House prices to rise more gradually over next 18 months.

(KPMG Australia releases latest property report)

Dear Fellow Property Investor,

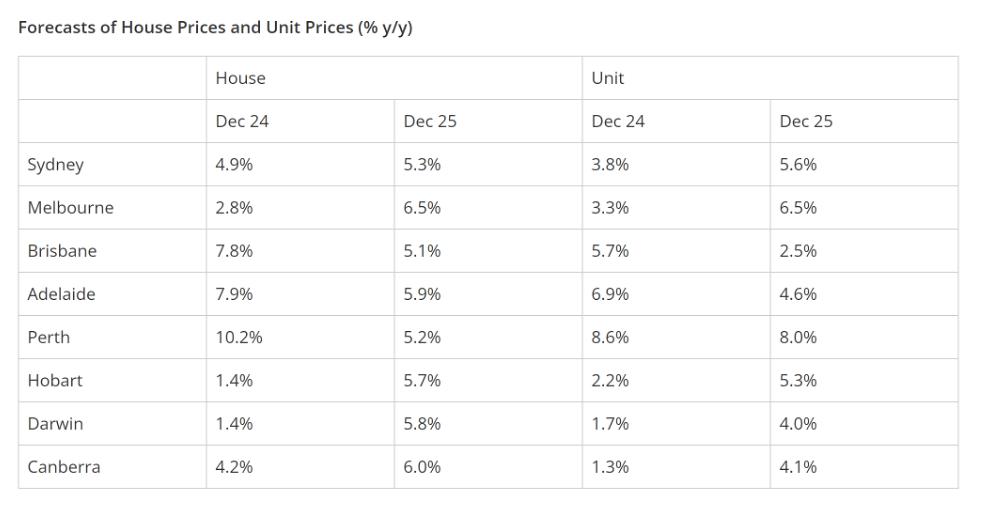

House prices will rise nationally by 5.3% over the next six months and by 5.6% during 2025, KPMG’s new property report on Australia’s capital cities finds.

Apartment prices across the country will see an average rise of 4.5% by December and then match houses by growing by 5.6% in the following 12 months.

For the next six months, there will be considerable national variation with Perth house prices rising by over 10% while Darwin and Hobart only experiencing 1.4% growth. For units, the predicted increases range from Perth’s 8.6% to Canberra’s 1.3%.

But in 2025, there will be much greater house price growth consistency across the country. Melbourne houses will rise the most by 6.5% followed by Canberra at 6.0%, but even the lowest, Brisbane will still rise by 5.1%. By contrast, units will still have considerable regional variation next year, ranging from Perth’s 8.0% growth to Brisbane’s more modest 2.5% increase.

The previous 12 months, to March 2024, saw a 7.7% national rise in house prices – with Perth, Adelaide and Brisbane the stand-out performers – and 6.1% in apartments. The slower growth over the next six months is attributed to a slower rate of migration, and the cooling impact of high interest rates. Prices will then start rising slightly faster during 2025 as rate cuts start to be introduced by the RBA, as KPMG anticipates.

Rents are tipped to rise by 4-5% over the next two years, having increased by 7.8% over the past year, the largest increase since the GFC in 2008/9.

Dr Brendan Rynne, KPMG Chief Economist, said: “In a year of high interest rates and inflation and subdued consumer sentiment the housing market has withstood all those factors and still provided strong price growth, due to demand outstripping supply. Even the much-anticipated ‘fixed-rate cliff' – the transition of mortgage holders off lower fixed rates to higher variable rates – has only had a mild impact and households have so far coped well with the rate rises, due to a robust labour market and Australia’s historic low unemployment rate.”

“Supply has remained insufficient, and while we do forecast a slight rise in housing approvals, this will take time to translate into actual housing completions, due to the time lag inherent in the process. Although material costs and financing costs have started to stabilise after sustained increases, labour costs continue to increase in response to high demand for qualified tradespeople. Many barriers remain to developers building new homes, while continuing high rental costs are pushing renters to look to buy instead, which is pushing up demand.”

“After the exceptional house price increases we have seen in several capital cities over the past 12 months, we do forecast a slowdown in the rate of growth, given the drop in migration, the delayed impact of high interest rates and a predicted increase in unemployment over the rest of this year. Foreign investment activity has also yet to regain its levels of two years ago. But overall we will still see solid price gains over the next 18 months, especially in 2025, as the RBA starts to introduce interest rate cuts, as we anticipate”.

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.