Data recently released by the ABS shows that household net worth has increased substantially over recent years however, household debt is also climbing to new record highs.

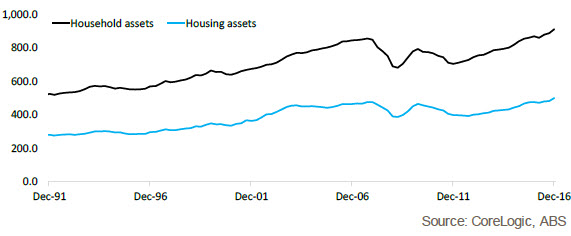

The ABS’ recent release on finance and wealth for the December 2016 quarter showed that the net worth of Australian households was $9.405 trillion. This comprised $11.710 trillion in assets minus $2.306 trillion in liabilities (including share capital). Over the 12 months to December 2016, net worth has increased by 8.3% with asset values increasing by 7.9% and liabilities increasing by 6.4%. The data breaks out the value of residential land and dwellings which as at the end of 2016 was valued at $6.114 trillion having increased by 8.3% over the year. Residential land and dwellings accounts for 52.2% of total household assets.

Using the data that the ABS publishes on wealth, the Reserve Bank (RBA) publishes a number of finance ratios for households comparing debt and assets to disposable incomes.

At the end of 2016, the ratio of household debt to disposable income was recorded at 188.7%, the highest on record and rising by 1.6 percentage points over the quarter and 3.1 percentage points over the year. The ratio of housing debt to disposable income was recorded at 133.8% which was also a record high. Based on this data, 70.9% of total household debt was housing debt. Over the quarter, housing debt increased by 1.5 percentage points and was 4.5 percentage points higher over the year.

While the ratios of household and housing debt to disposable incomes is at record-high levels, so too are the ratios of household and housing assets to disposable incomes. The ratio of housing assets to disposable incomes sits at 910.6% having increased by 23.2 basis points over the quarter and 42.2 basis points over the year. Meanwhile, the ratio of housing assets to disposable income sits at 500.4% having increased by 18.2 basis points over the quarter and 23.8 basis points over the year.

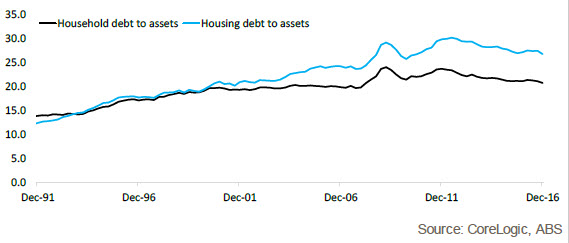

Comparing household debt to assets results in a ratio of 20.7% while the figure for housing debt to housing assets is 26.7%. This indicates that although household and housing debt is at an historic high level, the value of the assets that this debt is held against is also higher than it has ever been.

The data within this report should be viewed with some caution because it is not a granular analysis; so while the national figures may show a strong financial position, at smaller geographies, particularly where dwelling values are falling, the position is likely to be dramatically different. With regard to debt, the figure is measured as a national measure and includes those households that are renting and those that own a home but carry no housing debt. Some households have held their homes for many years and paid down a substantial amount of the debt on the home. For those that have either recently purchased, bought at the peak of a market which has since declined or those using interest-only mortgages they are unlikely to be in such a strong position as the national figures indicate. Those that don’t own a property asset are also likely to have substantially less household assets than those that do own a home.

Overall household debt is higher than it has ever been and although asset values are also at a record high, there remains concerns about how healthy it is to have such high levels of private debt. Furthermore, high debt, particularly for recent purchasers of residential properties, creates risks in the event of a housing market downturn which could see home owners enter into a period of negative equity. Especially with the heightened level of investor purchasing recently, investors have demonstrated a greater willingness to sell at a loss because that loss can be offset against future gains. Those that own owner occupied property do not enjoy a similar ability to offset these losses and are potentially much more financially vulnerable in the event of a housing market downturn. The high level of household debt is also expected to limit the ability for the RBA to lift interest rates suggesting that a neutral cash rate setting will be lower than it has been in the past.

This article was originally published by Cameron Kusher on the 10 April 2017 via corelogic.com.au

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.