Melbourne housing boom: Prices set to skyrocket up to $55,000, 6 per cent, in Financial Year 2025!

Dear Fellow Property Investor,

Melbourne homeowners are set for an up to $55,000 windfall that could usher in record house prices in the next year.

New PropTrack estimates have tipped the city for 3 per cent to 6 per cent home value growth, the biggest uplift in the past two years after multiple interest rate hikes since May 2022 put the Victorian capital’s housing market in the doldrums.

For Melbourne’s $921,000 median house price, the growth would mean a $27,630-$55,260 surge.

It would also add $18,500-$37,020 to the city’s $617,000 typical unit.

At the upper end of the forecast, the city’s home values would rise more than seven times the 0.8 per cent uptick they recorded this financial year.

PropTrack economic research director Cameron Kusher said Melbourne buyers have had more choice in stock than other states and the city was becoming more attractive to buyers due to its affordability.

“It’s the first time Brisbane is back in line with Melbourne in terms of affordability and the gap (of affordability) between Sydney and Melbourne, it’s one of the largest on record,” Mr Kusher said. “Although Victoria is still seeing a slightly greater loss of people to other states than it is gaining, housing affordability will drive people to want to come to Victoria.

“If you want to build your career you want to be in Sydney or Melbourne.”

Despite the scope for price rises, Mr Kusher said with the new financial year looming there were positive signs for buyers ahead.

“With the tax cuts coming next week we will see buyers borrowing capacity increase and then provided that we have interest rate cuts as well at some point, Melbourne will start looking more affordable and attractive,” he said.

“The state government in Victoria is still seeing investors selling out of the market which is creating space for first home buyers.

“It’s getting more expensive to rent and there is a lot of stock on the market.”

Ray White Craigieburn auctioneer and sales consultant Trish Orrico said 50 per cent of her sales lately had been landlords selling up due to tax hikes for investors, with first home buyers snapping up the residences.

“While these projected figures are positive, we shouldn’t be making assumptions on the property market, we don’t have a crystal ball,” Ms Orrico said.

“The market is the market we are guided by things that are happening within the economy now.”

The analysis from PropTrack revealed national home prices are expected to rise by up to 5 per cent in the new financial year in line with slowing price growth forecast for several capital cities, though more substantial price growth is still possible in Sydney as well as Melbourne.

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Did you know that Property Investors are swallowing up even more of the housing market?

In Australian politics there are relatively few issues outside of foreign policy that the two major parties can agree on. But there is one issue where both sides ostensibly agree: greater levels of home ownership.

In the run up to the last federal election, then Opposition Leader Anthony Albanese promised that a Labor government would help people achieve the “great Australian dream of home ownership”.

“For too long Australians who have worked hard have been locked out of the housing market by flat wages and rising prices, unable to even get a foot in the door let alone a roof over their heads,” Albanese said.

Opposition leader Peter Dutton shared similar views on home ownership with the press late last year: “the best way to empower Australians — to make them masters of their fate — is through home ownership.”

The leaders of the major parties sharing this view on home ownership is nothing new. Over 70 years ago there were debates in federal parliament not too dissimilar from todays, in which the leaders of the Coalition and Labor made their case on which party would do a better job building more new homes and getting more Australians into homes of their own.

Rhetoric collides with reality The peak rate of home ownership was recorded 57 years ago as part of the 1966 census, at which time 73 per cent of households owned homes. More recently, the Australian Institute Of Health and Welfare (AIHW) recorded a home ownership rate of 71.4 per cent in 1995. As of the latest data from the 2021 census, the home ownership rate has dropped to 66 per cent.

This raises an uncomfortable question for the nation’s leaders. After spending more than $20.5 billion on grants, concessions and other cash grants to first home buyers in the decade to 2021, home ownership rates have not risen, but instead have continued to decline.

Solely based on the decline in the proportion of households who own homes, there around 560,000 households who are renting today who would have otherwise been homeowners if the home ownership rate remained as it was in 1995.

Rise and rise Despite rising levels of home ownership being the stated priority of both the major parties their policies have achieved the polar opposite. The AIHW data instead illustrates a very different trend: the rise of the property investor.

In 1995, 18.4 per cent of households rented from a private landlord. As of 2020, 26.2 per cent rented from a private landlord and this is arguably somewhat distorted lower by the snapshot being taken during the pandemic.

If we extrapolate that on to the current number of households as determined by the ABS, private landlords have roughly 810,000 more tenant households today than they would have if the ratio of private landlord held housing to overall housing stock remained the same as 1995.

Today’s market According to data from the ABS, over the last 12 months 33.4 per cent of new mortgages for existing properties have flowed to property investors. In terms of new mortgages overall including construction loans and brand-new properties, that figure rises to 34.3 per cent.

By dollar value the proportion of mortgage lending flowing to investors recently hit the highest level since 2017, hitting a share of 36.2 per cent of all new housing finance.

With investors holding 26.2 per cent of occupied housing stock, this level of activity implies a growing proportion of the nation’s housing stock once more flowing to investors, unless otherwise offset by a much greater proportion of owner occupiers making fully cash purchases or investors selling out of the market at a greater rate than they are buying in.

Which raises the big question in all of this, how is the home ownership rate going to rise when the current set of incentives and policies have delivered 25 years of strong growth in the proportion of investor held housing stock instead?

Aspiration nation Both of the major parties like to paint themselves as the standard bearers for aspirational Australians, of folks who are trying to get ahead. But the simple reality is recipe for success is not what it once was.

In decades past, a household could work hard within the reality of their circumstances and work their way up to a median or well above median household income, then be able to purchase a home that reflected that.

In 1999, a household in the 80th percentile for income (higher than 80% of households), could purchase a home that was valued in the 80th percentile. Meanwhile the median earning household could purchase the median house. This is based a household having a 20 per cent deposit, additional cash for stamp duty and spending 25 per cent of gross income on the mortgage.

Today the median earning household can only afford 13 per cent of homes and even more affluent households in the 80th percentile are now competing for median priced homes. In states like NSW and Victoria its even worse. In NSW, households in the 80th percentile can only afford 1/3 of homes, while in Victoria less than half are affordable for these more affluent households.

Reality check Both Labor and the Coalition speak of hard work and the importance of home ownership, yet neither has the makings of a credible plan that would see home ownership rates increase back toward levels seen in the mid-1990s, let alone the all-time peak.

It was once said that doing the same thing again and again, and expecting a different result was the definition of insanity. After spending over $20 billion on first homebuyer support mechanisms over the past decade and actually lowering the home ownership rate during that time, it’s clear a different strategy is needed.

Ultimately, where we go from here is in the hands of the electorate. For decades political leaders have talked the talk on home ownership, then failed to walk the walk. Up until now that arguably hasn’t had a major political downside for the major parties, but with the issue of housing fast becoming one of the hottest in Canberra and around dining tables, one wonders if that will change.

Dear Fellow Property Investor,

With property prices reaching record highs across the country, the humble home has become the main breadwinner in many households. In certain suburbs, homes are earning multiple times the average wage.

National property prices hit new record highs in February, up 6.15% compared to a year ago, the fastest annual rise since July 2022, according to PropTrack.

For hundreds of thousands of Australians, that growth means their homes may have generated more income than their own salaries over the past year.

New analysis has used PropTrack's automation valuation model (AVM) to reveal the suburbs around the country where the median property price has grown by more than the average Australian wage.

According to ABS data released in February, the gross weekly ordinary time earnings for full-time adults was $1,888.80 in November 2023, which translates to average annual earnings of $98,218. Given the family home is exempt from the capital gains tax, an increase in value stretches even further than the average annual wage on a dollar-for-dollar basis.

Almost 900 suburbs around the country saw their median property price grow by more than $98,218 in the year to February.

The suburbs that saw the steepest hikes in value were the premium pockets in capital cities, which is unsurprising according to PropTrack senior economist Paul Ryan.

"In exclusive suburbs the same percentage increase will lead to a larger increase in terms of dollar value. And remember too, some of those premium suburbs saw quite sharp reductions in prices in 2022 so this is prices snapping back."

But solid price growth also happened in more affordable areas, Mr Ryan added.

"Over the past year or so, we've seen even and consistent growth within cities. While we're still seeing strong demand and strong growth in premium suburbs, this is happening in more affordable suburbs too."

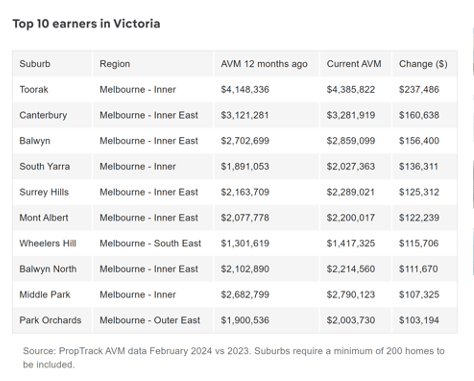

Melbourne property prices grew by a relatively modest 1.33% over the year, but in the exclusive inner-Melbourne suburbs of Toorak and South Yarra, houses gained $237,486 and $136,311 respectively.

Here are the suburbs in Melbourne where properties have earned the most this past year:

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

Apartments are selling at a loss in Australia's two biggest cities even during a housing affordability crisis, new data shows.

Record-high immigration has pushed up house prices but more inner-city units are selling at a loss in already-overcrowded Sydney and Melbourne than anywhere else.

An ultra-tight rental market and a digit-double surge in rents during the past year is also no guarantee that units will go up in value, especially if they are in a high-rise tower.

In the centre of Melbourne, 40.7 per cent of apartments sold at a loss during the December quarter - or 6.8 times the national average loss rate of 6 per cent, CoreLogic data showed.

Tim Lawless, CoreLogic's head of research, said oversupply was an issue in that part of Melbourne.

'Higher supply levels across the inner Melbourne apartments sector are likely to be a factor in this under performance, coupled with the preference shift towards lower density housing options though the pandemic,' he told Daily Mail Australia.

'Areas of inner Melbourne are now recording the highest population density of any region nationally.'

In the centre of Melbourne, 40.7 per cent of apartments sold at a loss during the December quarter - or 6.8 times the national average loss rate of 6 per cent, CoreLogic data showed (pictured is the Docklands area near the city) - and 98 per cent of loss-making sales were apartments.

CoreLogic noted that 98 per cent of loss-making sales were apartments, even though sellers in the Melbourne City Council area had held on to their apartments for an average of nine years and eight months.

Losses are more likely to occur in areas where apartments were built during the 2010s, when interest rates were lower and building activity was much stronger.

This has led to an oversupply of apartments in some areas and in some cases, quality issues.

'Unit supply was particularly elevated in the mid-to-late 2010s, buoyed by a high concentration of investor participation in the housing market and structurally falling interest rates,' CoreLogic said.

In Melbourne's city centre, the median apartments price is $473,483, or 28.2 per cent less than greater Melbourne's mid-point apartments price of $607,473.

Despite the tight rental vacancy rate, North Melbourne's apartments prices fell 0.3 per cent during the past year to $505,702.

Apartments are even cheaper at Flemington with a median unit price of $410,528.

But at Docklands, they are a bit dearer at $592,863, which would still be attainable for an average-income worker on $98,218.

In the neighbouring Port Phillip City Council area, 21.3 per cent of apartments sold at a loss, with this densely-populated area covering bayside St Kilda where the median apartments price is $530,584.

In Windsor, the median apartments price plunged by 6.2 per cent during the past year to $512,633.

Next door in the Stonnington council area, 27 per cent of apartments sold at a loss.

This covers South Yarra, a suburb with a median apartments price of $579,182, following a 4.2 per cent decline during the past year.

In ultra-upmarket Toorak, the mid-point apartment price fell by 3.4 per cent over the year to $1.033million.

So my advice is do not buy apartments in Melbourne CBD just yet…unless you are taking on a ultra long-term investment horizon and plan to hold them for 20 to 30 years!

If you have enjoyed this short email, then I encourage you to reserve your place and join me and 55 like-minded property investors for the next Real Estate Investing Fast Track Weekend for 2024!

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Dear Fellow Property Investor,

I realise that Apartments tend to get a bad rap when it comes to property investing.

And rightly so…many Melbourne suburbs such as Docklands, South Bank, and Melbourne CBD, just to name a few, have proven a complete disaster when it comes to long-term capital growth, with many apartments underperforming the rate of inflation…

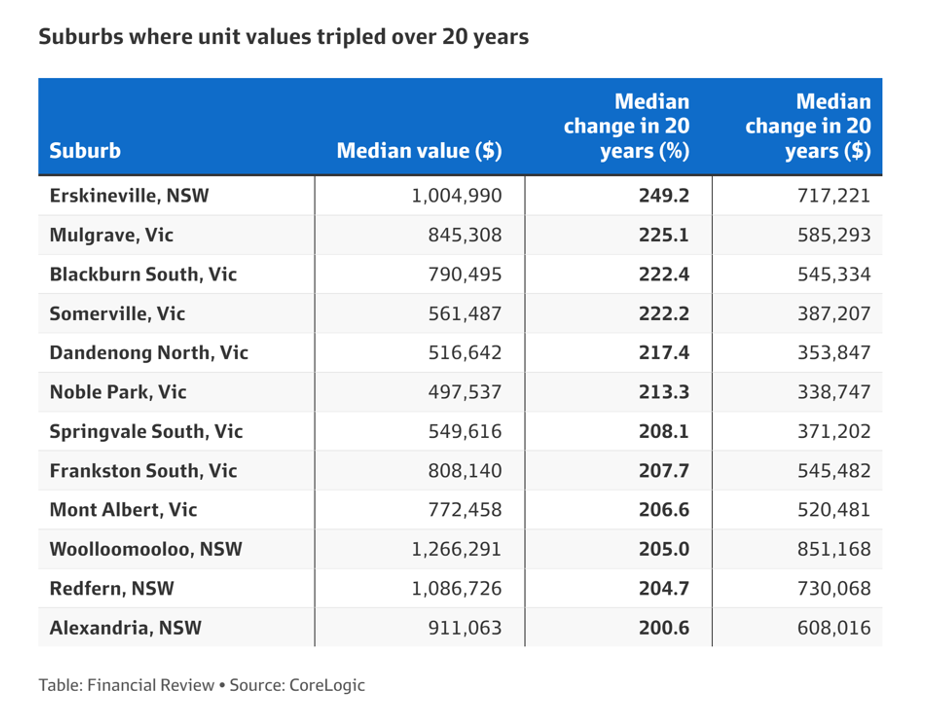

But did you know that according to a recent CoreLogic report, Unit [Apartments] values in Blackburn South and Mont Albert in Melbourne’s inner east, Mulgrave, Dandenong North, Noble Park, Springvale and Springvale South in the south-east and Somerville and Frankston South on the Mornington Peninsula have more than tripled in the past 20 years.

Unit prices in Melbourne climbed faster than both Sydney and Brisbane over the past 20 years, increasing by 120 per cent, data from CoreLogic shows.

Those gains were boosted by strong population growth and lower stock levels in the 2000s.

Sydney’s median unit value increased by 115 per cent, while Brisbane lifted by 81 per cent during the same period.

Underlining Melbourne’s performance over the past two decades, units across 85 per cent of all its suburbs more than doubled in value, while prices in more than 10 suburbs tripled over the same period.

A large chunk of the growth in Melbourne unit values in the past 20 years occurred before and after the GFC with unit values surging more than 20 per cent in 2007 and also in 2009-10, according to CoreLogic.

Let me ask you something…

Do you have a game plan for 2024?

Or will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which, in my opinion, already bottomed out in November 2022), again?

Or, will you join them?

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors for the first Real Estate Investing Fast Track Weekend for 2024!

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Off-the-plan apartment prices in some Melbourne suburbs could go up by as much as 25 per cent over the next year as developers adjust pricing amid rising costs and increasing demand, property advisory firm Charter Keck Cramer says.

“Prices will recalibrate upwards, and I think in about 12 months, it’s going to be across the entire Melbourne apartment market,” said Richard Temlett, Charter Keck Cramer’s national executive director.

“In certain areas, depending on the developer and project, buyers can expect to pay between 15 per cent and 25 per cent, even more in some cases. That’s certainly where the market is going and evolving.”

Developers will have to increase prices to offset the rising land values and construction costs so they can continue delivering apartment projects. But many remained reluctant to raise prices amid low consumer sentiment and higher interest rates, Mr Temlett said.

“Many developers are still very worried about increasing prices. And I’m encouraging them to be a bit more brave because there are sound fundamental reasons to support price increases,” he said.

“The development industry needs to realise that over the next six to 12 months, they can increase prices in a lot of areas and will still be met with a deeper pool of buyers. In fact, it’s already happening in some projects.”

Charter Keck Cramer’s analysis of a sample of off-the-plan apartment projects across various locations in Melbourne shows that several of those released this year have increased their prices by 15 per cent to 25 per cent compared to pre-COVID prices of apartments in earlier stages of the same development or in comparable projects in the same locations.

The study spanned 10 suburbs in the middle ring areas, and consisted of three apartment projects on average.

“The price gains were submarket specific, but those that posted large increases were not high-end landmark projects, they were quality owner-occupier stock in the suburbs,” Mr Temlett said.

“Interestingly, the market is accepting those price increases, albeit at a slow rate. Buyers understand what’s happening with costs and what’s happening in the market, and they are prepared to pay a higher rate.

“So these are demonstrable examples of apartment prices reverting upwards. I think there’s going to be an increase in demand for such dwellings because we’re not building enough houses or apartments.”

The advisory firm predicts that Melbourne’s apartment supply is set to slump by 7900 units, or 65.3 per cent, by 2025.

Mr Temlett said the rapid interest rate increases, substantial rise in construction costs and volatile consumer sentiment have made many apartment projects unfeasible and led to very slow sales rates.

Meanwhile, the 4 percentage point interest rate rise since May last year has slashed buying power by more than 40 per cent.

However, these factors also opened up a very large but slightly different buyer and renter pool over the next 12 months, he said.

“With rapid rate rises, there is anticipated to be a ‘shuffle’ downwards or trade-off, where many buyers are forced to trade into medium- and higher-density dwellings as dictated by their revised finances,” Mr Temlett said.

“Many people are still willing to buy, but they can’t afford to buy a standalone house because of affordability, so more will either be forced to live in apartments or will embrace apartment living.”

The price premium of houses over apartments has widened to 60 per cent despite a 9 per cent house price drop from the peak. Since March 2022, house prices are still 15 per cent higher than pre-COVID and are poised to continue rising.

“With rapidly rising rents, some renters may decide to buy and pay off a mortgage given that rental repayments may be similar to mortgage repayments in some markets and across various product types,” Mr Temlett said.

“These potential buyers are likely to seek the most affordable product type, which will be apartments.”

Mr Temlett said while conditions in the build-to-sell apartment market were arguably the toughest they have ever been, the sector will continue to improve.

“We believe that the RBA is close to the top of the rate-tightening cycle. When rates stabilise, we expect market demand will start to be expressed and sales rates will accelerate,” he said.

“When rates start to be cut, there is anticipated to be an extremely elastic response across the entire housing market, with the apartment market well poised to benefit.”

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Dear Fellow Property Investor,

One of the most important aspects of building and structuring a large residential property portfolio is to start with the end in mind.

That is, you must have an exact strategy or Blue-Print that is concise and all-encompassing before you start investing in property.

Many investors get into a lot of trouble because they simply never clearly articulated and mapped out a concise strategy to begin with. Or they end up buying the wrong type of property, such as a serviced apartment in Queensland, studio apartment with living areas less than 50 square meters, or an apartment in a high-density development, and most likely end up selling that property within 5 year, realising a small profit and in most cases breaking even or a loss.

The first thing that you must appreciate is that you will go through 3 distinctive stages while you are building your property portfolio:

The Acquisition and building stage,

The Consolidation and refining stage,

And the Harvesting stage.

These stages will vary from investor to investor, and will differ depending on investors personal Risk Profile, and time horizon for investing, as well as the amount of time, money or equity available.

In this segment of the event, you will gain a clear understanding of the importance of developing a personalised investment plan, based on your unique set of circumstances, and available resources.

During this segment of the event, you will also gain an understanding of the importance of creating a Master-Plan blue-print, before you do anything else.

That is, your ability to clearly identify your outcome and ultimate goal for building a large residential investment property portfolio.

Now here is one of the most important aspects covered in this YouTube Video;

“You’ve got to know your numbers!” - That’s probably one of the most common pieces of advice you’ll hear from wealthy (and RICH) property investors. - “You’ve got to know your numbers!” –

And in this segment, you will learn how to calculate cash-flow analysis via Property Investor Analysis Software.

The Property Investment Analysis (PIA) Program is an essential decision making tool for all property investors.

It will analyse capital growth, cash flow, and tax implications for any investment property and provide instant feedback on projected after-tax cost and rate of return.

The software will compute cash flow projections for up to 40 years and has facilities for changing more than 100 variables including property price, rent, capital growth, inflation, deposit and loan type.

The internal rate of return (IRR) and the cost-per-week are recalculated automatically whenever a change is made.

That’s all for this months video, stay tuned for my next video. CLICK HERE to subscribe to my Youtube channel so you don't miss out.

Dear Fellow Property Investor,

CoreLogic’s national Home Value Index (HVI) has recorded a third consecutive monthly rise, with the pace of growth accelerating sharply to 1.2% in May.

After finding a floor in February, home values increased 0.6% and 0.5% through March and April respectively.

Sydney continues to lead the recovery trend, posting a 1.8% lift in values over the month, recording the city’s highest monthly gain since September 2021. Since moving through a trough in January, home values have risen by 4.8%, or the equivalent of a $48,390 lift in the median dwelling value.

Brisbane (1.4%) and Perth (1.3%) are the only other capitals to record a monthly gain of more than 1.0%, however, the rise in values was broad-based with the rate of growth accelerating across every capital city last month.

CoreLogic’s Research Director, Tim Lawless, noted the positive trend is a symptom of persistently low levels of available housing supply running up against rising housing demand.

“Advertised listings trended lower through May with roughly 1,800 fewer capital city homes advertised for sale relative to the end of April. Inventory levels are -15.3% lower than they were at the same time last year and -24.4% below the previous five-year average for this time of year,” he said.

“With such a short supply of available housing stock, buyers are becoming more competitive and there’s an element of FOMO creeping into the market. Amid increased competition, auction clearance rates have trended higher, holding at 70% or above over the past three weeks. For private treaty sales, homes are selling faster and with less vendor discounting.”

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors at the next Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

OUR PAST ATTENDEES RAVED ABOUT THIS EVENT… WATCH WHAT THEY HAVE TO SAY.

I look forward to meeting you at the event!

Yours in Success,

KONRAD BOBILAK

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Right Now In 2023, The Melbourne Property Market Is Experiencing ‘A Perfect Storm’ Of Buying Opportunities For Educated And Market Ready Investors!

These are the following reasons why NOW is the Perfect Storm!

1. Chinese buyers return to Australia's housing market and snap up properties, sparking fears prices could rise even further! Foreign buyers are returning to the Australian property market; the fear is, they could drive up the cost of homes for Aussies already struggling to buy one.

China was the largest source of investment for residential real estate investment proposals by number and value ($0.6 billion), as it was in 2021-22 and 2020-21. The next two largest sources of residential investment were Hong Kong ($0.1 billion) and Vietnam ($0.1 billion).

The investment figures that were recently released by the Australian Government’s Treasury, in its Quarterly Report on Foreign Investment, cover the last quarter of 2022.

Total foreign investment in Australia fell sharply but Chinese buyers remained the most significant, with $600 million of approved investment, even though that was down $1 billion.

With Hong Kong investment included in the Chinese total, Chinese investment this quarter accounted for $700 million of Australian property. After China, the next largest investors were Vietnam, Singapore, and the United Kingdom, each of which invested $100 million in residential real estate.

In this quarter, the largest target sector for proposed investment for the quarter by value was commercial real estate, with a total value of $19.3 billion.

The United States was the largest source country for commercial investment proposals by number and value ($16.7 billion), as it was in 2021-22 and 2020-21.

The next four largest source countries by value were China ($6.7 billion), Singapore ($5.2 billion), South Korea ($4.2 billion), and Canada ($3.8 billion).

While the overall numbers are down, the return of Chinese students to Australia, an end to pandemic travel bans, and warming relations between the two countries, are driving a rise in property inquiries from China.

Juwai IQI Co-Founder and Group Managing Director Daniel Ho said that at the current rate, China would invest an estimated $3.2 billion in Australian residential real estate this year, which would be up from $2.4 billion in 2021-22.

With the inclusion of Hong Kong, China would invest $3.8 billion, which would be up from $3 billion last year.

“In 2022 and so far this year, Australia is the most popular country for Chinese homebuyers, for the first time ever, according to Juwai IQI Chinese buyer enquiries,” Mr Ho said.

“In January, Chinese buyer inquiries for Australian real estate surged by 24 percent compared to December, due to the announcement that borders would be reopening.” The latest data from national removalist booking platform Muval has revealed Australians are continuing their exodus from Sydney, looking strongly in favor of Melbourne.

2. Inbound inquiries show the laneway capital remains streets ahead of the rest according to the platform; Melbourne was the most popular city to move to in 2022, with the February figures showing the city accounted for the most eyeballs. 28% of all major metro inbound moving inquiries were for Melbourne. This is an increase from last January when Melbourne accounted for 24%.

3. Melbourne homeowners are holding back from listing properties in the declining market, resulting in almost a 30 percent drop in the number of homes for sale in some regions year on year.

House hunters have fewer properties to choose from as falling property prices prompt vendors to rethink plans and some to delay selling until the market improves.

Buyers in Melbourne’s north-east have seen the biggest drop in homes on offer, as new listings in January – properties marketed for 30 days or less – were down 28.2 percent year on year. This fall was closely followed by the inner south, where new listings dropped by 28.1 percent.

The inner region was down 21.9 percent, the outer east 19.7 percent, and the west 15.4 percent.

New listings were down more than 10 percent across Melbourne, but the number of homes hitting the market on the Mornington Peninsula rose 3.3 percent.

The total number of homes for sale was also down in most Melbourne regions except in the northwest and west of the city, where numbers were up 13.9 percent and 8.2 percent respectively. In the Mornington Peninsula, they were up 27.8 percent.

4. Melbourne rents have rocketed to record highs, jumping as much as 20 percent in a year and prompting fears of homelessness and housing stress for low-income households. In fact, there has never been a tougher time to be a renter in Melbourne, where vacancy rates are just 1.4 percent and rents have hit record highs.

The median weekly cost of renting an apartment in Melbourne last week hit $450 – a 20 percent increase on 12 months earlier – while in inner Melbourne rents have reached a weekly median of $490 a week, according to the Domain Rent Report for the December quarter.

The most recent Australian Bureau of Statistics figures, taken in August, showed the median weekly income in Melbourne was $1300 (across Victoria the median was $1250). Rental stress is defined as paying more than 30 percent of one’s income in rent, meaning for a single renter on a median wage in Melbourne, anything more than $390 a week would put them in rental stress.

For houses, the median rent reached a record high of $480 and grew 7.9 per cent in the 12 months to December.

The increase comes amid growth in demand as tenants make pandemic living habits permanent and eschew share houses for their own space, at the same time as international borders reopen.

While rental increases are bad news for tenants, its great news for landlords, especially for those who purchased their investment properties in the inner east and Bayside where rental yields have increased over 16 and 17 per cent respectively, far beyond any increases in interest rates over the same time period.

5. Record Low Vacancy Rates;

6. Financial markets think rate hikes are done... now pricing is in a rate cut through the second half of the year.

In fact, I believe, that many property investors who are currently staying out of the property market will look back retrospectively and realise that November and December 2022 were in fact the lowest and most opportune times to enter the Melbourne property market from a ‘Market Timing Perspective’…

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.