This extreme Armageddon-like Australian property outlook portrayed by the likes of Harry Dent, Dr Steven Keen and Jordan Wirsz, were, over time, all proved wrong.

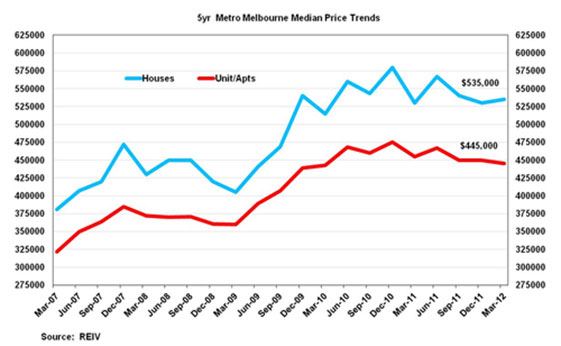

In fact, not much happened around the major capital cities; have a look at the Melbourne property market as an example below;

Conversely, these extreme views have been largely slammed by Australian property experts, leading economists, and property research based companies including, but not limited to, Residex, RP Data, AMP, ANZ, HIA, BIS Shrapnel, HSBC leading economist -Paul Bloxham, and the list goes on. To put this statement into context, a 60 per cent decline in property prices across Australia would translate to, Sydney’s house prices dropping from $660,000 to $264,000, Melbourne’s house prices dropping from $550,000 to $220,000, and Brisbane’s house dropping from $580,000 to $232,000. It’s laughable, isn’t it?

Did I mention that this proposed ‘market crash’ is supposed to take place in an Australian economic environment which includes low unemployment rates, historically low interest rates, a strong Australian dollar riding on the back of a resource and commodities boom industry, not to mention a massive surge in incoming migration, most of whom will settle in the major capital cities, with a back drop of a decline in housing construction and shortage of dwellings of approximately 160,000 by 2021?

So once again, the ‘Doom Seers’ retreated back into the dark cubicles, libraries, or university research departments, collecting new documents and data, preparing for a new opportunity to herald their next Apocalyptic prophecies.

And they didn’t have to wait very long due to the emergence of the European Debt Crisis, and once again the bandwagon of academic experts came around prophesying the demise of the Australian Property Market, high unemployment and years of misery. It was apparently inevitable that the European Debt Crisis would spill over to the Australian economy and the Australian Property market would suffer.

It didn’t, and despite the Australian property market being relatively flat in 2012, due to most capital cities being located in the bottom of the property cycle, no crashes were in sight.

So once again the ‘Doom Seers’ retreated and waited for another opportunity, patiently awaiting their opportunity to prophesize the Apocalypse once again, but this time for real!

Before long, they siezed their next Apocalyptic opportunity, the reduced Growth in the Chinese Economy. By end of 2012, the last quarterly Chinese economic figures showed that China’s growth, which has been recording double digits for years, slowed down to a decade-low 7.5%, as a result of weak export markets and Beijing’s efforts to curb surging prices, which have succeeded in reducing inflation and stabilizing property prices. At the end of the day, it is completely unsustainable to have growth at double digits for decades on end without inflation going out of control. This slowdown in the economic growth of China coincided with a drop in iron ore prices to record low levels in the months of August and September 2012 where iron ore slumped to below $US87 a tonne in world markets.

This was the opportunity that the ‘Doom Seers’ were waiting for, making a quick link between China’s economic slowdown and slump in iron ore prices signifying the ‘End of the Mining Boom in Australia’, followed by high unemployment, and you guessed it….a property market crash!

Unfortunately for them, their prophesies were short lived when in January 2013 the Organization for Economic Cooperation and Development (OECD) stated that the economy would bounce back to grow 8.5% next year and 8.9% in 2014 as domestic demand gathers pace and spending on housing and infrastructure revives, the report predicted. That is more bullish than the International Monetary Fund, which forecasts 2013 China growth of 8.2% and 8.5% in 2014. To add salt to their wounds, iron ore prices jumped back to $US157 a tonne, as China ran out of iron stock pile. And, no property crash in sight.

The point of all this?

The Australian economy it seems, is extremely stubborn in succumbing to the mystical ‘Property Bubble’, with mortgage arrears percentages being negligible, household debt stabilizing, savings increasing, and relatively low unemployment numbers; it suggests the housing market represents a modest threat to the economy.

The head of the country’s central bank certainly wonders what all the fuss is about.

“It has to be said that the housing market bubble, if that’s what it is, seems to be taking quite a long time to pop – if that’s what it is going to do,” observed Reserve Bank of Australia (RBA) Governor Glenn Stevens.

Interestingly enough, in a recent interview by AFR editor-in-chief Michael Stutchbury and economics editor Alan Mitchell with the Reserve Bank Governor Glenn Stevens, showed that Glenn Stevens does not think Australian house prices are unreasonably high and does not believe they will drop. Nor does he agree that we have a price bubble.

I tend to agree with him.

INVESTMENT OPPORTUNITIES AND HIGH GROWTH AREAS FOR 2013

According to ABS studies around 1 million houses in Australia are owned by private landlords, but how many of these can be classified as ‘real’ property investors?

The latest ABS figures show that approximately;

75% of investors own 1 single property

15% of investors own 2 properties

8% of investors own 3 properties

2% of investors own 4 properties or more

Personally, I classify one a true property investor if they have 4 properties or more, especially those who have 5 plus as this would need to involve a considerable amount of knowledge and time investment.

Here is my question to you…

Where do you sit in this ranking?

And more importantly, where do you want to be located on this ranking in the next 5 years?

My final question to you is what specific action steps are you going to take and implement in 2013 in order to make this happen?

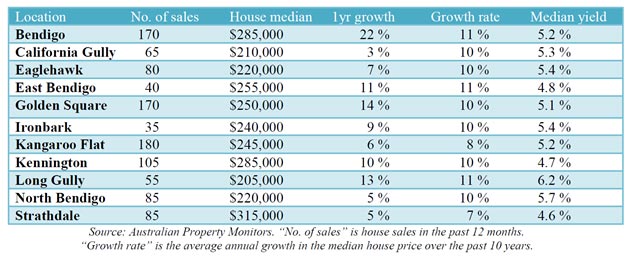

HERE ARE MY TOP 3 INVESTMENT PROPERTY LOCATIONS FOR 2013.

Regional Areas;

BENDIGO – VIC

Bendigo has long been one of Victoria’s key regional centres, with solid growth thanks to its steady local economy, proximity to Melbourne and good transport links to the capital. Bendigo is 130km north-west of Melbourne. It is accessible from Melbourne via the Calder Freeway and the Bendigo railway line, both of which have been recently upgraded. Bendigo is an 80-minute commute to Melbourne’s CBD via the V-Line Regional Fast Train, following a rail upgrade completed in 2006.

Bendigo has shown steady long-term price growth but remains affordable. Its economic prospects have improved recently with State Government plans to spend $630 million on a redevelopment of Bendigo’s hospital and private sector plans to develop the city’s first master-planned residential community.

Bendigo has been experiencing what seems to be an ever-growing population problem, which has created a perfect storm for savvy investors who are taking advantage of capital growth rates of 11 per cent over the last 10 years, vacancy rates of 0.2 to 0.4 per cent, and 5 to 6 per cent rental yields!

Did I mention that the median price is $285,000, and not to mention a population growth of up to 4.5 per cent per year in areas such as Huntley? All in all, it’s an area that has an diversified industry, balanced between manufacturing, Health Care and a number of white collar industries, and is growing organically, well above Melbourne and other regional areas around Australia.

See the capital growth history of the Bendigo area below;

Furthermore,regional areas have outperformed capital cities in the year to March, according to the ANZ, with Bendigo coming in as the fastest regional growth area in Victoria.

Source RP Data, Rismark, ANZ

Given the low entry point, or a median price point of $285,000, Bendigo gets my No 1 top recommendation for 2013.

Major Capital Cities;

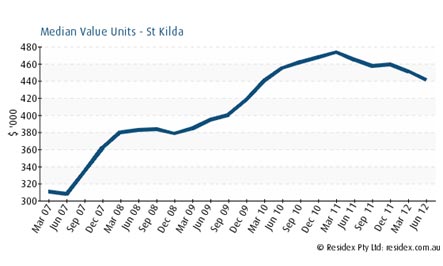

ST.KILDA – VIC

If Melbourne is “The World’s Most Livable City”, then St.Kilda is without doubt a premiere investment ‘hot spot’ on a global scale. St. Kilda is one of Melbourne’s top high-in-demand suburbs, with a young population, predominantly in the 25 to 34 year age group, leading a huge demand for rental property. With a blue chip and highly sought after inner city location, the suburb sits within 6 km of the CBD, in an area that is recognized as Melbourne’s most iconic cosmopolitan attraction, surrounded by parks and gardens, cafés, restaurants and an endless array of retail destinations, including designer Chapel Street, eclectic Greville Street and trendy Acland Street.

Located on the beach, the area boasts a rich history spanning well over 150 years, with a great array of amenities and infrastructure located in the suburb, and nearby. Transport including rail, train lines, and buses, makes St. Kilda one of the most accessible suburbs in Melbourne from the CBD, and the destination of choice for tourists and locals alike. A colorful, artistic, and rich heritage area, St. Kilda consists of a mixture of properties from cutting-edge, modern design apartments to Italianate-Victorian multi-million dollar mansions.

According to REIV capital growth for apartments in St. Kilda over the last 5 years are at 53.9% and have had a staggering 15.9% capital growth over the last 12 months. These are crazy numbers given the volatility of the European markets.

With such outstanding growth, we are excited to have access to an extraordinary new development which is sure to become a Melbourne icon in this most desirable location.

This brand new boutique 4 level development consists of 27 one and two bedroom apartments which have been designed to maximize space and light, complete with heating and air conditioning, security and car parking.

At a starting price point of $350,000 for a one bedroom apartment, to $750,000 for a two bedroom penthouse with city views, over 21 apartments have already been snapped up with only 6 apartments remaining!

This development will not last, so jump on the phones now and request a full Property Investor Analysis (PIA) Report from one of our senior consultants which details the exact out of pocket weekly investment that you will need in order to secure one of these properties.

Remember that many of our clients have secured a property in this development which is only costing them around $50 per week out of pocket.

China’s continued unprecedented growth will create a strong demand for our commodities for decades. Have a look at these staggering growth projections for China:

China’s urban population is expected to swell by up to 400 MILLION by 2025 as workers and their families migrate from the rural towns to cities.

By 2025 there will be 221 Chinese cities that have at least 1 million people living in them (the whole of Europe has only 35 cities with over 1 million people).

5 million buildings will are expected to be constructed by 2025.

Up to 50,000 skyscrapers will be erected – the equivalent of building 2 Chicago’s every year.

As many as 97 new airports are to be built.

1 million kilometres of new road will be laid. That’s enough to travel around the Earth 25 times!

28,000 kilometres of metro rail will be constructed.

That’s just silly growth!

This has resulted in over $500 Billion Dollars invested in mining projects throughout Australia.

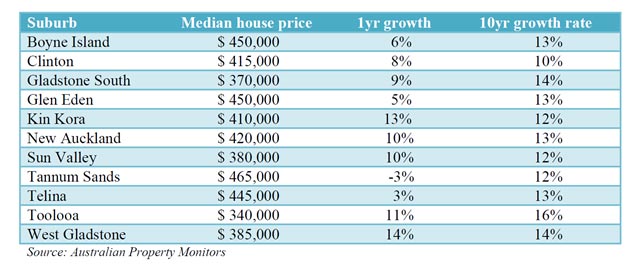

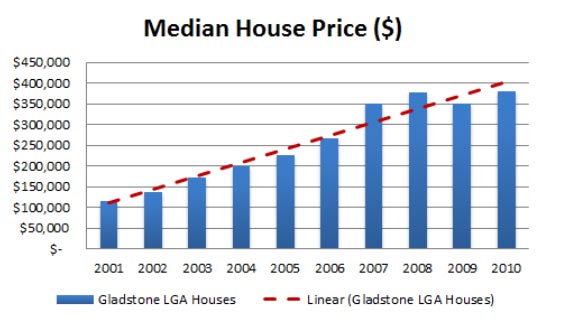

Gladstone Market Overview

Gladstone is currently going through a rapid phase of economic growth. There is $30 billion worth of engineering construction underway, with the resultant construction-related workforce expected to peak in 2014, with a further $70 billion worth of investment planned for the area.

At present, accommodation is so tight that local employees are shifting away from detached rental houses (due to its short supply) and into older apartments or even construction camps. Many are buying now instead of renting. The average Gladstone resident earns 50% more than the typical Australian.

Gladstone’s population is predicted to increase between 10,000 and 25,000 in the next five years. The wide range depends on the scale of future industrial development. Independent modelling by central Queensland University suggests that Gladstone’s median house prices could rise from today’s $480, 000 to between $600, 000 and $925,000 by 2018.

See Gladstone’s key suburbs capital growth history below;

Here are some quick facts about Gladstone;

1. 20% of Queensland exports originate in Gladstone region.

2. 65, 000 permanent residents.

3. Future residents growth 2,300 per annum.

4. 88% dwellings are detached.

5. Need for more small-lot detached housing.

6. Looking forward, given the expected lift in population growth based around Gladstone’s growing economy, there is a need to build about 900 new dwellings each year in the area.

7. Over the past seven years, the underlying demand was for around 800 new housing starts each year. Yet over the same time period, just 600 new dwellings were supplied on an annual basis.

8. In recent years, new housing starts have increased, causing some supply concerns, but the lift from just 300 starts in 2010; to 611 in 2011 and 1, 150 in 2012 is essentially “catch-up”.

9. There are currently about 5, 000 new dwellings approved in the Gladstone region, of which just about 27% have operational works. Approvals take place early in the development process and by their very natures, are a lead supply indicator. ‘Operational works’ is the final stage in the development process.

10. Despite claims to the contrary, there isn’t enough new urban development coming through Gladstone’s construction pipelines.

11. 22, 000 private dwellings.

12. Need to create up to 900 new dwellings every year

13. Despite recent rise in new housing approvals the Gladstone market remains undersupplied

14. Last year alone, 5,600 new jobs were created across central Queensland, about a third of which were located in and around Gladstone

15. Gladstone’s median household annual income exceeds $96,000, which is 50% higher than the Australian average and 33% higher than the average annual earnings in Brisbane

16. There are just 87 properties – as at late August 2012 – available for permanent rental in the Gladstone area. This equates to a 1.3% vacancy rate. Yes, the vacancy rate had lifted from 0.3% this time last year, but keep in mind that most vacant properties in Gladstone take under two weeks to rent and on average five applicants apply per listing. There were 128 properties vacant in July this year, so properties lease quickly in the area

17. Gross rental returns remain very favourable for investors with independent advice suggesting that Rivergum Gladstone house and land product should attract gross rental yields between 6.8% and 7.3%. this compares extremely well with the mid-4% range for many rental properties in the south-east corner of Queensland

18. The billions being invested will create over 9,000 new permanent jobs and thousands of contract workers.

FINAL THOUGHTS

The key to building your wealth in the shortest possible time frame is to appreciate one key fundamental principle of finance which is understanding the Debt Serviceability Ratios (DSR) used by banks and financial institutions, and how they assess and work out how much money you can borrow.

Ultimately, the key is to acquire a combination of Growth Properties which are negatively geared and Cash-Flow Positive properties in order to fast track your accumulation process.

That’s almost it from me for now, but I wish you all great prosperity for 2013 and encourage you to seize all the opportunities before you this year, that will ultimately bring you financial freedom.

To your exciting future…

Konrad Bobilak

CEO of 21st Century Property Direct

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.