Are you thinking of buying Melbourne Investment Properties in 2024 whilst they are still cheap?

Are you thinking of buying Melbourne Investment Properties in 2024 whilst they are still cheap?

Remember that not all Melbourne property is created equal; you need to know where to buy, what to buy, and which suburb represents the best value for money!

Dear Fellow Property Investor,

Australia’s housing market has had a mixed start to spring, but PropTrack data has revealed a number of suburbs around the country that have seen massive growth over the past 12 months.

The data looked at Melbourne suburbs with at least 100 sales for the year, revealing that some areas had experienced boom-like growth cycles.

Melbourne’s housing market shows resilience with significant growth in suburbs like Ivanhoe, Diamond Creek, and Coburg North. Ivanhoe leads the housing growth, while Blackburn, Box Hill, and Surrey Hills witness strong unit growth driven by overseas interest and skilled migrants.

Melbourne’s market has faced unique challenges, including unfavourable investment taxation and changes to tenancy laws making investment properties less attractive.

Leading house price growth over the last 12 months was Ivanhoe (17.3 per cent), Diamond Creek (13.2 per cent) and Coburg North (12.8 per cent).

Blackburn (22.1 per cent), Box Hill (11.1 per cent) and Surrey Hills (11 per cent), led unit growth.

“With higher interest rates, we’ve seen sales at higher price points and a higher turnover in the top quartile.

“With units, Blackburn, Box Hill, and Surrey Hills have all seen significant overseas interest, especially since the Covid lockdowns – skilled migrants have been arriving in these areas and the hospital precinct.“

So let me ask you a question…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the recovery phase of the Melbourne property cycle (which, in my opinion, is RIGHT NOW!)

Or, will you join them?

The choice is yours!

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

They say a picture can be worth a thousand words….

Check out the latest HTW Australian National Property Clock for Melbourne!

That’s right, Melbourne has been slowly moving though the bottom of the housing market property cycle and is now in the best possible section of the property clock – 8:00 o’clock, moving onto 9:00 o’clock which coincides with the BOOM phase!

The BOOM phase starts at 9:00 o’clock and peaks at 12:00 o’clock…

Remember…

You will ONLY get one opportunity like this every 10 years!

So let me ask you a question…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the recovery phase of the Melbourne property cycle (which, in my opinion, is RIGHT NOW!)

Or, will you join them?

The choice is yours!

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the last Real Estate Investing Fast Track Weekend for 2024!

Sydney has long been Australia’s most expensive city for homebuyers, but the price difference between Sydney and Melbourne has reached unprecedented levels.

PropTrack’s Eleonor Creagh said that as of August, Sydney’s median house price is 70% higher than Melbourne’s, with Melbourne homes now 41% cheaper – a $600,000 difference, marking the largest price gap in 20 years.

Housing supply and land constraints drive Sydney’s premium.

One significant factor behind Sydney’s rising premium is its constrained land supply.

Sydney’s natural features, including its harbor and surrounding national parks, limit the availability of developable land. In contrast, Melbourne has seen a higher rate of new home completions per capita.

Over the past decade, Victoria averaged 9.5 new dwellings per 1,000 residents per year, compared to just seven in New South Wales, PropTrack reported.

Higher building costs in Sydney

A recent report by The Centre for International Economics (CIE) also highlighted Sydney’s higher construction costs. Red tape, taxes, and other fees make building new homes in Sydney more expensive, with 50% of these costs tied to such charges, compared to 37% in Melbourne.

“Waterfront properties and international appeal have kept Sydney’s market strong,” Creagh said.

Melbourne’s market struggles post-pandemic

Melbourne has lagged behind other cities since the COVID-19 pandemic, losing population and experiencing less dramatic price increases than other Australian capitals.

Since March 2020, Melbourne has been the weakest performing capital, with house prices still 4.7% below their peak. The city has even dropped to fourth place among Australia’s most expensive capitals, with Brisbane and Canberra surpassing it.

Investor confidence declines in Victoria

Several factors are contributing to Melbourne’s continued underperformance.

Higher land taxes for investment properties have made Melbourne less attractive to investors, while stock levels remain high. In July, Melbourne listings were the highest since November 2018, providing buyers with plenty of choices.

The future of the Sydney-Melbourne divide

Looking ahead, Melbourne’s housing market is expected to remain subdued compared to Sydney, Creagh said.

The combination of a high inventory of homes and softer economic conditions may cause Melbourne prices to fall further. However, as Melbourne houses become more affordable, the price gap could eventually narrow.

While Sydney’s geographic limitations and global appeal may ensure it retains a price premium, the historic price swing may make Melbourne more appealing in the future.

“At some point, Melbourne may be seen as undervalued, given its current price levels relative to Sydney,” Creagh said.

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the last Real Estate Investing Fast Track Weekend for 2024!

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Dear Fellow Property Investor,

Did you know that Tax depreciation is the key to increasing cash flow on your investment property?

Every residential property investor should have a tax depreciation schedule to substantiate and claim maximum deductions.

As the owner of a residential investment property, claiming depreciation deductions can make a big difference to your cash flow.

Of all the tax deductions available to property investors, depreciation is the second largest deduction available after interest.

Both new, and old residential investment properties have substantial depreciable value. On average, BMT finds residential investors an average of over $11,000 in deductions in the first full financial year, and more than forty thousand dollars, in the first five years.

What is tax depreciation?

Tax depreciation is a tax deduction claimed for the natural wear and tear of an income-producing building and its assets over time. It is generally the second biggest tax deduction for property investors, after interest.

Who can claim?

Tax depreciation deductions are available for both residential investment properties and commercial buildings. Most properties, new and old, have depreciation available.

What can you claim?

You don’t need to spend money to claim tax depreciation. Tax depreciation deductions are split into two categories:

Division 43: Capital works deductions

Capital works deductions (division 43) refer to the building’s structure and items that are permanently fixed to the property such as kitchen cupboards, doors and sinks.

Capital works typically make up between 85-90% of the total claim.

There are different rates of depreciation available for different properties based on their type, industry and construction commencement date.

Division 40: Plant and equipment depreciation

Plant and equipment assets (division 40) are items which are easily removable from the property, like carpet and blinds. These assets have a limited effective life as set out by the ATO and can generally be depreciated over time. Investors can claim depreciation deductions for more than 6,000 different ATO recognised plant and equipment assets.

There are some restrictions to claiming depreciation on previously used plant and equipment found in second-hand residential properties as legislation changed in May 2017.

How do I claim depreciation?

A tax depreciation schedule prepared by a specialist quantity surveyor like BMT Tax Depreciation is the best way to substantiate your tax depreciation claim with the ATO.A comprehensive tax depreciation schedule prepared by BMT Tax Depreciation will help you claim all available depreciation tax deductions for the effective life of your investment property.

For a Quote, simply call BMT on 1300 728 726 or online at www.BMTQS.com.au

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

You may need to pay land tax if you own an investment property, holiday home, commercial property or vacant land.

What is land tax?

Land tax is an annual tax based on the total taxable value of all the land you own in Victoria, excluding exempt land such as your home (principal place of residence).

Land tax is calculated using the site values (determined by the Valuer-General Victoria) of all taxable land you owned as at midnight on 31 December of the year preceding the year of assessment.

You may have to pay land tax if you own, either individually or jointly with others:

investment properties, including residential rental properties

commercial properties such as retail shops, office premises and factories

holiday homes

vacant land.

Land tax assessments are generally issued between January and June each year.

Land tax exemptions

Land tax does not apply to exempt land such as:

your home, known as your principal place of residence (PPR)

your farm, known as primary production land (PPL)

rooming houses and charitable institutions.

If you start leasing your home (your principal place of residence) or change your address, the exemption ends and you must notify the ATO immediately.

Paying your assessment

There are 3 ways to pay your land tax assessment – via credit or debit card, BPAY, or in instalments via AutoPay.

If you choose AutoPay, you can pay your land tax assessment in fortnightly, monthly or in four equal payments up to 38-weeks from the issue date on your assessment. AutoPay instalments must be set up annually as instalment amounts can change depending on your tax liability.

You can create an AutoPay arrangement via My Land Tax. It is important to pay or set up a payment arrangement on time to avoid late payment interest and recovery action.

Land tax trust surcharge

Land held on trust for a fixed, discretionary or unit trust is generally assessed at trust surcharge rates of land tax. The trust surcharge does not apply to land held by an administration trust, an excluded trust or an implied or constructive trust.

The trust surcharge rates are higher than general land tax rates and apply once the total value of the taxable land held by the trust is $25,000 or more. When the total value of the taxable land is $3,000,000 or more, there is no difference between the general and trust surcharge land tax rates.

If you tell us about the beneficiaries of the trust, we may assess the trust at general rates and may also assess the beneficiaries for their interest in the trust land in any individual assessments they receive.

Absentee owner surcharge

If you are the trustee of an absentee trust, the absentee owner surcharge applies to the trust’s taxable land. The absentee owner surcharge is additional to the land tax you pay at general or trust surcharge rates.

The surcharge is 4% from the 2024 land tax year (previously 2% for the 2020-2023 land tax years, 1.5% for the 2017-2019 land tax years and 0.5% for the 2016 land tax year).

An absentee trust is a discretionary trust, a unit trust or a fixed trust, which has at least one beneficiary who is an absentee person. If you are the trustee of an absentee trust that owns taxable land, you must also tell us you are an absentee owner.

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Deposit Bond vs. Bank Guarantee: Which is Right for Your Property Purchase?

Securing your next property is an exciting endeavour, but the financial aspects can sometimes be daunting, especially for retirees looking to downsize and transition to a new chapter in their lives. Whether you’re seeking an apartment by the beach, a cozy townhouse, or a penthouse with a view, the path to securing your ideal property should be as smooth as possible.

If you’re in this situation, you may be wondering about the best way to provide a deposit for your new property without tying up your hard-earned cash. Two popular options to consider are deposit bonds and bank guarantees. In this article, we’ll compare these financial tools to help you make an informed decision that suits your unique circumstances.

What is a Deposit Bond?

Let’s start with the basics. A deposit bond is a financial instrument designed to instil confidence in property transactions. It serves as a guarantee to the seller, ensuring that if for whatever reason, the buyer defaults on the property purchase, the insurer will fulfill the deposit requirement. Deposit bonds provide flexibility, ease of acquisition, and can be applied to various property transactions.

What is a Bank Guarantee?

On the other hand, a bank guarantee involves a promise from a bank that it will cover a specific financial obligation should the buyer fail to meet it. In the context of property purchases, a bank guarantee is similar to a deposit bond in that it acts as a guarantee to the seller that the buyer will fulfil the deposit requirement when necessary. Unlike deposit bonds, bank guarantees require the buyer to provide security to the bank usually in the form of a term deposit or property security, therefore tying up their assets as collateral, which can negatively impact financial flexibility.

Benefits of Deposit Bonds;

Preserving Your Investments: You may have your wealth tied up in various investments. Deposit bonds allow you to keep your investments intact while securing your property.

No Need to Use Superannuation: You won’t need to draw on your super fund, keeping your retirement savings intact and continuing to earn you a return.

No Home Equity Required: Unlike bank guarantees, deposit bonds don’t require you to use your home or other assets as security.

Peace of Mind: Deposit bonds provide peace of mind to both buyers and sellers by ensuring the deposit is secure.

Quick to Arrange: Deposit Bonds can be arranged within one or two days which ensures you are less likely to miss out on your property. On the other hand, bank guarantees take weeks to organise due to the requirements of the bank to have various legal documents and securities put in place.

Cost Effective: A Deposit Bond costs around 3% per annum (without the need to provide property or cash security) which is around half the cost of borrowing the money from a bank.

Benefits of Bank Guarantees;

Pay as you go: Banks often allow for the payment of the bank guarantee fee to be made on a ‘pay as you go’ basis such as paying 6 months in advance. A deposit bond needs to paid for in advance however you may qualify for a rebate if your property settles early.

Access to a wide range of properties: Due to bank guarantees being around for a longer period than deposit bonds, they are currently more widely accepted.

Dear Fellow Property Investor,

Recent infrastructure developments and upgrades to local amenities have been key factors in Altona’s recent property price surge, according to a local real estate director.

Real Estate Institute of Victoria (REIV) data showed a 25 per cent increase in the median property price to $1.2 million in the June quarter

The number of properties sold in Altona has remained steady, with 120 properties sold this quarter compared to 118 in the March quarter.

Ray White Altona director Anthony Anile said the steady volume of sales and rising prices indicates a strong demand.

Properties have been selling faster, with the average days on market reducing from 45 to 30 days, while Mr Anile said was a sign of increased buyer interest and competition.

Auction clearance rates have also risen considerably, going from 70 per cent to 85 per cent, the data revealed.

First-home buyers and investors alike have shown an interest in Altona, with increased activity from both demographics.

Mr Anile mentioned “the appeal of a coastal suburb with a relaxed lifestyle,” as being among the deciding factors.

The suburb is attracting young professionals, singles and couples, as well as families,” he said.

“They are drawn by the family-friendly environment, good schools, parks, and community facilities,” he said.

The suburb saw the largest median price increase in Hobsons Bay and Maribyrnong and was significantly higher than the rest of metro Melbourne, which recorded a 1.5 per cent decrease to property prices.

Among the suburbs in Hobsons Bay and Maribyrnong to also record a rise were Altona North (7.8 per cent to $965,000), Footscray (5 per cent to $1.1 million), Kingsville (1.6 per cent to $1.1 million), Laverton (0.8 per cent to $578,000), Seabrook (2.8 per cent to $784,000) and West Footscray (11.4 per cent to $1.02 million).

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

Melbourne renters are now paying almost $2900 more in rent than they were 12 months ago, new data has revealed.

According to PropTrack’s latest Market Insight Report, Melbourne rental prices have climbed by 10.6 per cent in the year to June 2024.

The median advertised rent increased by $55 a week over the last 12 months, meaning renters on average are having to pay $2860 more a year.

Across the board, the median weekly cost of renting a home in Australia’s capital cities has increased by 10.3 per cent.

Renters in Sydney are paying the most ($740 a week), followed by Perth ($650), Brisbane ($620), Darwin ($600) and the ACT (also $600).

Despite the sharp increase over the past 12 months, Melbourne is the third-cheapest city in Australia to rent in ($575 a week), with Adelaide coming in at a close second ($570)

The cheapest place to rent is in Hobart, which recorded a median rental price of $510 a week over the last 12 months.

“Sydney remains the most expensive capital city to rent a home, with the median advertised rent rising 2.8 per cent over the quarter and 8.8 per cent year-on-year to reach $740 per week,” PopTrack said.

“Over the past decade, Perth has transitioned from being the most affordable capital city to rent to the second most expensive behind Sydney, with the median advertised rent hitting $650 per week in June.

“Hobart and the ACT were the only cities which saw rents decline over the quarter, however Hobart remains higher compared to 12 months ago while the ACT’s rental prices have held steady.”

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

Melbourne homeowners are set for an up to $55,000 windfall that could usher in record house prices in the next year.

New PropTrack estimates have tipped the city for 3 per cent to 6 per cent home value growth, the biggest uplift in the past two years after multiple interest rate hikes since May 2022 put the Victorian capital’s housing market in the doldrums.

For Melbourne’s $921,000 median house price, the growth would mean a $27,630-$55,260 surge.

It would also add $18,500-$37,020 to the city’s $617,000 typical unit.

At the upper end of the forecast, the city’s home values would rise more than seven times the 0.8 per cent uptick they recorded this financial year.

PropTrack economic research director Cameron Kusher said Melbourne buyers have had more choice in stock than other states and the city was becoming more attractive to buyers due to its affordability.

“It’s the first time Brisbane is back in line with Melbourne in terms of affordability and the gap (of affordability) between Sydney and Melbourne, it’s one of the largest on record,” Mr Kusher said. “Although Victoria is still seeing a slightly greater loss of people to other states than it is gaining, housing affordability will drive people to want to come to Victoria.

“If you want to build your career you want to be in Sydney or Melbourne.”

Despite the scope for price rises, Mr Kusher said with the new financial year looming there were positive signs for buyers ahead.

“With the tax cuts coming next week we will see buyers borrowing capacity increase and then provided that we have interest rate cuts as well at some point, Melbourne will start looking more affordable and attractive,” he said.

“The state government in Victoria is still seeing investors selling out of the market which is creating space for first home buyers.

“It’s getting more expensive to rent and there is a lot of stock on the market.”

Ray White Craigieburn auctioneer and sales consultant Trish Orrico said 50 per cent of her sales lately had been landlords selling up due to tax hikes for investors, with first home buyers snapping up the residences.

“While these projected figures are positive, we shouldn’t be making assumptions on the property market, we don’t have a crystal ball,” Ms Orrico said.

“The market is the market we are guided by things that are happening within the economy now.”

The analysis from PropTrack revealed national home prices are expected to rise by up to 5 per cent in the new financial year in line with slowing price growth forecast for several capital cities, though more substantial price growth is still possible in Sydney as well as Melbourne.

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

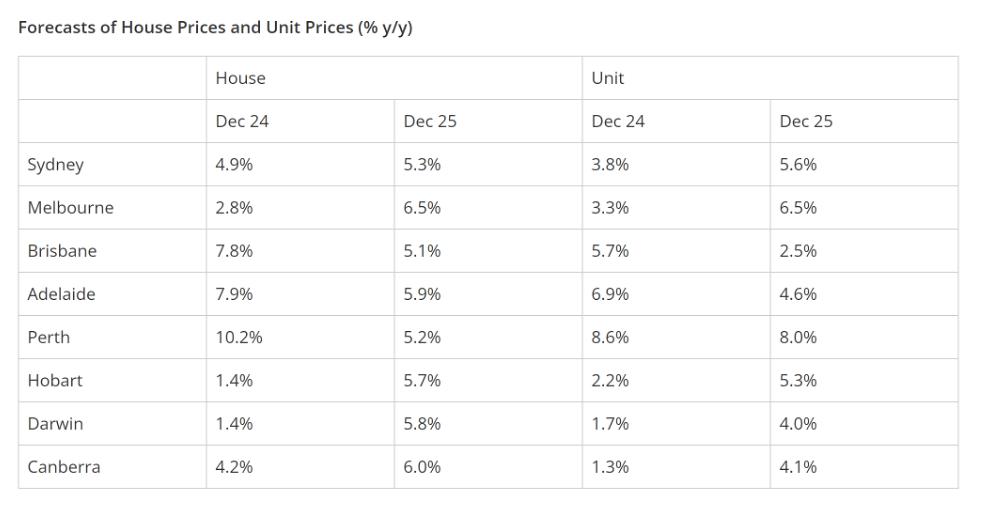

House prices will rise nationally by 5.3% over the next six months and by 5.6% during 2025, KPMG’s new property report on Australia’s capital cities finds.

Apartment prices across the country will see an average rise of 4.5% by December and then match houses by growing by 5.6% in the following 12 months.

For the next six months, there will be considerable national variation with Perth house prices rising by over 10% while Darwin and Hobart only experiencing 1.4% growth. For units, the predicted increases range from Perth’s 8.6% to Canberra’s 1.3%.

But in 2025, there will be much greater house price growth consistency across the country. Melbourne houses will rise the most by 6.5% followed by Canberra at 6.0%, but even the lowest, Brisbane will still rise by 5.1%. By contrast, units will still have considerable regional variation next year, ranging from Perth’s 8.0% growth to Brisbane’s more modest 2.5% increase.

The previous 12 months, to March 2024, saw a 7.7% national rise in house prices – with Perth, Adelaide and Brisbane the stand-out performers – and 6.1% in apartments. The slower growth over the next six months is attributed to a slower rate of migration, and the cooling impact of high interest rates. Prices will then start rising slightly faster during 2025 as rate cuts start to be introduced by the RBA, as KPMG anticipates.

Rents are tipped to rise by 4-5% over the next two years, having increased by 7.8% over the past year, the largest increase since the GFC in 2008/9.

Dr Brendan Rynne, KPMG Chief Economist, said: “In a year of high interest rates and inflation and subdued consumer sentiment the housing market has withstood all those factors and still provided strong price growth, due to demand outstripping supply. Even the much-anticipated ‘fixed-rate cliff' – the transition of mortgage holders off lower fixed rates to higher variable rates – has only had a mild impact and households have so far coped well with the rate rises, due to a robust labour market and Australia’s historic low unemployment rate.”

“Supply has remained insufficient, and while we do forecast a slight rise in housing approvals, this will take time to translate into actual housing completions, due to the time lag inherent in the process. Although material costs and financing costs have started to stabilise after sustained increases, labour costs continue to increase in response to high demand for qualified tradespeople. Many barriers remain to developers building new homes, while continuing high rental costs are pushing renters to look to buy instead, which is pushing up demand.”

“After the exceptional house price increases we have seen in several capital cities over the past 12 months, we do forecast a slowdown in the rate of growth, given the drop in migration, the delayed impact of high interest rates and a predicted increase in unemployment over the rest of this year. Foreign investment activity has also yet to regain its levels of two years ago. But overall we will still see solid price gains over the next 18 months, especially in 2025, as the RBA starts to introduce interest rate cuts, as we anticipate”.

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.