Melbourne Housing recovery accelerates: CoreLogic Home Value Index surges with the strongest monthly growth since November 2021

Dear Fellow Property Investor,

CoreLogic’s national Home Value Index (HVI) has recorded a third consecutive monthly rise, with the pace of growth accelerating sharply to 1.2% in May.

After finding a floor in February, home values increased 0.6% and 0.5% through March and April respectively.

Sydney continues to lead the recovery trend, posting a 1.8% lift in values over the month, recording the city’s highest monthly gain since September 2021. Since moving through a trough in January, home values have risen by 4.8%, or the equivalent of a $48,390 lift in the median dwelling value.

Brisbane (1.4%) and Perth (1.3%) are the only other capitals to record a monthly gain of more than 1.0%, however, the rise in values was broad-based with the rate of growth accelerating across every capital city last month.

CoreLogic’s Research Director, Tim Lawless, noted the positive trend is a symptom of persistently low levels of available housing supply running up against rising housing demand.

“Advertised listings trended lower through May with roughly 1,800 fewer capital city homes advertised for sale relative to the end of April. Inventory levels are -15.3% lower than they were at the same time last year and -24.4% below the previous five-year average for this time of year,” he said.

“With such a short supply of available housing stock, buyers are becoming more competitive and there’s an element of FOMO creeping into the market. Amid increased competition, auction clearance rates have trended higher, holding at 70% or above over the past three weeks. For private treaty sales, homes are selling faster and with less vendor discounting.”

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors at the next Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

OUR PAST ATTENDEES RAVED ABOUT THIS EVENT… WATCH WHAT THEY HAVE TO SAY.

I look forward to meeting you at the event!

Yours in Success,

KONRAD BOBILAK

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Right Now In 2023, The Melbourne Property Market Is Experiencing ‘A Perfect Storm’ Of Buying Opportunities For Educated And Market Ready Investors!

These are the following reasons why NOW is the Perfect Storm!

1. Chinese buyers return to Australia's housing market and snap up properties, sparking fears prices could rise even further! Foreign buyers are returning to the Australian property market; the fear is, they could drive up the cost of homes for Aussies already struggling to buy one.

China was the largest source of investment for residential real estate investment proposals by number and value ($0.6 billion), as it was in 2021-22 and 2020-21. The next two largest sources of residential investment were Hong Kong ($0.1 billion) and Vietnam ($0.1 billion).

The investment figures that were recently released by the Australian Government’s Treasury, in its Quarterly Report on Foreign Investment, cover the last quarter of 2022.

Total foreign investment in Australia fell sharply but Chinese buyers remained the most significant, with $600 million of approved investment, even though that was down $1 billion.

With Hong Kong investment included in the Chinese total, Chinese investment this quarter accounted for $700 million of Australian property. After China, the next largest investors were Vietnam, Singapore, and the United Kingdom, each of which invested $100 million in residential real estate.

In this quarter, the largest target sector for proposed investment for the quarter by value was commercial real estate, with a total value of $19.3 billion.

The United States was the largest source country for commercial investment proposals by number and value ($16.7 billion), as it was in 2021-22 and 2020-21.

The next four largest source countries by value were China ($6.7 billion), Singapore ($5.2 billion), South Korea ($4.2 billion), and Canada ($3.8 billion).

While the overall numbers are down, the return of Chinese students to Australia, an end to pandemic travel bans, and warming relations between the two countries, are driving a rise in property inquiries from China.

Juwai IQI Co-Founder and Group Managing Director Daniel Ho said that at the current rate, China would invest an estimated $3.2 billion in Australian residential real estate this year, which would be up from $2.4 billion in 2021-22.

With the inclusion of Hong Kong, China would invest $3.8 billion, which would be up from $3 billion last year.

“In 2022 and so far this year, Australia is the most popular country for Chinese homebuyers, for the first time ever, according to Juwai IQI Chinese buyer enquiries,” Mr Ho said.

“In January, Chinese buyer inquiries for Australian real estate surged by 24 percent compared to December, due to the announcement that borders would be reopening.” The latest data from national removalist booking platform Muval has revealed Australians are continuing their exodus from Sydney, looking strongly in favor of Melbourne.

2. Inbound inquiries show the laneway capital remains streets ahead of the rest according to the platform; Melbourne was the most popular city to move to in 2022, with the February figures showing the city accounted for the most eyeballs. 28% of all major metro inbound moving inquiries were for Melbourne. This is an increase from last January when Melbourne accounted for 24%.

3. Melbourne homeowners are holding back from listing properties in the declining market, resulting in almost a 30 percent drop in the number of homes for sale in some regions year on year.

House hunters have fewer properties to choose from as falling property prices prompt vendors to rethink plans and some to delay selling until the market improves.

Buyers in Melbourne’s north-east have seen the biggest drop in homes on offer, as new listings in January – properties marketed for 30 days or less – were down 28.2 percent year on year. This fall was closely followed by the inner south, where new listings dropped by 28.1 percent.

The inner region was down 21.9 percent, the outer east 19.7 percent, and the west 15.4 percent.

New listings were down more than 10 percent across Melbourne, but the number of homes hitting the market on the Mornington Peninsula rose 3.3 percent.

The total number of homes for sale was also down in most Melbourne regions except in the northwest and west of the city, where numbers were up 13.9 percent and 8.2 percent respectively. In the Mornington Peninsula, they were up 27.8 percent.

4. Melbourne rents have rocketed to record highs, jumping as much as 20 percent in a year and prompting fears of homelessness and housing stress for low-income households. In fact, there has never been a tougher time to be a renter in Melbourne, where vacancy rates are just 1.4 percent and rents have hit record highs.

The median weekly cost of renting an apartment in Melbourne last week hit $450 – a 20 percent increase on 12 months earlier – while in inner Melbourne rents have reached a weekly median of $490 a week, according to the Domain Rent Report for the December quarter.

The most recent Australian Bureau of Statistics figures, taken in August, showed the median weekly income in Melbourne was $1300 (across Victoria the median was $1250). Rental stress is defined as paying more than 30 percent of one’s income in rent, meaning for a single renter on a median wage in Melbourne, anything more than $390 a week would put them in rental stress.

For houses, the median rent reached a record high of $480 and grew 7.9 per cent in the 12 months to December.

The increase comes amid growth in demand as tenants make pandemic living habits permanent and eschew share houses for their own space, at the same time as international borders reopen.

While rental increases are bad news for tenants, its great news for landlords, especially for those who purchased their investment properties in the inner east and Bayside where rental yields have increased over 16 and 17 per cent respectively, far beyond any increases in interest rates over the same time period.

5. Record Low Vacancy Rates;

6. Financial markets think rate hikes are done... now pricing is in a rate cut through the second half of the year.

In fact, I believe, that many property investors who are currently staying out of the property market will look back retrospectively and realise that November and December 2022 were in fact the lowest and most opportune times to enter the Melbourne property market from a ‘Market Timing Perspective’…

Dear Fellow Property Investor,

Did you know that despite the recent 11 interest rate increases from the Reserve Bank of Australia, which has seen official rates rise by 3.75 percent over the last twelve months, property prices in Melbourne are on the rise?

That’s right, we are witnessing the next phase of the 7 to 10-year property cycle, and it’s the beginning of the next bull run…

But unlike in the previous property cycle, the Boom in Melbourne is occurring on two fronts simultaneously…capital growth appreciation and record-high rental yield increases!

In fact, the latest data by NAB below shows us that the current rental yield increases averaged a staggering 10% across Australian listed dwellings!

And that’s just in the last 12 months!

I mean it just doesn’t get any better than this!

So, what are you waiting for?

Reserve your place and join me and 55 like-minded property investors at the next

Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

I look forward to meeting you at the event!

Yours in Success,

KONRAD BOBILAK

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Dear Fellow Property Investor,

Did you know that Melbourne and Sydney have officially entered the beginning of the growth part of the next property cycle?

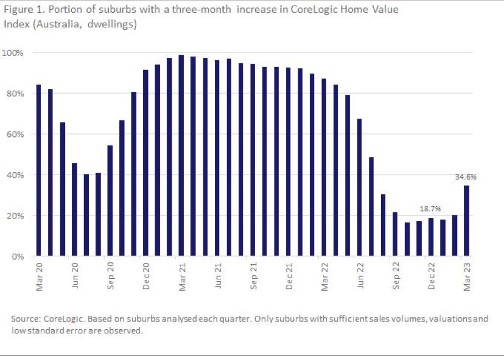

This CoreLogic graph perfectly captures the cyclical nature of the Australian property market – and suggests we may be entering another growth phase.

The share of Australian suburbs that recorded price growth over a rolling three-month period rose from 18.7% in December to 34.6% in March.

As the graph shows, the market started booming in late 2020, and, by early 2021, almost every suburb in Australia was experiencing quarterly growth.

The market then cooled sharply from early 2022, but this downturn appears to have bottomed out in October when 16.5% of suburbs posted quarterly growth.

Since then, the share of growth in suburbs has been trending upward.

So the first million-dollar question is…

Are you market-ready to take advantage of the prevailing circumstances?

And the next million-dollar question is;

Do you have the skills and knowledge to correctly identify the best-performing suburbs in Melbourne in 2023 right now?

Or will you simply wait by the sidelines and see other savvy property investors snap up the best opportunities?

Now I know what you are thinking…

But Melbourne is very expensive now, as the average 3-bedroom townhouse in the bayside area or the eastern suburbs costs between $1.5 to $2 million dollars.

And yes, that’s very true.

So If you have a budget of only $700K, where do you buy?

Well, the answer is in suburbs that are currently going through the process of gentrification!

The bad and ugly ducklings of today will become the trendy-hipster suburbs of tomorrow.

Case and point; Brunswick 20 years ago, Carlton 20 years ago, St Kilda 20 years ago, Northcote 20 years ago, and Yarraville 20 years ago, just to name a few.

Take Northcote for example, known as the poster boy of the Gentrification phenomena in Melbourne, from 2011 to 2023 Northcote boomed!

In Northcote West, the median income is now $1216 per individual, an increase of 62 percent from 2011. In Northcote East, the median leaped 55 percent over the decade to $1130.

Footscray and Yarraville were also suburbs that were showing similar signs of gentrifying. Wealth has also increased rapidly in Thornbury, the median weekly income has risen from $641 in 2011 to $1041 by 2021, an increase of 62 percent.

So where are the Gentrification suburbs of tomorrow?

Join me for an exclusive 1.15-hour video where you will discover advanced property investing strategies to use in the current market to identify, with laser-like precision the best-performing Gentrification suburbs of tomorrow!

You will also learn specific real estate finance and due diligence methodologies that will give you the confidence and skills to start building your property portfolio as soon as you finish watching the video;

Many of you will be thinking right now…’ have I missed the boat? Especially on Suburbs experiencing Gentrification?

Well not really….

One of the most fundamental principles of property investing in Australia is to appreciate that the market moves in distinct cycles which are characterized by periods of strong capital growth and demand for properties, through to periods of a flat-lining market, following periods of distinctive falling median prices, lower demand for properties, and a decline in property prices.

The general rule of thumb is that these property cycles last 7 to 10 years, and can be segmented into 4 main parts, the ‘Peak of the Market’ being the shortest of the four;

Peak of the Property Market – High capital growth, auction clearance rates of 85% plus.

Decline of the Property Market – Declining capital growth, auction clearance rates dropping from 80% to 60% and 50%.

Bottom of the Property Market – Extended periods of low capital growth, auction clearance rates of 45% to 50%.

Growth of the Property Market – Increasing capital growth, increase demand for property, increased auction clearance rates, 55% to eventually 75%.

Would you like to know exactly where Melbourne or Sydney is located right now on the property clock?

I will be revealing the location of our major property markets on the property clock during this video.

Plus…

I will also reveal my TOP 10 Gentrification Suburbs of Tomorrow, those that are destined to experience double-digit capital growth over the next decade!

In fact, one of these suburbs is booming right now, and no one is noticing or even talking about it in the mainstream media.

The main thing to remember is that money is made by both the timing of the market, and of time in the market.

Finally, for those of you with deeper pockets, I will show you the top ten suburbs in Melbourne that have consistently hit double digits in Capital growth over the last 10 years, and more importantly, the top 10 areas that will have the highest potential to outperform the rest of the property market in 2023 and over the next 5 years!

I will also show you the exact type of properties, i.e. house and land packages, townhouses, or apartments to target in these areas, and why….this section will surprise many of you.

So what are you waiting for?

Check out this video NOW!

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

CoreLogic Home Value Index: National home values up 0.6% in March, breaking a 10-month streak of falls.

After remaining virtually flat in February (-0.1%), CoreLogic’s national Home Value Index (HVI) posted the first month-on-month rise since April 2022, up 0.6% in March. Dwelling values were higher across the four largest capital cities and most of the broad ‘rest-of-state’ regions, led by a 1.4% gain in Sydney.

CoreLogic’s Research Director, Tim Lawless, put the rise down to a combination of low advertised stock levels, extremely tight rental conditions and additional demand from overseas migration.

“Although interest rates are high and there is an expectation the economy will slow through the year, it’s clear other factors are now placing upwards pressure on home prices,”

Mr Lawless said. “Advertised supply has been below average since September last year, with capital city listing numbers ending March almost -20% below the previous five-year average. Purchasing activity has also fallen but not as much as available supply; capital city sales activity was estimated to be roughly -7% below the previous five-year average through the March quarter.

“With rental markets this tight, it’s likely we are seeing some spillover from renting into purchasing, although, with mortgage rates so high, not everyone who wants to buy will be able to qualify for a loan. Similarly, with net overseas migration at record levels and rising, there is a chance more permanent or long-term migrants who can afford to, will skip the rental phase and fast track a home purchase simply because they can’t find rental accommodation.”

The lift in housing values has been most evident across the upper quartile of Sydney’s housing market. House values within the most expensive quarter of Sydney’s market were up 2.0% in March and the upper quartile of the Sydney unit market was 1.4% higher over the month. “Sydney upper quartile house values fell by -17.4% from their peak in January 2022 to a recent low in January 2023, the largest drop from the market peak of any capital city market segment.

We may be seeing some opportunistic buyers coming back into the market where prices have fallen the most,” Mr Lawless said. Regional housing markets have mostly shown firmer housing conditions as well, with the combined regionals index rising 0.2% over the month.

Housing values across Regional WA and Regional SA remain at cyclical highs despite 10 rate hikes.

SA’s Fleurieu[1] Kangaroo Island SA3 sub-region led capital gains over the month with a 2.6% rise in dwelling values followed by Dubbo, NSW (2.5%), Wellington, Victoria (2.4%) and Mid West, WA (2.1%).

“The best performing regional markets are quite different to what we were seeing through the recent growth cycle,” Mr Lawless said.

“In today’s market it is mainly rural areas that are seeing the strongest increases, rather than the commutable coastal and lifestyle markets that were booming through the upswing.

However, we are seeing some subtle growth return to regions within commuting distance of the major capitals, after many recorded a sharp drop in values.

”But housing values aren’t rising everywhere. Hobart recorded the largest drop in home values among the capital cities, down -0.9% over the month. Housing values across the southern most capital have fallen -12.9% since peaking in May last year; overtaking Sydney as the largest cumulative fall from peak across the capital cities. However, the pace of decline has been easing across Hobart over the past three months.

Canberra (-0.5%), Darwin (-0.4%) and Adelaide (-0.1%) also recorded a decline in values over the month, as did Regional Victoria (-0.1%) and Regional Tasmania (-0.7%). Housing values across every capital city and broad rest-of-state region remain higher relative to the onset of COVID in March 2020.

Melbourne dwelling values are the closest to pre-COVID levels, with only a 0.6% buffer (up from a 0.03% buffer a month ago). At the other extreme is Adelaide where housing values remain a stunning 41.2% above the levels recorded at the onset of COVID, and Regional SA where values remain at a record high, 49.2% above March 2020 levels.

Dear Fellow Property Investor,

Guess What?

Did you know that SQM Research managing director Louis Christopher said the rapidly improving auction markets and increasing asking prices by vendors, were also clear signs the Sydney and Melbourne housing markets have bottomed out.

Asking prices for Sydney homes had climbed by 2.7 per over the past four weeks ended April 11. They increased by 0.9 per cent in Melbourne and lifted by 0.7 per cent nationwide according to SQM Research.

Clearance rates also stayed firm, with the combined capital cities’ clearance rate averaging 65.4 per cent in the four weeks ending 2 April 2023, which is stronger than the final weeks of 2022.

“I believe the worst is over for the Sydney and Melbourne markets,” Mr Christopher said. “We’re confident that the housing market would recover from here provided the cash rate peaks below 4 per cent, which looks like it would.

“We’ve still got inflation out there and housing historically has been a good hedge against inflation.

“We’ve also got record population growth, so we’re seeing a surge in underlying demand for accommodation, and it’s showing up clearly in the rental market. But that also feeds through into the sales market as well because many new arrivals don’t want to rent. That’s why we’re increasingly confident of housing market recovery in 2023.”

Reserve your place and join me and 55 like-minded property investors at the next

Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

I look forward to meeting you at the event!

Yours in Success,

KONRAD BOBILAK

Dear Fellow Property Investor,

Big News!

The housing price downturn is over for Sydney and Melbourne, according to the key property data analysts, who have called the bottom of the market, saying the record return of migrants would bolster prices.

While some housing economists said prices might still have further to fall – if interest rates continued to rise – even those who aren’t yet calling a bottom said the faster-than-expected return of immigration after the pandemic would underpin the housing market.

“Immigration is going to be stronger than developers anticipated some 12 to 24 months prior, and we saw in the 2000s how unexpected immigration can be a fillip to prices,” said Challenger chief economist Jonathan Kearns, a former head of financial stability at the Reserve Bank.

“Other factors were at play then also, and in the pandemic, unexpected lack of immigration was more than offset by declining household size and general demand for more housing.”

CoreLogic, SQM Research, Proptrack and RBC Capital Markets have all declared house prices had bottomed out in the two biggest housing markets amid a growing number of housing indicators showing a marked upturn.

“As more data flows have come through across housing finance, consumer sentiment, vendor discounting and sales volumes, it seems the national housing market downswing may have bottomed out in early March,” said CoreLogic head of research Eliza Owen.

Reserve your place and join me and 55 like-minded property investors at the next

Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

“A record return in overseas migration was unexpected, and it has left housing demand far outstripping supply, which has contributed to the start of a more sustained upswing in value.”

CoreLogic’s daily index also indicates Sydney seems to have bottomed out in the first week of February, and have since increased around 2 per cent, while Melbourne bottomed out early March and has picked up 0.7 per cent.

This means that national home values have dropped by 9.4 per cent peak-to-trough, which is the largest housing market downswing on record, according to CoreLogic. However, this is significantly lower than many economists’ average forecast of a 15 per cent decline.

For Sydney, house prices had dropped by 14 per cent peak-to-trough and Melbourne slumped by 9.8 per cent. These results are lower than many economists’ forecast of 20 per cent price falls for Sydney and a 15 per cent drop in Melbourne.

“The start of an upswing is usually marked by a pick-up in the higher end of the Sydney and Melbourne market, which was also reflected in March home value index data,” Ms Owen said.

In March, Sydney’s premium eastern suburbs jumped by 3.1 per cent, and in Melbourne, monthly home values rose fastest in the expensive inner east, lifting by 1.3 per cent. The tiered hedonic index also shows a strong recovery trend in the top 25 per cent of home values across the capital cities according to CoreLogic.

Sales volumes also recovered strongly, jumping by 10.4 per cent month-on-month through March, although still down year-on-year by about 16 per cent according to CoreLogic.

Reserve your place and join me and 55 like-minded property investors at the next Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

I look forward to meeting you at the event!

Yours in Success,

KONRAD BOBILAK

Dear Fellow Property Investor,

Let me ask you something.

Do you have a game plan for 2023?

Or will you simply sit on the sidelines and wait for a clear market recovery to take place before you start buying investment properties?

Will you watch savvy, educated, market-ready investors snap up all the bargains at the bottom of the Melbourne property cycle (which in my opinion by the way has already bottomed out in November 2022), or will you join them?

You see all the economic indicators are pointing to the Melbourne property market starting to slowly move into the next phase of the property cycle. Not only is inflation down to 6.8 percent in February, and continuing to decline….but also we are having a record number of new migrants about to enter the country, all on landscape of low volume of stock offered for sale, by both owner occupiers and developers alike!

You see…

The Albanese Government is reportedly planning for a total of 650,000 new migrants to settle here by mid-2024.

Combined with estimates for next year, this means a total of 1.2 million extra people will be living in Australia in June next year compared to five years earlier.

The floodgates are being opened to skilled migrants, international students, and those coming for family or humanitarian reasons, even though Sydney and Melbourne (home to more than half of those who have come to Australia in the last 20 years) have ultra-low one percent rental vacancy rates.

SQM Research managing director Louis Christopher said surging immigration would make it even harder for people looking for a home to find accommodation, with weekly rents in Sydney soaring by 25 percent during the past year compared with 22 percent in Melbourne.

This unprecedented influx of skilled migrants, and international students will put a great amount of pressure on the capital growth of properties, as well as increases in rental yields!

Great news for property investors!

Bad news for tenants, and first-time home buyers.

So, what will you do about it?

What are you waiting for?

Reserve your place and join me and 55 like-minded property investors at the next Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

Ultimately, you will be placing yourself into one of the following categories;

1. The Analytical Compulsive Information Gatherer; usually coming from a technical industry such as engineering, science, or medicine, these property investors will spend months and years conducting market due diligence, analysing charts, and crunching numbers.

They tend to read lots of property books, attend workshops, and frequent property investing forums and chatrooms….

Most experience ‘analysis paralysis’, due to so many opposing views that exist in the industry on what constitutes the best way to invest, and in most cases, they end up not investing at all…spending years on the sidelines waiting for the perfect time to invest…which never eventuates.

2. The ‘Get Rich Quick’ Gambler; this group of people usually come from a direct selling background, or multi-level marketing, and have a general interest in ‘alternative’ medicine, alternative energy healing, health and fitness, green drinks, and love conspiracy theories.

This group is very open-minded, and has a great sense of urgency built to get results NOW! Many of these people have undertaken extensive personal development, and hence believe that anything is possible…including becoming a multi-millionaire overnight!

This group of people tends to make impulsive investment decisions and in most cases is not afraid to jump in first!

In a lot of cases they end up losing money by investing in Gold Coast properties, Cash flow positive properties in Mining towns, US properties, European holiday apartments, etc.

3. The Comfort Zone Investor; makes up the vast majority of the property investor market in Australia today, or 72.8% of investors who have one investment property.

This group of people tends to be the PAYG middle class, they are skeptical about attending or spending money on seminars or any type of personal development, books, or courses as they claim it’s ‘just common sense’….or you can just ask your accountant or financial planner for advice…

Most of these investors are structured incorrectly, and have no idea about how to conduct any type of property or market due diligence or cash flow analysis and end up buying one property, within 3 to 5km of where they live…their ‘comfort zone’, and in most cases, the property is comparable to the one they live in themselves.

4. The Active, Savvy Property Investor; makes up a small percentage of the entire Australian population, in fact, only 0.9% of all property investors end up owning more than 6 investment properties.

The active savvy property investors come from all walks of life and have varying amounts of income, education, and age groups…but they do have 1 thing in common, and that is a SYSTEM!

You see, developing and implementing a SYSTEM is the single difference between success and failure when it comes to the world of property investing.

By Attending the 2-Day Live Real Estate Investing Fast Track Weekend you will learn a proven system that has worked for thousands of successful property investors to successfully build large property portfolios….

And it comes down to the following 4 things;

1. Cultivating the right investor PSYCHOLOGY,

2. Developing the right tailor-made PLAN,

3. Developing a team of EXPERTS around you, and

4. Understanding PROPERTY SELECTION METHODOLOGY!

So, if you have been sitting on the sidelines watching other property investors around you going from strength to strength then you need to book yourself into the next Real Estate Fast-Track Weekend live workshop!

Reserve your place and join me and 55 like-minded property investors at the next Real Estate Investing Fast Track Weekend!

Seats are strictly limited so book NOW in order to avoid future disappointment…

I look forward to meeting you at the event!

Yours in Success,

KONRAD BOBILAK

Don’t miss out, CLICK HERE to get up to date video education from Konrad Bobilak.

Dear Fellow Property Investor,

Did you know that one-bedroom flats in the big cities have missed out on Australia's property boom despite interest rates being at record lows?

National home prices last year surged by 22.1 per cent - the fastest annual growth for a calendar year since 1989.

House values in some capital cities went up by a third in just one year as two and three-bedroom units had double-digit annual price growth.

But one-bedroom apartments hardly increased in value at all, especially in cities with oversupply issues, Domain sales data showed.

In Australia's biggest cities, values were either flat over the year or increased by single digits even though the Reserve Bank kept the cash rate at a record-low of 0.1 per cent.

Young couples with a child usually prefer something larger with a bedroom for the baby, which means the potential market for one-bedroom units is smaller.

Investors often buy smaller apartments to rent out but Sydney's unit market is now going backwards for the first time since late 2020 despite a reopening of Australia's border to international students and skilled migrants.

Economists are expecting the Reserve Bank to raise interest rates later this year, which would cause a slowdown in house price increases and a fall in 2023.

In Melbourne, the median price for a one-bedroom unit remained flat over the year, staying at $395,000 as the city was kept in lockdown for many months.

By comparison, mid-point house prices in the same city rose by 18.6 per cent to $1,101,612.

Apartments in general still had a lacklustre year with two-bedroom units in Melbourne going up by 4.5 per cent to $606,000.

Larger, three-bedroom units did better though with values rising by 12.1 per cent over the year to $846,250.

Inner-city areas of the Victorian capital had some of Australia's highest rental vacancy rates during the earlier stages of the pandemic, after the border was closed to foreigners.

Sydney also saw smaller units vastly underperform the increase in house prices and larger apartments.

One-bedroom units went up by just 6.6 per cent annually, to $680,000.

This was well below the 33.1 per cent surge in the median house price to $1,601,467.

Larger apartments, however, had double-digit growth with two-bedroom unit prices rising by 10.9 per cent last year to $825,000.

The median price of a three-bedroom apartment in Sydney went up by 14.1 per cent to $1.325million.

But new CoreLogic data released this week showed Sydney's house and unit prices together falling by 0.1 per cent in February - marking the first decline since September 2020, before the Reserve Bank cut the cash rate to a record-low of 0.1 per cent.

Median apartment values dropped by 0.3 per cent to $831,793, which was the sharpest decline since November 2020.

Australia's median home price last year rose by more than 22 per cent, marking the fastest calendar year increase since 1989.

The annual increase has slowed to a still-strong 20.6 per cent, with $728,034 now the middle point for a property.

One-bedroom units in Brisbane went up by just 4.1 per cent over the year to $333,150, the Domain data showed.

This occurred as the median house price surged by 25.7 per cent to $792,065.

Two-bedroom apartments had double-digit price growth, going up by 10.2 per cent to $452,000.

But the median price for a three-bedroom unit fell by 2.1 per cent to $460,000.

Canberra, however, was a rare exception with the median price of a one-bedroom unit surging by 15.4 per cent to a still-affordable $410,000.

Two-bedroom units did even better with an annual price increase of 28.6 per cent to $575,000 as three-bedroom apartment prices rose 25.9 per cent to $752,000.

Last year, Canberra's mid-point house price rose by 36.6 per cent to $1,178,364.

But in the other mainland capital cities, the value of one-bedroom apartments went up in the single digits last year.

Perth's median price for a one-bedroom flat rose by just 6.3 per cent to $276,500.

But this was at least better than the 1.4 increase for two-bedroom units, taking the mid-point to $350,000.

In Adelaide, the median price of one-bedroom apartments increased by eight per cent to $289,000.

By comparison, two-bedroom unit prices rose by four per cent over the year to $348,500.

Nonetheless, three-bedroom units had strong growth, with prices climbing by 15.9 per cent to $524,000.

Kind regards,

KONRAD BOBILAK

Interested in learning more about property investing in Australia? Please visit our main website InvestorsPrime.com.au for loads of free resources, articles, videos and more to help you on your investing journey.